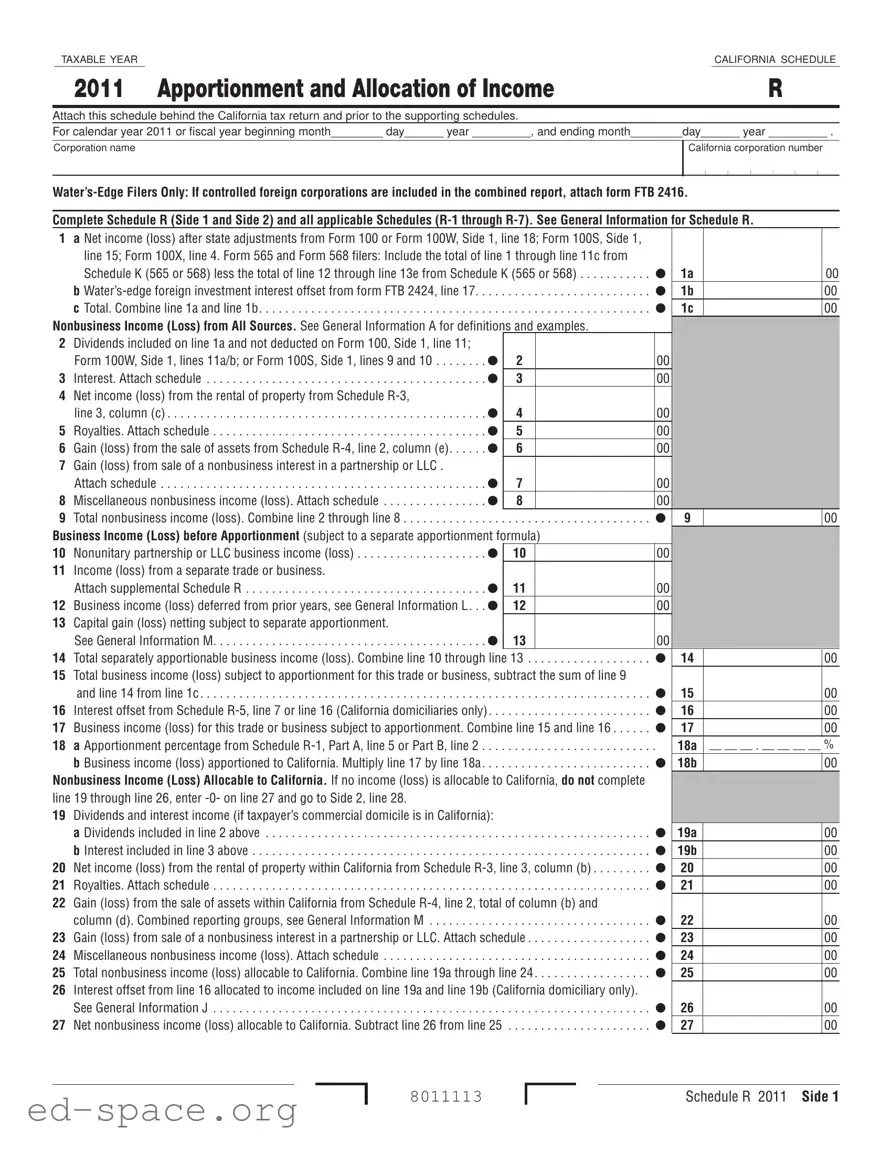

The California Schedule R form plays a crucial role in the state's tax reporting process for corporations, particularly in the apportionment and allocation of income. This form is essential for corporations operating both within and outside California, as it allows them to determine the portion of their income that is taxable in the state. The Schedule R is divided into two sides, with Side 1 focusing on the calculation of net income and losses, while Side 2 addresses the apportionment of business and nonbusiness income. Corporations must report their net income after state adjustments, including any nonbusiness income from dividends, interest, and rental properties. Additionally, the form requires the completion of various schedules (R-1 through R-7) to provide detailed information on income sources and apportionment factors. The form also includes provisions for corporations that elect to use the Water's-Edge method, which is particularly relevant for those with foreign investments. Accurate completion of the Schedule R is vital, as it directly impacts the corporation's tax liability and compliance with California tax regulations.

