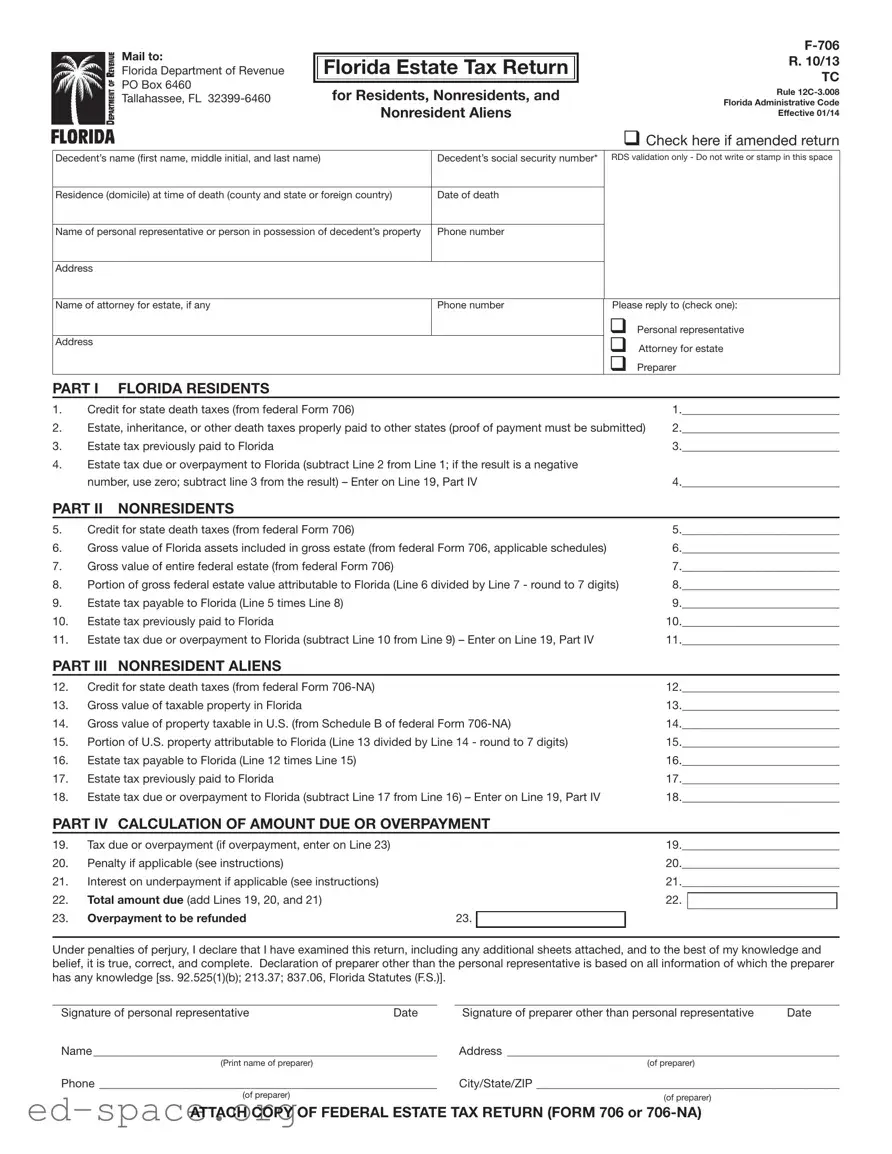

The Florida F 706 form is a crucial document for managing estate taxes in the state. It serves as the Florida Estate Tax Return, and its filing is essential for both residents and nonresidents who meet specific criteria. The form requires detailed information about the decedent, including their name, Social Security number, and residence at the time of death. Additionally, it outlines the responsibilities of the personal representative or the attorney managing the estate. Key sections of the form address various tax credits and obligations, including state death taxes, estate taxes paid to other states, and calculations for any due or overpaid amounts. Understanding the requirements for filing, including the need for a signed copy of the federal estate tax return, is vital for compliance. Filing deadlines and potential penalties for late submissions further underscore the importance of timely and accurate completion of this form. Failure to adhere to these guidelines can result in significant financial repercussions. The form also provides guidance on amending returns and the process for obtaining a nontaxable certificate, making it an essential tool for estate management in Florida.

