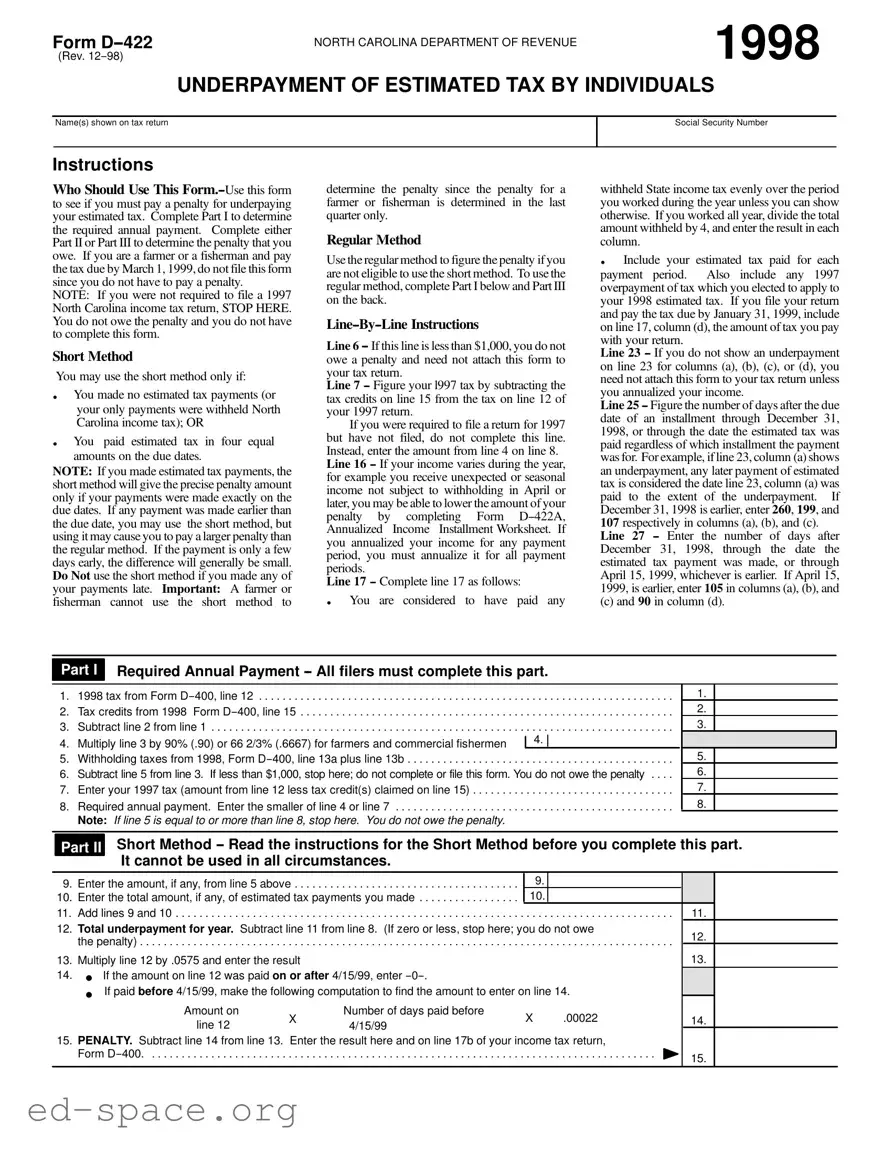

The D 422 North Carolina form is an essential tool for individuals who need to assess whether they owe a penalty for underpaying their estimated tax. This form guides users through a series of steps to determine their required annual payment and any penalties that may apply. It consists of multiple parts, including a short method for those who meet specific criteria, and a regular method for others. Farmers and fishermen have unique considerations, as they may not need to file if they pay their taxes by a certain date. The form requires detailed calculations, including tax credits, withholding amounts, and payment deadlines. It's crucial to follow the instructions carefully, as the consequences of underpayment can lead to penalties that vary based on the timing of payments. Overall, understanding and correctly completing the D 422 form can help individuals avoid unnecessary financial burdens while ensuring compliance with North Carolina tax regulations.

(Rev. |

|

1998 |

Form |

NORTH CAROLINA DEPARTMENT OF REVENUE |

|

UNDERPAYMENT OF ESTIMATED TAX BY INDIVIDUALS

Name(s) shown on tax return

Social Security Number

Instructions

Who Should Use This

NOTE: If you were not required to file a 1997 North Carolina income tax return, STOP HERE. You do not owe the penalty and you do not have to complete this form.