TAXABLE YEARCALIFORNIA SCHEDULE

2011 Apportionment and Allocation of IncomeR

Attach this schedule behind the California tax return and prior to the supporting schedules.

For calendar year 2011 or fiscal year beginning month________ day______ year _________, and ending month________day______ year _________ .

Corporation name

California corporation number

Complete Schedule R (Side 1 and Side 2) and all applicable Schedules

1 |

a Net income (loss) after state adjustments from Form 100 or Form 100W, Side 1, line 18; Form 100S, Side 1, |

|

|

|

|

|||

|

line 15; Form 100X, line 4. Form 565 and Form 568 filers: Include the total of line 1 through line 11c from |

|

|

|

|

|||

|

Schedule K (565 or 568) less the total of line 12 through line 13e from Schedule K (565 or 568) |

1a |

|

00 |

||||

|

|

|

|

|

|

|

|

|

|

b |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . |

1b |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

c Total. Combine line 1a and line 1b |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . |

1c |

|

00 |

|

Nonbusiness Income (Loss) from All Sources. See General Information A for definitions and examples. |

|

|

|

|

||||

2 |

Dividends included on line 1a and not deducted on Form 100, Side 1, line 11; |

|

|

|

|

|

|

|

|

Form 100W, Side 1, lines 11a/b; or Form 100S, Side 1, lines 9 and 10 |

2 |

|

00 |

|

|

|

|

3 |

Interest. Attach schedule |

|

3 |

|

00 |

|

|

|

4 |

Net income (loss) from the rental of property from Schedule |

|

|

|

|

|

|

|

|

line 3, column (c) |

4 |

|

00 |

|

|

|

|

5 |

Royalties. Attach schedule |

|

5 |

|

00 |

|

|

|

6 |

Gain (loss) from the sale of assets from Schedule |

|

6 |

|

00 |

|

|

|

7 |

Gain (loss) from sale of a nonbusiness interest in a partnership or LLC . |

|

|

|

|

|

|

|

|

Attach schedule |

7 |

|

00 |

|

|

|

|

8 |

Miscellaneous nonbusiness income (loss). Attach schedule |

|

8 |

|

00 |

|

|

|

9 |

. .Total nonbusiness income (loss). Combine line 2 through line 8 |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . |

|

9 |

|

00 |

Business Income (Loss) before Apportionment (subject to a separate apportionment formula) |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

10 |

Nonunitary partnership or LLC business income (loss) |

10 |

|

00 |

|

|

|

|

11 |

Income (loss) from a separate trade or business. |

|

|

|

|

|

|

|

|

Attach supplemental Schedule R |

11 |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

12 |

Business income (loss) deferred from prior years, see General Information L. . . |

12 |

|

00 |

|

|

|

|

13Capital gain (loss) netting subject to separate apportionment.

|

See General Information M |

13 |

00 |

|

|

|

|

14 |

Total separately apportionable business income (loss). Combine line 10 through line |

13 |

|

14 |

|

00 |

|

15 |

Total business income (loss) subject to apportionment for this trade or business, subtract the sum of line 9 |

|

|

|

|

||

|

and line 14 from line 1c |

. . . . . . . . . . . . . . . . . . . . . . . . . |

15 |

|

00 |

||

|

|

|

|

|

|

||

16 |

Interest offset from Schedule |

16 |

|

00 |

|||

|

|

|

|

|

|

||

17 |

Business income (loss) for this trade or business subject to apportionment. Combine line 15 and line 16 |

17 |

|

00 |

|||

18 |

a Apportionment percentage from Schedule |

. . . . . . . . . . . . . . . . . . . . . . . . . |

. |

18a |

__ __ __ . __ __ __ __ % |

||

|

b Business income (loss) apportioned to California. Multiply line 17 by line 18a . |