Mail to:

Florida Department of Revenue

PO Box 6460

Tallahassee, FL

|

||

Florida Estate Tax Return |

R. 10/13 |

|

TC |

||

|

||

for Residents, Nonresidents, and |

Rule |

|

Florida Administrative Code |

||

|

||

Nonresident Aliens |

Effective 01/14 |

q Check here if amended return

Decedent’s name (first name, middle initial, and last name) |

Decedent’s social security number* |

RDS validation only - Do not write or stamp in this space |

|

|

|

Residence (domicile) at time of death (county and state or foreign country) |

Date of death |

|

|

|

|

Name of personal representative or person in possession of decedent’s property |

Phone number |

|

|

|

|

Address |

|

|

|

|

|

Name of attorney for estate, if any |

Phone number |

Please reply to (check one): |

|

|

q Personal representative |

Address |

|

q Attorney for estate |

|

|

|

|

|

q Preparer |

PART I FLORIDA RESIDENTS

1. |

Credit for state death taxes (from federal Form 706) |

1.___________________________ |

2. |

Estate, inheritance, or other death taxes properly paid to other states (proof of payment must be submitted) |

2.___________________________ |

3. |

Estate tax previously paid to Florida |

3.___________________________ |

4.Estate tax due or overpayment to Florida (subtract Line 2 from Line 1; if the result is a negative

|

number, use zero; subtract line 3 from the result) – Enter on Line 19, Part IV |

4.___________________________ |

|||||

PART II |

NONRESIDENTS |

|

|

|

|

|

|

5. |

Credit for state death taxes (from federal Form 706) |

|

|

5.___________________________ |

|||

6. |

Gross value of Florida assets included in gross estate (from federal Form 706, applicable schedules) |

6.___________________________ |

|||||

7. |

Gross value of entire federal estate (from federal Form 706) |

|

|

7.___________________________ |

|||

8. |

Portion of gross federal estate value attributable to Florida (Line 6 divided by Line 7 - round to 7 digits) |

8.___________________________ |

|||||

9. |

Estate tax payable to Florida (Line 5 times Line 8) |

|

|

9.___________________________ |

|||

10. |

Estate tax previously paid to Florida |

|

|

10.___________________________ |

|||

11. |

Estate tax due or overpayment to Florida (subtract Line 10 from Line 9) – Enter on Line 19, Part IV |

11.___________________________ |

|||||

PART III |

NONRESIDENT ALIENS |

|

|

|

|

|

|

12. |

Credit for state death taxes (from federal Form |

|

|

12.___________________________ |

|||

13. |

Gross value of taxable property in Florida |

|

|

13.___________________________ |

|||

14. |

Gross value of property taxable in U.S. (from Schedule B of federal Form |

14.___________________________ |

|||||

15. |

Portion of U.S. property attributable to Florida (Line 13 divided by Line 14 - round to 7 digits) |

15.___________________________ |

|||||

16. |

Estate tax payable to Florida (Line 12 times Line 15) |

|

|

16.___________________________ |

|||

17. |

Estate tax previously paid to Florida |

|

|

17.___________________________ |

|||

18. |

Estate tax due or overpayment to Florida (subtract Line 17 from Line 16) – Enter on Line 19, Part IV |

18.___________________________ |

|||||

PART IV CALCULATION OF AMOUNT DUE OR OVERPAYMENT |

|

|

|

||||

19. |

Tax due or overpayment (if overpayment, enter on Line 23) |

|

|

19.___________________________ |

|||

20. |

Penalty if applicable (see instructions) |

|

|

20.___________________________ |

|||

21. |

Interest on underpayment if applicable (see instructions) |

|

|

21.___________________________ |

|||

22. |

Total amount due (add Lines 19, 20, and 21) |

|

|

22. |

|

|

|

|

|

|

|

||||

23. |

Overpayment to be refunded |

23. |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including any additional sheets attached, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer other than the personal representative is based on all information of which the preparer has any knowledge [ss. 92.525(1)(b); 213.37; 837.06, Florida Statutes (F.S.)].