Short Method

You may use the short method only if:

. You made no estimated tax payments (or your only payments were withheld North Carolina income tax); OR

. You paid estimated tax in four equal amounts on the due dates.

NOTE: If you made estimated tax payments, the short method will give the precise penalty amount only if your payments were made exactly on the due dates. If any payment was made earlier than the due date, you may use the short method, but using it may cause you to pay a larger penalty than the regular method. If the payment is only a few days early, the difference will generally be small. Do Not use the short method if you made any of your payments late. Important: A farmer or fisherman cannot use the short method to

determine the penalty since the penalty for a farmer or fisherman is determined in the last quarter only.

Regular Method

Use the regular method to figure the penalty if you are not eligible to use the short method. To use the regular method, complete Part I below and Part III on the back.

Line 6

Line 7

If you were required to file a return for 1997 but have not filed, do not complete this line. Instead, enter the amount from line 4 on line 8.

Line 16

Line 17

. You are considered to have paid any

withheld State income tax evenly over the period you worked during the year unless you can show otherwise. If you worked all year, divide the total amount withheld by 4, and enter the result in each column.

. Include your estimated tax paid for each

payment period. Also include any 1997 overpayment of tax which you elected to apply to your 1998 estimated tax. If you file your return and pay the tax due by January 31, 1999, include on line 17, column (d), the amount of tax you pay with your return.

Line 23

Line 25

Line 27

(c) and 90 in column (d).

Part I

Required Annual Payment

1. |

1998 tax from Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

2. |

Tax credits from 1998 Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

3. |

Subtract line 2 from line 1 |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

4. |

Multiply line 3 by 90% (.90) or 66 2/3% (.6667) for farmers and commercial fishermen |

|

4. |

|

|

|

|||

5. |

Withholding taxes from 1998, Form |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

6. |

Subtract line 5 from line 3. If less than $1,000, stop here; do not complete or file this form. You do not owe the penalty . . . . |

|||

7. |

Enter your 1997 tax (amount from line 12 less tax credit(s) claimed on line 15) |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

8. |

Required annual payment. Enter the smaller of line 4 or line 7 |

|

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

|

Note: If line 5 is equal to or more than line 8, stop here. You do not owe the penalty. |

|

|

|

1.

2.

3.

5.

6.

7.

8.

Part II

Short Method

9. |

Enter the amount, if any, from line 5 above |

9. |

|

|

|||

10. |

Enter the total amount, if any, of estimated tax payments you made |

10. |

|

|

|||

11. |

Add lines 9 and 10 |

11. |

|||||

12. |

Total underpayment for year. Subtract line 11 from line 8. (If zero or less, stop here; you do not owe |

12. |

|||||

|

the penalty) |

||||||

|

|

||||||

13. |

Multiply line 12 by .0575 and enter the result |

|

|

|

13. |

||

14. |

. |

If the amount on line 12 was paid on or after 4/15/99, enter |

|

|

|

||

|

. |

If paid before 4/15/99, make the following computation to find the amount to enter on line 14. |