. . . . . . . . . . . . . . . . . . . . . . . . . |

18b |

|

00 |

||

Nonbusiness Income (Loss) Allocable to California. If no income (loss) is allocable to California, do not complete |

|

|

|

|

|||

line 19 through line 26, enter |

|

|

|

|

|

|

|

19 |

Dividends and interest income (if taxpayer’s commercial domicile is in California): |

|

|

|

|

||

|

a Dividends included in line 2 above |

. . . . . . . . . . . . . . . . . . . . . . . . . |

19a |

|

00 |

||

|

|

|

|

|

|

|

|

|

b Interest included in line 3 above |

. . . . . . . . . . . . . . . . . . . . . . . . . |

19b |

|

00 |

||

20 |

|

|

|

|

|

||

Net income (loss) from the rental of property within California from Schedule |

20 |

|

00 |

||||

|

|

|

|

|

|

|

|

21 |

Royalties. Attach schedule |

. . . . . . . . . . . . . . . . . . . . . . . . . |

21 |

|

00 |

||

22 |

Gain (loss) from the sale of assets within California from Schedule |

|

|

|

|

||

|

column (d). Combined reporting groups, see General Information M |

. . . . . . . . . . . . . . . . . . . . . . . . . |

22 |

|

00 |

||

23 |

|

|

|

|

|

||

Gain (loss) from sale of a nonbusiness interest in a partnership or LLC. Attach schedule |

23 |

|

00 |

||||

24 |

|

|

|

|

|

|

|

Miscellaneous nonbusiness income (loss). Attach schedule |

. . . . . . . . . . . . . . . . . . . . . . . . . |

24 |

|

00 |

|||

|

|

|

|

|

|

||

25 |

Total nonbusiness income (loss) allocable to California. Combine line 19a through line 24 |

25 |

|

00 |

|||

26 |

Interest offset from line 16 allocated to income included on line 19a and line 19b (California domiciliary only). |

|

|

|

|

||

|

See General Information J |

. . . . . . . . . . . . . . . . . . . . . . . . . |

26 |

|

00 |

||

27 |

|

|

|

|

|

||

Net nonbusiness income (loss) allocable to California. Subtract line 26 from line 25 |

27 |

|

00 |

||||

8011113

Schedule R 2011 Side 1

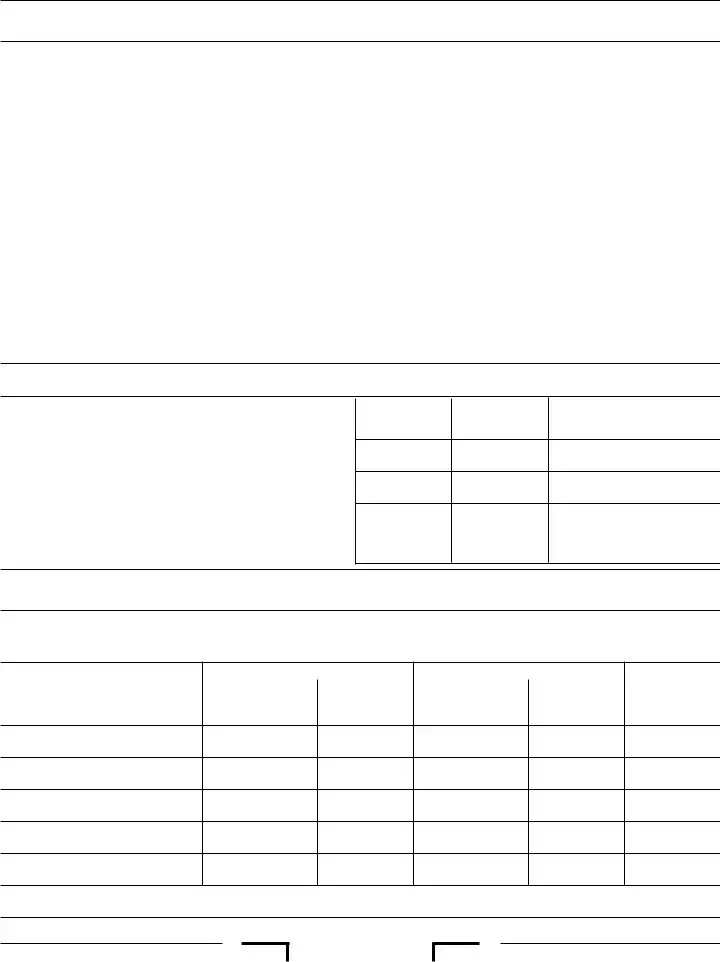

California Business Income (Loss) subject to a separate apportionment formula. |

|

|

|

|

28 |

California business income (loss) from a nonunitary partnership or LLC |

28 |

00 |

|

29 |

California income (loss) from a separate trade or business. Attach |

|

|

|

|

supplemental schedule R.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

29 |

00 |

|

30California business income (loss) deferred from prior years,

|

see General Information L |

30 |

00 |

|

31 |

Total business income (loss) separately apportioned to California. Combine line 28 through line 30 |

