The Delaware Promissory Note form serves as a crucial document in the realm of personal and business finance, facilitating the borrowing and lending of money between parties. This legal instrument outlines the terms under which a borrower agrees to repay a specified amount of money to a lender, typically including details such as the principal amount, interest rate, repayment schedule, and any applicable late fees. Additionally, it may address the consequences of default, providing clarity on the rights and obligations of both parties. Importantly, the form can be tailored to meet the specific needs of the transaction, allowing for flexibility in terms of payment arrangements and security interests. By understanding the essential components of the Delaware Promissory Note, individuals and businesses can better navigate their financial agreements, ensuring that all parties are on the same page and minimizing potential disputes down the line.

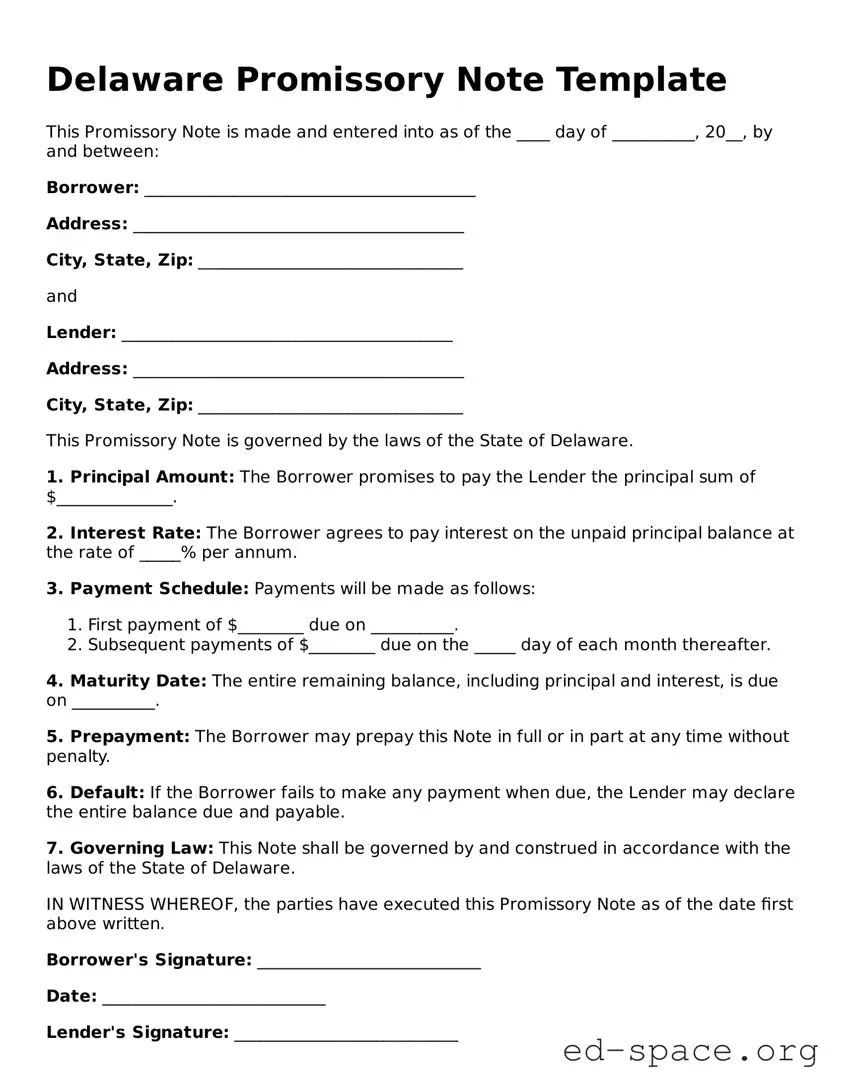

Delaware Promissory Note Template

This Promissory Note is made and entered into as of the ____ day of __________, 20__, by and between:

Borrower: ________________________________________

Address: ________________________________________

City, State, Zip: ________________________________

and

Lender: ________________________________________

Address: ________________________________________

City, State, Zip: ________________________________

This Promissory Note is governed by the laws of the State of Delaware.

1. Principal Amount: The Borrower promises to pay the Lender the principal sum of $______________.

2. Interest Rate: The Borrower agrees to pay interest on the unpaid principal balance at the rate of _____% per annum.

3. Payment Schedule: Payments will be made as follows:

4. Maturity Date: The entire remaining balance, including principal and interest, is due on __________.

5. Prepayment: The Borrower may prepay this Note in full or in part at any time without penalty.

6. Default: If the Borrower fails to make any payment when due, the Lender may declare the entire balance due and payable.

7. Governing Law: This Note shall be governed by and construed in accordance with the laws of the State of Delaware.

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: ___________________________

Date: ___________________________

Lender's Signature: ___________________________

Date: ___________________________

| Fact Name | Details |

|---|---|

| Definition | A Delaware Promissory Note is a written promise to pay a specific amount of money to a designated person at a specified time. |

| Governing Law | The Delaware Uniform Commercial Code (UCC) governs promissory notes in Delaware. |

| Parties Involved | Typically, there are two parties: the borrower (maker) and the lender (payee). |

| Interest Rate | The note may specify an interest rate, which can be fixed or variable, but must comply with state usury laws. |

| Payment Terms | Payment terms should clearly outline the due date, payment schedule, and any late fees. |

| Signatures | Both parties must sign the note for it to be legally binding, though notarization is not required. |

| Enforceability | A properly executed promissory note is enforceable in court, provided it meets all legal requirements. |

Once you have the Delaware Promissory Note form in front of you, it’s time to complete it with the necessary details. This document will require specific information about the parties involved and the terms of the loan. Carefully following the steps below will help ensure that the form is filled out correctly.

After completing the form, review it for accuracy. Make sure all necessary information is included and that both parties have signed. Keeping a copy for your records is also recommended.

What is a Delaware Promissory Note?

A Delaware Promissory Note is a legal document in which one party, known as the borrower, agrees to pay a specific amount of money to another party, known as the lender, under agreed-upon terms. This document outlines the repayment schedule, interest rate, and any other conditions related to the loan.

Who can use a Delaware Promissory Note?

Any individual or business entity can utilize a Delaware Promissory Note. It is commonly used in personal loans, business loans, and real estate transactions. Both lenders and borrowers benefit from this formal agreement, as it provides clarity and protection for both parties involved.

What are the key components of a Delaware Promissory Note?

A typical Delaware Promissory Note includes several essential components: the names and addresses of the borrower and lender, the principal amount borrowed, the interest rate, the repayment schedule, and any penalties for late payments. Additionally, it may outline any collateral securing the loan.

Is a Delaware Promissory Note legally binding?

Yes, a properly executed Delaware Promissory Note is legally binding. Once signed by both parties, it serves as a contract that can be enforced in court if necessary. It is crucial for both parties to understand the terms before signing to ensure that they are in agreement.

Do I need a lawyer to create a Delaware Promissory Note?

While it is not mandatory to have a lawyer draft a Delaware Promissory Note, consulting with one is advisable. A lawyer can help ensure that the document complies with state laws and adequately protects your interests. This is especially important for larger loans or complex agreements.

Can a Delaware Promissory Note be modified after it is signed?

Yes, a Delaware Promissory Note can be modified, but both parties must agree to the changes. It is best to document any modifications in writing and have both parties sign the amended note to avoid future disputes. Verbal agreements are not sufficient for changes to be enforceable.

What happens if the borrower defaults on the loan?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit or pursuing collections. The specific remedies available will depend on the terms outlined in the Promissory Note and Delaware law.

Are there any tax implications related to a Delaware Promissory Note?

Yes, there can be tax implications for both the borrower and lender. The lender may need to report the interest income received, while the borrower may be able to deduct interest payments under certain circumstances. It is advisable to consult a tax professional to understand the specific implications for your situation.

How can I ensure my Delaware Promissory Note is enforceable?

To ensure that your Delaware Promissory Note is enforceable, make sure it is clear, complete, and signed by both parties. Include all necessary terms and conditions, and consider having it notarized. Keeping accurate records of all payments and communications related to the loan can also strengthen your position if enforcement becomes necessary.

Omitting Essential Information: One common mistake is failing to include all necessary details, such as the names of both the borrower and the lender. This can lead to confusion and potential disputes in the future.

Incorrectly Stating the Loan Amount: It is crucial to accurately specify the total loan amount. Errors in this figure can create complications, especially if the borrower defaults on the loan.

Not Including Interest Terms: Some individuals neglect to outline the interest rate or terms of repayment. Without this information, it may be difficult to enforce the agreement later.

Failing to Sign the Document: A promissory note is not valid unless it is signed by both parties. Forgetting to sign can render the entire document unenforceable.

When dealing with a Delaware Promissory Note, several other forms and documents may be necessary to ensure clarity and legal compliance. Each of these documents serves a specific purpose in the lending process and can help protect the interests of both the lender and the borrower.

Understanding these documents can significantly enhance the borrowing experience, ensuring that all parties are aware of their rights and responsibilities. Proper documentation not only fosters trust but also provides legal safeguards throughout the lending process.

The Promissory Note is a key financial document that shares similarities with several other legal documents. Each serves a unique purpose but often overlaps in function and intent. Below is a list of documents that resemble the Promissory Note:

When filling out the Delaware Promissory Note form, it's important to follow certain guidelines to ensure accuracy and legality. Here are some things you should and shouldn't do:

Understanding the Delaware Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are nine common misconceptions:

Awareness of these misconceptions can help individuals navigate the complexities of promissory notes more effectively. Always consider seeking guidance if there are uncertainties about the terms or implications.

When it comes to using a Delaware Promissory Note, understanding the essentials can make the process smoother and more effective. Here are some key takeaways to keep in mind:

By following these guidelines, you can navigate the process of creating and using a Delaware Promissory Note with confidence.