__________________________________________________________________ |

__________________________________________________________________ |

||

Signature of personal representative |

Date |

Signature of preparer other than personal representative |

Date |

Name___________________________________________________________ |

Address _________________________________________________________ |

||

(Print name of preparer) |

|

(of preparer) |

|

Phone __________________________________________________________ |

City/State/ZIP ____________________________________________________ |

||

(of preparer) |

|

(of preparer) |

|

|

|

|

|

ATTACH COPY OF FEDERAL ESTATE TAX RETURN (FORM 706 or

INSTRUCTIONS FOR FORM

R.10/13 Page 2

General Information

Florida’s estate tax is based on the allowable federal credit for state death taxes. Florida tax is imposed only on those estates subject to federal estate tax filing requirements and entitled to a credit for state death taxes (Chapter 198, F.S.). Estate tax is not due if a federal estate tax return (Form 706 or

Form

The requirement to file Form

Date of Death |

|

|

|

On or before December 31, 2004 |

Yes** |

|

|

On or after January 1, 2005 |

No |

|

|

**If required, Form

Due Dates and Extensions of Time

Form

us within 30 days of mailing the request and 30 days of receiving the federal approval. An extension of time to file does not extend the time to pay. Interest accrues on the Florida tax due from the original due date until paid.

Tax Paid to Other States

For Florida residents: if estate, inheritance, or other death taxes were properly paid to other states, proof of payment must be submitted to the Florida Department of Revenue. (Proof of payment means the final certificate of payment showing the specific amounts of tax, penalty, or interest assessed and paid.)

*Social Security Numbers

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identifiers for the administration of Florida’s taxes. SSNs obtained for tax administration purposes are confidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public records. Collection of your SSN is authorized under state and federal law. Visit our Internet

site at floridarevenue.com and select “Privacy Notice” for more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

Where to File

Mail your completed

Tallahassee, FL

If you are requesting a nontaxable certificate, include the $5.00 fee.

Signature

The personal representative must sign the return declaration under penalties of perjury. If someone else prepares the return, the preparer must also sign the return.

Amending Form

If you must change a return that has already been filed, you must complete another Form

Penalties and Interest

Penalties – If tax is not paid by the due date (or approved extension date) a late payment penalty of 10% of the unpaid tax is due. After 30 days, the late penalty increases to 20%. An added penalty of 10% per month up to a maximum of 50% of the tax due is imposed if the unpaid tax is due to negligence or intentional disregard. A fraud penalty of 100% of the tax due is imposed if the unpaid tax is due to willful intent to defraud. However, the Department of Revenue is authorized to compromise or settle these penalties pursuant to section 213.21, F.S.

Interest – Interest is due on late payments from the due date until paid. Interest rates are updated January 1 and July 1 of each year. To obtain current interest rates, visit our website at floridarevenue.com.

Need Assistance?

Information and forms are available on our Internet site at

floridarevenue.com.

If you have any questions, you may contact Taxpayer Services at

For a written reply to your tax questions, write:

Taxpayer Services MS

Florida Department of Revenue

5050 W Tennessee St

Tallahassee, FL

For federal estate tax information or forms, visit the IRS website at www.irs.gov.

| Fact Name | Details |

|---|---|

| Form Title | The official name of the form is the Florida Estate Tax Return, designated as F-706. |

| Governing Law | The form is governed by Chapter 198 of the Florida Statutes. |

| Filing Requirement | Form F-706 is required if the decedent's date of death is on or before December 31, 2004. |

| Due Date | The form and payment are due within 9 months after the decedent's death. |

| Extension Policy | Florida grants extensions for filing and payment that align with IRS approved extensions. |

| Amended Returns | If changes are needed, a new Form F-706 must be filed, indicating that it is an amended return. |

| Social Security Numbers | SSNs are collected for tax administration and are confidential under Florida law. |

| Payment to Other States | Proof of any estate taxes paid to other states must be submitted with the form. |

| Penalties for Late Payment | A late payment penalty starts at 10% and can increase to 50% depending on the circumstances. |

| Contact Information | For assistance, taxpayers can contact the Florida Department of Revenue at 850-488-6800. |

Completing the Florida F 706 form is an important step in managing estate taxes. Ensure that you have all necessary documents and information ready before starting. Follow these steps to fill out the form accurately.

What is the Florida F 706 form?

The Florida F 706 form is the Florida Estate Tax Return. It is required for estates that meet specific criteria related to federal estate tax filing requirements. This form helps determine the estate tax due to the state of Florida and must be filed by the personal representative of the decedent's estate.

Who needs to file the F 706 form?

Filing the F 706 form is necessary for estates of Florida residents, nonresidents, and nonresident aliens with Florida property if a federal estate tax return (Form 706 or 706-NA) is required. If the decedent passed away on or before December 31, 2004, the form must be filed. However, if the date of death is on or after January 1, 2005, no filing is required unless there is a federal estate tax obligation.