. |

31 |

|

Net Income (Loss) for California Purpose |

|

|

|

|

32 |

. |

|

||

|

See General Information M |

. . . . . . . . . . . . . . . . . . . . . . . . |

32 |

|

33 |

Net income (loss) for California purposes before contributions adjustment. Combine lines 18b, 27, 31, and 32 |

. |

33 |

|

34 |

Contributions adjustment from Schedule |

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

34 |

35 |

Net income (loss) for California purposes. Combine line 33 and line 34. Enter here and on Form 100 or |

. |

|

|

|

Form 100W, Side 1, line 19 or Form 100S, Side 1, line 16 |

. . . . . . . . . . . . . . . . . . . . . . . . |

35 |

|

00

00

00

00

00

Complete the applicable Schedules

Side 2 Schedule R 2011

8012113

Schedule

If “Yes,” skip Part A and complete Part B. If “No,” complete Part A and skip Part B.

Part A Standard Method –

|

(a) |

(b) |

|

|

|

|

|

|

|

|

|

|

|

|

|

(c) |

|

|

|||||||

|

Total within and outside California |

Total within California |

|

|

|

Percent within |

|

|

|||||||||||||||||

|

|

|

|

|

|

California (b) ÷ (a) |

|

|

|||||||||||||||||

1 Property: Use the average yearly value of owned real and tangible |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

personal property used in the business at original cost. See General |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Information E. Exclude property not connected with the business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and the value of construction in progress. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Inventory |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Buildings |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Machinery and equipment (including delivery equipment) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Furniture and fixtures |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Land |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other tangible assets. Attach schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rented property used in the business. See General Information E. . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total property |

|

|

|

|

. |

|

|

|

|

|

|

|

% |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 Payroll: Use employee wages, salaries, commissions, and other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

compensation related to business income. See General Information F. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total payroll |

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

% |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . . . . . . . . . . .3 Sales: Gross receipts, less returns, and allowances |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a Sales delivered or shipped to California purchasers. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See General Information G. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(i) Shipped from outside California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(ii) Shipped from within California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b Sales shipped from California to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(i) The United States Government |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(ii) Purchasers in a state where the taxpayer is not taxable. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See General Information G |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c Other gross receipts (rents, royalties, interest, etc.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total sales |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Divide total sales column (b) by total sales column (a) and multiply by 2 (except for qualified business activities). See General Information G |

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

% |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 Total percent. Add the percentages in column (c). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See General Information H |

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

% |

|||||

5 Apportionment percentage. Divide line 4 by 4 (qualified business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

activities divide by 3, see General Information G) and enter the result |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

here and on Schedule R, Side 1, line 18a. See General Information H |

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

% |

|||

Part B Alternate Method – |

|

|

|||||||||||||||||||||||

formula. This is an irrevocable annual election. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

(b) |

|

|

|

|

|

|

|

|

|

|

|

|

(c) |

|

|

||||||||

|

Total within and outside California |

Total within California |

|

|

Percent within |

|

|

||||||||||||||||||

|

|

|

|

|

|

California (b) ÷ (a) |

|

|

|||||||||||||||||

. . . . . . . . . . . . .1 Sales: Gross receipts, less returns, and allowances |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a Sales delivered or shipped to California purchasers. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See General Information G. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . .(i) Shipped from outside California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(ii) Shipped from within California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b Sales shipped from California to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . .(i) The United States Government |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(ii) Purchasers in a state where the taxpayer is not taxable. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . . . . .See General Information G |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

c Other gross receipts (rents, royalties, interest, etc.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total sales |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 Apportionment percentage. Divide total sales column (b) by total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

sales column (a) and enter the result here and on Schedule R, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Side 1, line 18a. See General Information H |

