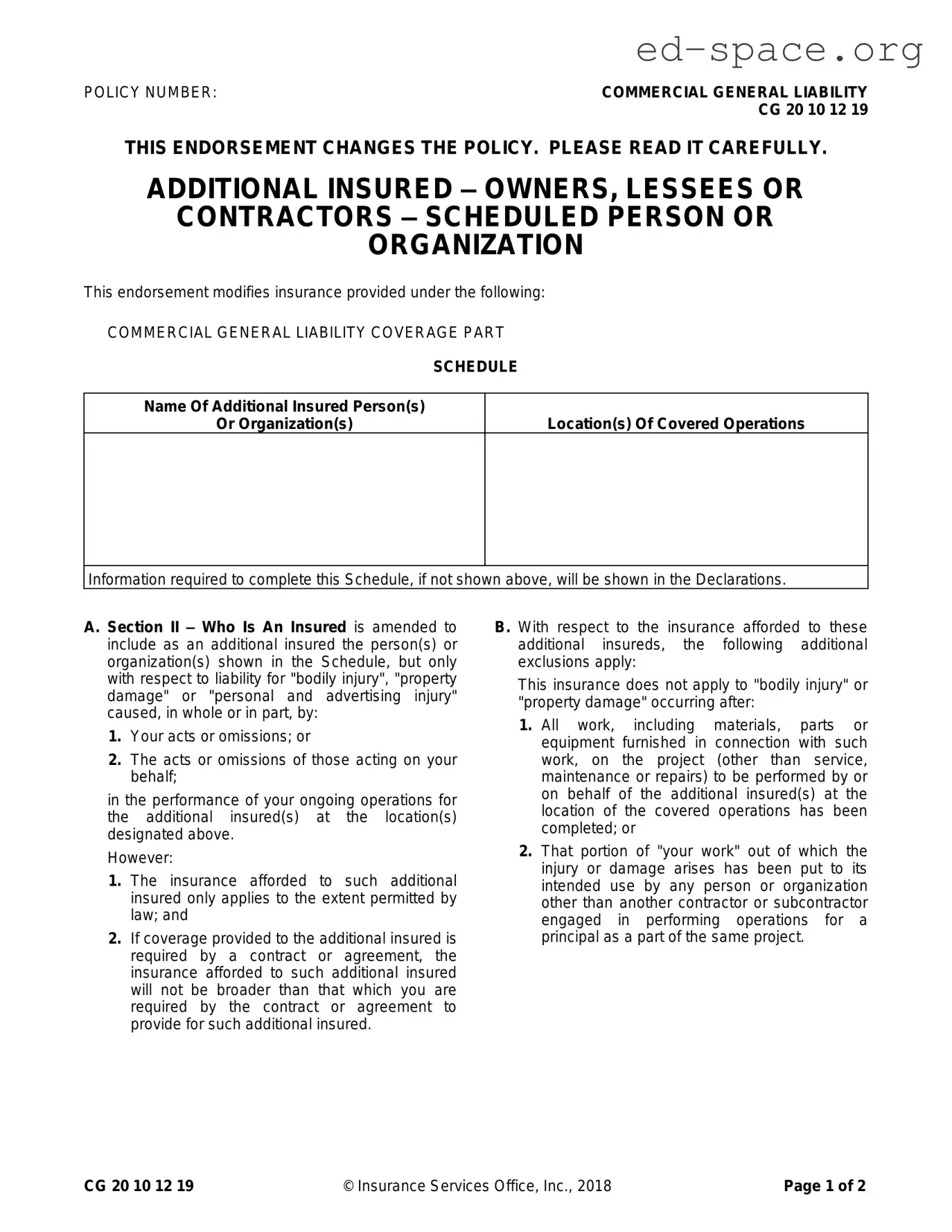

In the realm of insurance, endorsements play a crucial role in tailoring policies to specific needs, and the CG 20 10 07 04 Liability Endorsement form is a prime example of such an adaptation. Used widely in commercial general liability (CGL) insurance, this form extends coverage to additional insureds, typically owners, lessees, or contractors, specifying the conditions under which these parties are covered. The endorsement is activated when certain acts or omissions, either by the policyholder or those acting on their behalf, lead to bodily injury, property damage, or personal and advertising injury during the policyholder's ongoing operations for the additional insured at a specific location. However, it's important to note the nuanced limitations that accompany this added protection. Coverage is contingent upon the boundaries established by law and preexisting contractual agreements, ensuring that the scope of coverage for additional insureds does not exceed what is legally mandated or what was contractually agreed upon. Furthermore, specific exclusions and limitations apply, particularly concerning when the coverage ceases to be effective—such as upon the completion of work or when the completed work has been used for its intended purpose, emphasizing the temporal and operational boundaries of this endorsement. Additionally, it adjusts the general liability coverage part to potentially limit the insurer's financial exposure, ensuring that the maximum payout does not exceed the limits defined either by a related contract or agreement or by the policy itself, whichever is less. Thus, the CG 20 10 07 04 Liability Endorsement form introduces a significant modification to standard liability policies, necessitating a careful examination by those it seeks to protect.

| Fact Name | Description |

|---|---|

| Endorsement Title | Additional Insured – Owners, Lessees or Contractors – Scheduled Person or Organization |

| Document Identification | CG 20 10 12 19 |

| Purpose of Endorsement | Modifies the Commercial General Liability Coverage to include additional insured entities as specified in the schedule. |

| Coverage Scope | Covers liability for bodily injury, property damage, or personal and advertising injury caused by the named insured or those acting on their behalf. |

| Limitations | Coverage for additional insureds is only to the extent permitted by law and cannot exceed the scope required by any contract or agreement. |

| Additional Exclusions | Excludes coverage for injuries or damage occurring after all work at the site is completed or when the work is put to its intended use, with certain conditions. |

| Limits of Insurance Modification | The maximum payable amount for additional insureds is determined by the contract or agreement or the applicable insurance limits, whichever is less, without increasing overall policy limits. |

| Governing Law | Subject to limitations and requirements of applicable law and specific terms of related contracts or agreements. |