|

||||

|

Amount on |

|

Number of days paid before |

|

|

|

|

|

|

X |

X |

.00022 |

14. |

||

|

|

line 12 |

4/15/99 |

||||

|

|

|

|

|

|

||

15. |

PENALTY. Subtract line 14 from line 13. |

Enter the result here and on line 17b of your income tax return, |

|

||||

|

Form |

15. |

|||||

|

|

|

|

|

|

|

|

Form

Page 2

|

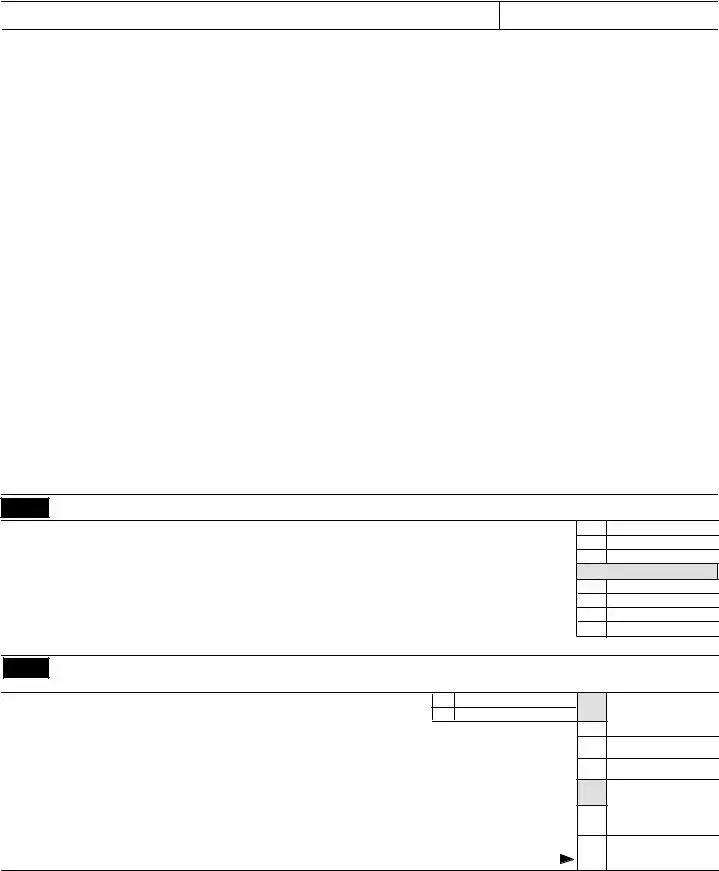

Part III |

Regular Method |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section A |

|

|

Payment Due Dates |

|

||

|

|

(a) |

(b) |

(c) |

(d) |

||

|

|

|

|

4/15/98 |

6/15/98 |

9/15/98 |

1/15/99 |

16.Divide line 8 by 4 and enter the result in each column. Exception: If you use the annualized income