What is the due date for filing the F 706 form?

The F 706 form and any payment due must be submitted within nine months of the decedent's death. This aligns with the due date for the federal estate tax return. If you need more time to file or pay, you must request an extension from the IRS, as Florida does not have a separate extension form.

What happens if I miss the filing deadline?

If the F 706 form is not filed by the deadline, penalties and interest may apply. A late payment penalty of 10% on the unpaid tax is incurred if the tax is not paid on time. This penalty increases to 20% after 30 days. Additionally, interest accrues on the tax due from the original due date until it is paid.

How do I amend a previously filed F 706 form?

To amend a filed F 706 form, complete a new form and check the box indicating it is an amended return. If the amendment is due to changes in your federal Form 706 or 706-NA, include a statement explaining the reasons for the amendment along with any relevant documents, such as correspondence from the IRS.

Where do I send the completed F 706 form?

Your completed F 706 form and payment should be mailed to the Florida Department of Revenue at the following address: PO Box 6460, Tallahassee, FL 32399-6460. If you are requesting a nontaxable certificate, be sure to include the $5.00 fee with your submission.

What should I do if I have questions about the F 706 form?

If you have questions or need assistance regarding the F 706 form, you can visit the Florida Department of Revenue's website at floridarevenue.com. You can also contact Taxpayer Services at 850-488-6800, Monday through Friday, excluding holidays. For written inquiries, send your questions to Taxpayer Services, MS 3-2000, Florida Department of Revenue, 5050 W Tennessee St, Tallahassee, FL 32399-0112.

Neglecting to Include Required Signatures: One of the most common mistakes is failing to ensure that the personal representative and any preparer sign the return. This oversight can lead to delays or rejections of the form.

Incorrectly Calculating the Estate Tax: Many individuals struggle with the calculations involved in determining the estate tax due. Errors in adding or subtracting the various lines can result in either underpayment or overpayment, both of which can have consequences.

Omitting Required Attachments: It is crucial to attach a copy of the federal estate tax return (Form 706 or 706-NA) when filing Form F-706. Failing to do so may lead to complications or additional scrutiny from the Florida Department of Revenue.

Inaccurate Reporting of Social Security Numbers: Providing incorrect social security numbers for the decedent or the personal representative can create significant issues. These numbers are vital for the identification and processing of the return.

Missing Deadlines: The deadline for filing Form F-706 is nine months after the decedent's death. Many people mistakenly believe they have more time or overlook the need for extensions, leading to penalties and interest.

The Florida F 706 form is essential for reporting estate taxes in Florida. However, several other documents are often needed to support the filing process or to clarify certain aspects of the estate. Below are five commonly used forms and documents that may accompany the Florida F 706 form.

Understanding the necessary forms and documents that accompany the Florida F 706 can streamline the estate tax filing process. Proper documentation ensures compliance with state regulations and can ease the burden on the personal representative handling the estate. If there are any questions or uncertainties, seeking assistance from a tax professional or the Florida Department of Revenue can be beneficial.

The Florida F 706 form is primarily used for reporting estate taxes. Several other documents serve similar purposes in different contexts or jurisdictions. Below is a list of documents that share similarities with the Florida F 706 form:

When filling out the Florida F-706 form, it’s essential to approach the task with care and attention to detail. Here’s a list of ten dos and don’ts to guide you through the process:

By following these guidelines, you can navigate the Florida F-706 form process more smoothly and effectively, ensuring compliance and minimizing potential complications.

This form applies to Florida residents, nonresidents, and nonresident aliens with property in Florida. Everyone who meets these criteria must file if they are required to file a federal estate tax return.

If there is no federal estate tax filing requirement, you do not need to file the Florida F 706 form. Instead, use Form DR-312 to remove any estate tax liens.

The form and payment are due within nine months after the decedent’s death, aligning with the federal estate tax return due date.

To amend, simply complete another F 706 form and check the amended return box. Include a statement explaining the changes.

If you overpay, you can enter the amount on Line 23 of the form to request a refund.

It is essential to attach a signed copy of the federal Form 706 or 706-NA when filing the F 706 form.

You can request an extension from the IRS, and Florida will grant the same extension for filing and payment. Just ensure you send the necessary documents to Florida within the required timeframe.

Currently, the Florida Department of Revenue does not allow electronic submissions for the F 706 form. It must be mailed in.

Social Security numbers collected for tax purposes are confidential and protected under Florida law. They are not public records.