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

% |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8013113

Schedule R 2011 Side 3

Schedule

1Describe briefly the nature and location(s) of the California business activities: _____________________________________________________________

__________________________________________________________________________________________________________________________

2State the exact title and principal business activity of all joint ventures, partnerships, or LLCs in which the corporation has an interest: _________________

__________________________________________________________________________________________________________________________

3 Does the California sales figure on Schedule

4Does the California sales figure on Schedule

the taxpayer is not subject to tax? See General Information G. mYes mNo If “No,” explain. _____________________________________________

5Are the nonbusiness items reported on Schedule R, Side 1, line 2 through line 8, and the apportionment factor items reported on Schedule

6Has this corporation or any member of its combined unitary group changed the way income is apportioned or allocated to California from prior year tax

returns? See General Information I. mYes mNo If “Yes,” explain. ________________________________________________________________

__________________________________________________________________________________________________________________________

7Does the California sales figure on Schedule

mYes mNo If “No,” indicate the name of the selling member and the nature of the sales activity believed to be immune. ________________________

__________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________

8Does the California sales figure on Schedule

California which have an ultimate destination in California? mYes mNo If “No,” explain. _______________________________________________

Schedule

1 Income from rents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2 Rental deductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Net income (loss) from rents. Subtract line 2 from line 1. Enter the result here and enter column (c) on Side 1, line 4; enter column (b)

on Side 1, line 20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(a)

Total outside

California

(b)

Total within

California

(c)

Total outside and within

California (a) + (b)

Schedule

California sales of nonbusiness assets include transactions involving: (1) real property located in California; (2) tangible personal property, if it had a situs in California at the time of sale, or if the corporation is commercially domiciled in California and not taxable in the state where the property had a situs at the time of sale; and (3) intangible personal property if the corporation’s commercial domicile is in California or the income is otherwise allocable to California.

Description of property sold

Real estate and other tangible assets |

Intangible assets |

Total |

||

(a) |

(b) |

(c) |

(d) |

(e) |

Gain (loss) from outside |

Gain (loss) from |

Gain (loss) from |

Gain (loss) from |

Gain (loss) |

California |

within California |

outside California |

within California |

(a)+(b)+(c)+(d) |

1

2 Total gain (loss) . . . . . . . . . . . . . . . . . .

Enter total gain (loss) line 2, column (e) on Side 1, line 6 and enter total of line 2, columns (b) and (d) on Side 1, line 22

Side 4 Schedule R 2011

8014113

| Fact Name | Details |

|---|---|

| Purpose | The California Schedule R form is used for the apportionment and allocation of income for corporations operating in multiple states. |

| Tax Year | This specific form is for the tax year 2011, applicable to both calendar and fiscal year filers. |

| Filing Requirement | Taxpayers must attach Schedule R behind their California tax return before any supporting schedules. |

| Water's-Edge Filers | Corporations filing as water's-edge must include Form FTB 2416 if controlled foreign corporations are part of the combined report. |

| Nonbusiness Income | Schedule R includes sections for reporting nonbusiness income, such as dividends, interest, and gains from asset sales. |

| Governing Law | The California Schedule R is governed by the California Revenue and Taxation Code, particularly sections related to corporate taxation. |

Completing the California Schedule R form involves a systematic approach to ensure that all necessary information is accurately reported. This form is essential for corporations to report income and allocate it appropriately. Following the steps outlined below will help you fill out the form correctly, leading to a smoother filing process.

After completing these steps, review the form for accuracy. Once verified, you will be ready to submit the Schedule R along with your California tax return. Remember to keep a copy for your records.

What is the purpose of the California Schedule R form?

The California Schedule R form is used by corporations to report the apportionment and allocation of income for California tax purposes. It helps determine how much of a corporation's income is taxable in California, especially for those engaged in business both within and outside the state. This form is essential for ensuring compliance with California tax laws and accurately reporting income from various sources.

Who needs to file Schedule R?

What information is required on Schedule R?

Schedule R requires detailed information about the corporation's net income or loss, nonbusiness income, and business income before apportionment. Additionally, it asks for apportionment percentages and income allocable to California. The form also requires supporting schedules for specific types of income, such as rental income and gains from asset sales. Accurate reporting on this form is vital for determining the corporation's California tax liability.

What are the key sections of Schedule R?

Schedule R consists of several key sections, including the calculation of net income or loss, the reporting of nonbusiness and business income, and the apportionment of income to California. It also includes sections for specific types of income, such as dividends, interest, and gains from sales. Each section has specific lines that need to be filled out based on the corporation's financial activities during the tax year.

How do I determine the apportionment percentage?

The apportionment percentage is determined by using either the standard three-factor formula or the single-sales factor formula, depending on the corporation's election. The three-factor formula considers property, payroll, and sales, while the single-sales factor focuses solely on sales made to California customers. The appropriate formula must be completed on Schedule R-1, and the resulting percentage is then reported on Schedule R.

What if my corporation has nonbusiness income?

If your corporation has nonbusiness income, you must report it separately on Schedule R. This includes dividends, interest, and gains from the sale of nonbusiness assets. Nonbusiness income is treated differently from business income when determining apportionment and allocation to California. Ensure that you follow the guidelines for reporting nonbusiness income to avoid potential tax issues.

Can I attach additional schedules to Schedule R?

Yes, additional schedules can be attached to Schedule R as needed. For example, if your corporation has rental income, you would need to attach Schedule R-3. Similarly, if there are gains or losses from asset sales, Schedule R-4 must be included. Make sure to complete all applicable schedules to provide a comprehensive view of your corporation's income and comply with tax requirements.

What should I do if I need assistance with Schedule R?

If you need assistance with Schedule R, consider consulting a tax professional or accountant who specializes in California corporate tax law. They can help ensure that you complete the form accurately and comply with all necessary regulations. Additionally, the California Franchise Tax Board provides resources and guidance for completing tax forms, which can be helpful in navigating the filing process.

Incomplete Information: Failing to provide all required details, such as the corporation name or California corporation number, can lead to delays or rejections.

Incorrect Income Reporting: Misreporting net income or loss from Form 100 or Form 100W can result in incorrect tax calculations.

Neglecting Attachments: Not attaching necessary schedules, like R-1 through R-7, when applicable, may cause the form to be considered incomplete.

Miscalculating Apportionment: Errors in calculating the apportionment percentage can lead to incorrect tax obligations.

Omitting Nonbusiness Income: Failing to report all nonbusiness income, such as dividends or royalties, can result in underreporting income.

Ignoring California Specifics: Not considering California-specific rules, such as those related to water's-edge foreign investment, can lead to mistakes.

Inconsistent Reporting: Reporting different figures on various state tax returns can raise red flags and lead to audits.

Missing Deadlines: Submitting the form after the due date can incur penalties and interest.

Failing to Review: Not double-checking the form for accuracy before submission can result in avoidable errors.

Not Seeking Help: Avoiding professional assistance when unsure about complex sections can lead to mistakes that could have been easily avoided.

The California Schedule R form is an essential document for corporations operating within the state, particularly those involved in apportioning and allocating income. This form is typically accompanied by several other documents that provide critical information needed for accurate tax reporting. Below is a list of common forms and documents that are often used alongside the California Schedule R, each serving a specific purpose in the tax preparation process.

Utilizing these forms and schedules in conjunction with the California Schedule R ensures that corporations can accurately report their income and comply with state tax regulations. Each document plays a vital role in the overall tax filing process, contributing to a clearer understanding of the corporation's financial obligations in California.

When filling out the California Schedule R form, it’s important to keep a few key guidelines in mind. Here’s a list of things to do and avoid:

Understanding the California Schedule R form can be challenging. Here are some common misconceptions that may cause confusion:

Being aware of these misconceptions can help ensure that the Schedule R is completed accurately and efficiently. If you have any questions, seeking assistance can provide clarity and guidance.

When filling out and using the California Schedule R form, it is crucial to keep several key points in mind. These takeaways will help ensure accuracy and compliance with state tax regulations.

By following these key takeaways, you can navigate the complexities of the California Schedule R form more effectively. Timely and accurate completion of this form is vital to ensure compliance and avoid potential penalties.