|

ment method, complete Form |

|

16. |

|

|

||||

17. |

Income Installment Worksheet) and check this box. |

|

|

|

|

|

|||

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

Estimated tax paid and tax withheld. For column (a) only, |

|

|

|

|

|

||||

|

|

|

|

|

|

||||

|

enter the amount from line 17 on line 21. (If line 17 is |

|

|

|

|

|

|||

|

equal to or more than line 16 for each payment period, |

17. |

|

|

|||||

|

. . . .stop here; you do not owe the penalty.) |

|

|

||||||

|

|

|

|||||||

|

Complete lines 18 through 24 of one column before |

|

|

|

|

|

|||

|

going to the next column. |

|

|

|

|

|

|||

18. |

Enter amount, if any, from line 24 of previous colum . . . . |

18. |

|

|

|||||

|

|

19. |

|

|

|||||

19. |

Add lines 17 and 18 |

|

|

||||||

20. |

Add amounts on lines 22 and 23 of the previous column |

|

|

and enter the result |

20. |

21.Subtract line 20 from line 19 and enter the result. If zero

or less, enter zero. (For column (a) only, enter the |

|

amount from line 17) |

21. |

22.Remaining underpayment from previous period. If the

amount on line 21 is |

||

and enter the result. Otherwise, enter |

. . . . 22. |

|

23. Underpayment. If line 16 is larger than or equal |

to |

|

line 21, subtract line 21 from line 16 and enter the |

||

result. Enter 0 on line 18 of the next column and go to |

||

line 19. Otherwise, go to line 24 |

. . . . 23. |

|

24.Overpayment. If line 21 is larger than line 16, subtract

|

|

line 16 from line 21 and enter the result. Then go to |

|

|

|

|

|

|

|||||

|

|

line 18 of next column. . |

. . . . . . . . . . . . . . . . . . . . |

. . . . |

. . . . 24. |

|

|

|

|

||||

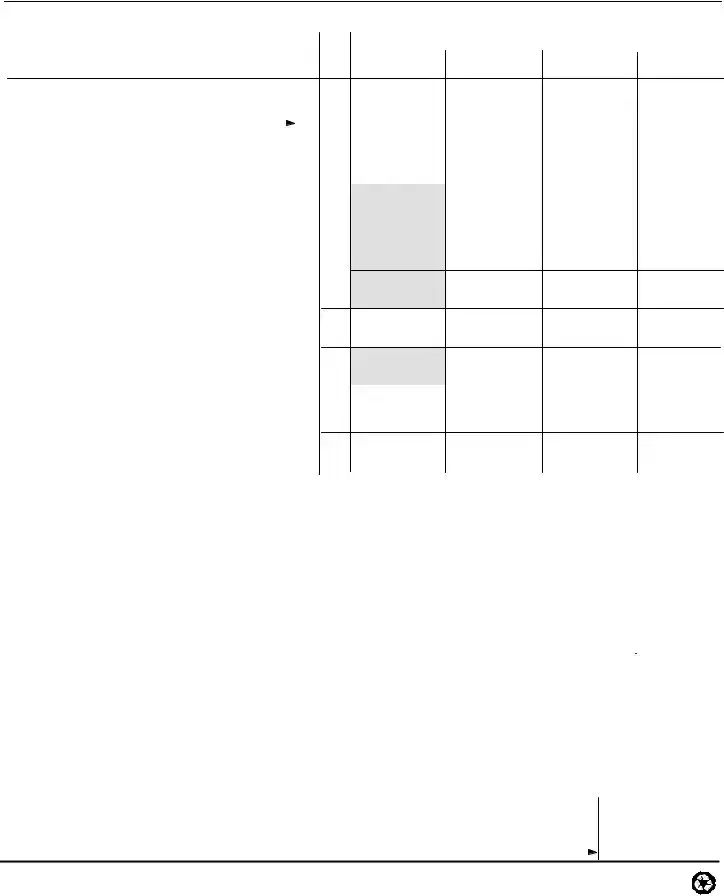

|

Section B Figure the Penalty (Complete lines 25 through 28 of one column before going to the next |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

April 15, 1998 December 31, 1998 |

|

|

|

|

|

|

|

||||

|

|

|

|

|

4/15/98 |

6/15/98 |

9/15/98 |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

25. Number of days after the date shown above line 25 through |

|

Days: |

Days: |

Days: |

|

|||||||

|

|

the date the amount on line 23 was paid or |

12/31/98, |

|

|

|

|

|

|||||

|

|

whichever is earlier. |

. . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . |

25. |

|

|

|

|

|||

|

26. |

Underpayment |

X |

|

Number of days |

X |

.09 |

|

|

|

|

|

|

|

|

on line 23 |

|

on line 25 |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(see instructions) |

|

365 |

|

|

|

26. |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

January 1, 1999 |

April 15, 1999 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

12/31/98 |

12/31/98 |

12/31/98 |

1/15/99 |

|||||

|

|

|

|

|

|

|

|

|

|

||||

|

27. Number of days after the date shown above line 27 through |

|

Days: |

Days: |

Days: |

Days: |

|||||||

|

|

the date the amount on line 23 was paid or |

4/15/99, |

|

|

|

|

|

|||||

|

|

whichever is earlier. |

. . . . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . |

27. |

|

|

|

|

|||

|

28. |

Underpayment |

X |

|

Number of days |

X |

.08 |

|

|

|

|

|

|

|

|

on line 23 |

|

on line 27 |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(see instructions) |

|

365 |

|

|

|

28. |

$ |

$ |

$ |

$ |

|

|

|

|

|

|

|

|

|

|

|||||

29.Penalty (add amounts on line 26 and 28). Enter here and on line 17b of your individual income tax return,

Form

29.

| Fact Name | Details |

|---|---|

| Purpose | The D-422 form is used to determine if individuals owe a penalty for underpaying estimated taxes. |

| Eligibility | This form is for individuals who may have underpaid their estimated tax, excluding farmers and fishermen who meet certain criteria. |

| Governing Law | North Carolina General Statutes, specifically N.C. Gen. Stat. § 105-163.2. |

| Short Method | The short method can only be used if no estimated tax payments were made or if they were made in four equal installments. |

| Regular Method | Individuals not eligible for the short method must use the regular method to calculate their penalty. |

| Penalty Calculation | The penalty is calculated based on the amount of underpayment and the number of days the payment was late. |

| Annualized Income | Taxpayers with varying income may use Form D-422A to annualize their income, potentially lowering their penalty. |

| Filing Deadline | Taxpayers must file and pay any owed taxes by January 31, 1999, to avoid penalties. |

| Exemption from Filing | If the required annual payment is less than $1,000, the taxpayer does not owe a penalty and does not need to file the form. |

Filling out the D 422 North Carolina form requires careful attention to detail. After completing the form, you will have a clearer understanding of whether you owe a penalty for underpaying your estimated tax. Follow these steps to ensure accurate completion.

What is the purpose of the D 422 North Carolina form?

The D 422 form is used by individuals in North Carolina to determine if they owe a penalty for underpaying their estimated tax. By completing this form, taxpayers can assess their required annual payment and calculate any penalties that may apply. It helps ensure compliance with state tax regulations and allows individuals to understand their tax obligations better.

Who needs to use this form?

This form should be used by individuals who are required to pay estimated taxes and want to check if they underpaid. If you did not need to file a North Carolina income tax return for the previous year, you do not need to fill out this form. Additionally, farmers and fishermen who pay their taxes by March 1, 1999, are exempt from filing this form as they do not incur a penalty.