Filling out the CG 20 10 07 04 Liability Endorsement form is a crucial step in adjusting your commercial general liability insurance to cover additional insured persons or organizations. This form allows you to extend your liability coverage to others (e.g., owners, lessees, or contractors) associated with your business operations. The form specifically modifies who is considered an insured under the policy, making it necessary to be meticulous when completing it to ensure that all necessary parties are covered, and the extent of the coverage is clear. The process involves specifying the additional insured, detailing the operations covered, and understanding the scope and limitations of this extension. The following steps will guide you through filling out the form accurately.

After submitting the CG 20 10 07 04 Liability Endorsement form, the added coverage will take effect per the terms outlined in your commercial general liability policy and the endorsement itself. It’s advisable to follow up with your insurance provider to confirm the endorsement’s incorporation into your policy and to clarify any subsequent changes or additional requirements. Ensuring that your policy accurately reflects your coverage needs, including any additional insureds, is paramount in maintaining adequate protection for your business operations.

What is the purpose of the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form is designed to amend a commercial general liability (CGL) policy by specifying additional insureds. Essentially, it extends coverage to other individuals or organizations (as outlined in the policy’s schedule) for liability arising from the policyholder’s actions or the actions of those working on their behalf. This is crucial in many business arrangements, such as leases or contracts where a party requires added protection against potential claims.

Who can be added as an additional insured under this endorsement?

Under the CG 20 10, additional insureds can include owners, lessees, or contractors that the policyholder specifies in the policy’s schedule. These entities become covered only concerning liability for bodily injury, property damage, or personal and advertising injury that originates, completely or partially, from the policyholder’s operations or those conducted on their behalf. The addition is subject to the conditions and exclusions set forth in the endorsement and the underlying policy.

Are there any exclusions or limitations to the coverage extended to additional insureds?

Yes, the endorsement contains specific exclusions and limitations on the coverage extended to additional insureds. For instance, additional insureds are covered only to the extent the law allows and only within the scope required by any contract or agreement necessitating their addition. Coverage does not apply to injuries or damages occurring after all work at the designated location is completed or after completed work has been put to its intended use. Additionally, the most insurance companies will pay on behalf of an additional insured is the amount required by contract or the limits of the insurance, whichever is less, without increasing the overall limits of insurance.

What happens if the coverage required by a contract exceeds the policy limit?

When the coverage stipulated by a contract or agreement exceeds the policy limit, the insurance afforded to the additional insured will not surpass the available policy limits. In such instances, the insurance provided will adhere to the lesser amount between what is required by the contract or agreement and what the policy can offer within its limits. The endorsement explicitly states that it does not increase the policy’s applicable limits of insurance.

How does this endorsement affect the policy’s limit of insurance?

The CG 20 10 endorsement affects the policy’s limit of insurance by stating that any coverage extended to additional insureds under a contract or agreement will not exceed the lesser of the required insurance amount or the policy’s existing limits of insurance. This means that the endorsement provides added protection for specified additional insureds without enlarging the policy’s overall coverage limit. The insurer’s maximum payout on behalf of the additional insured, therefore, is bound by the existing limits set forth in the policy, ensuring that the primary policyholder’s coverage is not inadvertently diminished.

Filling Out the Schedule Incorrectly: A significant mistake is providing inaccurate information in the "SCHEDULE" section which includes the name of the additional insured person(s) or organization(s) and the location(s) of covered operations. Precision is critical as this section identifies who is being afforded coverage and where. Errors in these details can lead to disputes over whether the policy extends to claims involving the additional insured or the location in question.

Overlooking the Conditions Required for Coverage: It is a common oversight not to fully comprehend the conditions under which the additional insured is covered. The coverage is explicitly for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by the policyholder's or their operative's actions in the performance of ongoing operations. Neglecting the scope of this coverage can result in misconceptions about the protection afforded under the policy.

Misunderstanding the Scope of Coverage: There is often a misconception that the insurance provided to the additional insured is unlimited or broader than it actually is. The document specifies that the insurance afforded will not extend beyond the scope required by law or a specified contract or agreement. Assuming coverage without recognizing these limitations can lead to a false sense of security for the additional insured.

Not Recognizing Additional Exclusions: Individuals frequently miss the section outlining additional exclusions to the insurance provided to additional insureds. This oversight can be critical, as it details situations where coverage does not apply, such as "bodily injury" or "property damage" occurring after the completion of certain works or when the work has been put to its intended use. Awareness and understanding of these exclusions are necessary to comprehensively grasp the extents and limits of the provided coverage.

In conclusion, when completing the CG 20 10 07 04 Liability Endorsement form, attention to detail and a thorough understanding of the terms are indispensable. Properly indicating the additional insured and the covered locations, understanding the coverage's scope and its conditions, and recognizing the pertinent exclusions are pivotal in ensuring that all parties involved have the necessary protection as intended by the policy.

When handling matters of commercial general liability, the CG 20 10 07 04 Liability Endorsement form is a pivotal document, particularly for granting additional insured status under specific circumstances. However, this form doesn't stand alone in the context of risk management and insurance documentation. Other forms and documents often accompany it to provide a comprehensive risk mitigation strategy and to comply with contractual obligations. Each of these documents plays a critical role in ensuring that coverage is aligned with the requirements of the involved parties.

In summary, while the CG 20 10 07 04 Liability Endorsement form plays a crucial role in defining the scope of liability coverage for additional insureds, it is frequently used alongside other documents to provide a fuller picture of the insurance protection in place. Together, these forms and documents create a network of protections that meet the needs of all parties involved, ensuring compliance with legal and contractual obligations while managing risk effectively.

CG 20 33 – Additional Insured – Owners, Lessees or Contractors – Automatic Status for Other Parties When Required in a Written Construction Agreement: Similar to the CG 20 10 endorsement, the CG 20 33 form provides additional insured status to entities such as owners, lessees, or contractors when such status is required under a written construction agreement. Both forms extend coverage to additional insureds mainly in the scope of liability arising out of the named insured's work for the additional insured. However, CG 20 33 grants this status automatically to new parties under qualifying contracts without the need to specifically schedule each entity.

CG 20 37 – Additional Insured – Owners, Lessees or Contractors – Completed Operations: This endorsement is closely related to the CG 20 10 by offering additional insured status, but it specifically extends the coverage to completed operations. While CG 20 10 focuses on operations in progress, CG 20 37 ensures that the additional insured remains protected for liability issues arising from the completed work of the named insured. Both are essential in providing a comprehensive risk management strategy for projects involving multiple parties.

ISO Form CG 00 01 – Commercial General Liability (CGL) Policy: The CG 00 01 is the foundational document to which the CG 20 10 and other endorsements are attached. This form outlines the core coverages, exclusions, and limits of the commercial general liability policy. The CG 20 10 functions as an amendment to the CG 00 01, specifying changes to the who is an insured section to include additional insureds. Together, they create a full picture of the policy's scope.

CG 24 26 – Waiver of Transfer of Rights of Recovery Against Others to Us (Waiver of Subrogation): Though different in purpose, the CG 24 26 shares a connection with the CG 20 10. Both address specific needs within a contractual relationship, affecting the rights and coverage of parties involved in a project. The CG 24 26 waives the insurer's right to pursue cost recovery (subrogation) against a third party, often required in contracts to facilitate smoother operational relationships, similar to how the CG 20 10 facilitates additional insured status.

CG 21 39 – Contractual Liability Limitation: This endorsement modifies the coverage provided under the CG 00 01 form by limiting contractual liability, which fundamentally alters the policy similarly to the CG 20 10. The CG 21 39 restricts coverage for liability assumed under a contract or agreement, whereas the CG 20 10 expands the scope of who is considered an insured under the policy for certain liabilities. Both endorsements adjust the standard CGL policy to better fit the needs and agreements between parties involved in contractual relationships.

Filling out the CG 20 10 07 04 Liability Endorsement form requires attention to detail and an understanding of the requirements. Here are five recommendations for what should and should not be done when completing this form.

Do:

Do Not:

Many misunderstandings surround the CG 20 10 07 04 Liability Endorsement form. Here are ten common misconceptions and the truths behind them:

It provides blanket coverage for any third party. In reality, the endorsement specifically names additional insureds, offering them coverage only under certain conditions directly related to your actions or the actions of those working on your behalf.

The additional insured is covered for all types of liability. The truth is that coverage for additional insureds is limited to "bodily injury", "property damage", or "personal and advertising injury" that occurs as a result of the named insured's operations for the additional insured at designated locations.

Coverage is unlimited. The endorsement clearly stipulates that if coverage is mandated by a contract or agreement, the most that will be paid on behalf of the additional insured is either the required amount by contract or the limit available under the policy, whichever is less.

Coverage extends indefinitely after a project is completed. Coverage for bodily injury or property damage does not apply after all work on the project has been completed, or the completed work has been put to its intended use, except by another contractor or subcontractor working on the same project.

The form automatically extends coverage to subcontractors. The form does not extend coverage to subcontractors. The named additional insureds are explicitly listed in the schedule, and coverage is primarily designed for their protection concerning the named insured's operations.

Coverage under this endorsement is broader than the main policy. Coverage for additional insureds will not be broader than what the contract requires the primary policyholder to provide. It complements but does not surpass the scope of the main commercial general liability coverage.

Any contract or agreement can obligate coverage under this endorsement. While contracts or agreements can necessitate adding an additional insured, the coverage extends only to the degree permitted by law and within the limitations of the endorsement and the overall policy.

The endorsement applies to all locations and operations. Coverage is specific to the locations and operations listed in the schedule or the declarations. It does not universally apply to all locations where the primary policyholder operates.

It grants additional insureds same rights as the primary insured. The rights and coverages afforded to additional insureds under this endorsement are specific to the liabilities originating from the named insured’s actions. They do not include the full rights and protections granted to the primary policyholder.

This endorsement is solely for the benefit of the additional insureds. While it provides certain protections to additional insureds, it also benefits the primary policyholder by specifying limits and conditions under which others are covered, thereby helping to manage the policyholder’s risk exposure.

Understanding the intricacies of the CG 20 10 07 04 Liability Endorsement form is crucial for businesses and individuals engaging in contracts requiring additional insured status on a commercial general liability policy. Here are key takeaways that should be considered:

In essence, the CG 20 10 07 04 form represents an essential mechanism for extending liability coverage to additional insureds under a commercial general liability policy. It is paramount for parties involved to thoroughly understand and accurately complete this endorsement to ensure compliance and adequate coverage based on contractual obligations and legal requirements.