What are the short and regular methods for calculating penalties?

The short method can be used if you made no estimated tax payments or if you paid estimated tax in four equal amounts on the due dates. However, if any payments were made late or if you made payments early, using the short method may not provide an accurate penalty amount. The regular method is used when the short method is not applicable. It requires filling out additional sections of the form to calculate the penalty based on your specific tax situation.

What should I do if my income varies throughout the year?

If your income fluctuates, such as receiving seasonal income not subject to withholding, you may be able to reduce your penalty. In this case, you can complete Form D-422A, the Annualized Income Installment Worksheet, to adjust your calculations. It’s important to annualize your income for all payment periods if you choose this method.

What happens if my calculated underpayment is less than $1,000?

If your calculated underpayment is less than $1,000, you do not owe a penalty and do not need to attach the D 422 form to your tax return. This threshold is significant because it indicates that your estimated tax payments were sufficient to avoid penalties. Always ensure to check this line carefully to avoid unnecessary filings.

Incorrect Personal Information: Failing to accurately fill in the name(s) and Social Security Number can lead to processing delays or issues with your tax return.

Not Understanding Eligibility: Some individuals mistakenly complete the form even when they are not required to file it. If you weren’t required to file a 1997 North Carolina income tax return, you should stop here.

Using the Wrong Method: People often select the short method when they are not eligible. This method is only appropriate if you made no estimated tax payments or paid them on time in four equal amounts.

Late Payments: If any estimated tax payments were made late, individuals should not use the short method. This mistake can result in a larger penalty than necessary.

Incorrect Line Calculations: Miscalculating the amounts on key lines, such as line 7 (1997 tax) or line 8 (required annual payment), can lead to incorrect penalty assessments.

Ignoring Annualized Income: If your income varies throughout the year, failing to complete Form D-422A can lead to a higher penalty than necessary.

Overlooking Underpayment Lines: Individuals sometimes forget to check line 23 for underpayment. If there is no underpayment, you do not need to attach this form to your tax return.

Misunderstanding Payment Dates: Confusion about the due dates for estimated tax payments can lead to incorrect calculations on lines 25 and 27, affecting the penalty amount.

Failing to Attach Required Documentation: Not including the D-422 form when it is required can result in penalties being assessed incorrectly.

Not Reviewing Instructions: Skipping the detailed instructions can lead to errors in the form completion. Each line has specific requirements that must be followed closely.

The D-422 form is a crucial document for individuals in North Carolina who may face penalties for underpaying estimated taxes. Several other forms and documents are commonly used alongside the D-422 to ensure compliance with tax obligations. Below is a list of these related documents, each described briefly for clarity.

Understanding these forms and their purposes can help individuals navigate their tax responsibilities more effectively. Each document plays a vital role in ensuring compliance with North Carolina tax laws and minimizing potential penalties.

The D 422 North Carolina form, which addresses underpayment of estimated tax by individuals, shares similarities with several other tax-related documents. Below is a list of four forms that are comparable, along with a brief explanation of how they are alike:

When filling out the D-422 North Carolina form, it's essential to be careful and thorough. Here’s a handy list of things to do and avoid, ensuring you complete the form correctly and efficiently.

Understanding the D 422 North Carolina form can be challenging, especially with the various misconceptions surrounding it. Here are seven common misunderstandings about this form:

This is not true. If your required annual payment is less than $1,000, you do not owe a penalty and do not need to file this form.

While it is true that farmers and fishermen have different rules, they must still file the form if they do not pay their tax by the specified deadline, even if they are exempt from penalties if paid on time.

This is misleading. The short method can only be used under specific circumstances. If any payment was made late or early, it might result in a larger penalty than using the regular method.

If you were not required to file a tax return for the previous year, you do not owe a penalty and do not need to complete the D 422 form.

This is incorrect. The short method can only be used if you made no estimated tax payments or if you made equal payments on time. Late payments disqualify you from using this method.

For those who owe a penalty for underpayment, completing this form is mandatory. It helps determine the exact penalty amount owed.

This is not the case. Any individual who underpays their estimated tax, regardless of income level, may need to file this form to assess potential penalties.

Being informed about these misconceptions can help ensure compliance with tax regulations and avoid unnecessary penalties. If there are any uncertainties, seeking guidance from a tax professional can provide clarity and peace of mind.

Understanding the D-422 North Carolina Form is essential for individuals who may face penalties for underpaying their estimated tax. Here are key takeaways to help navigate this process: