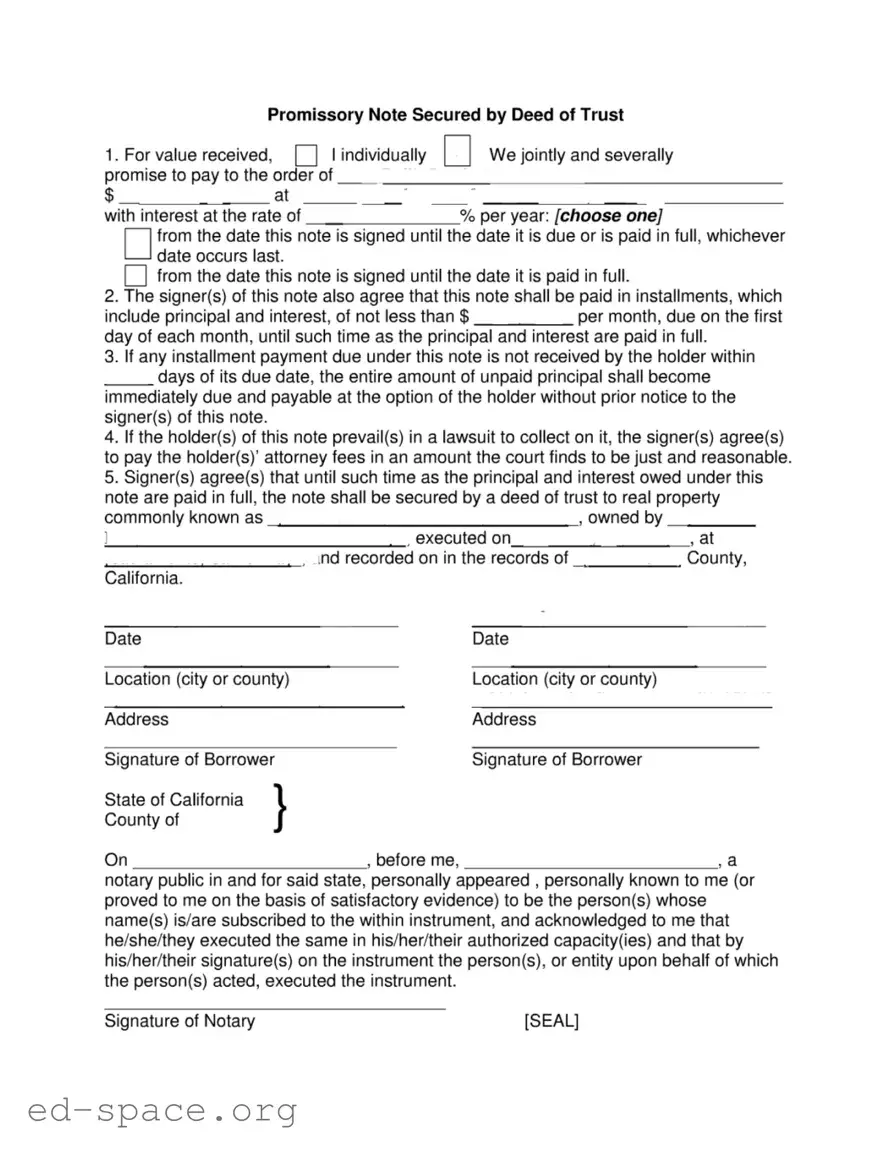

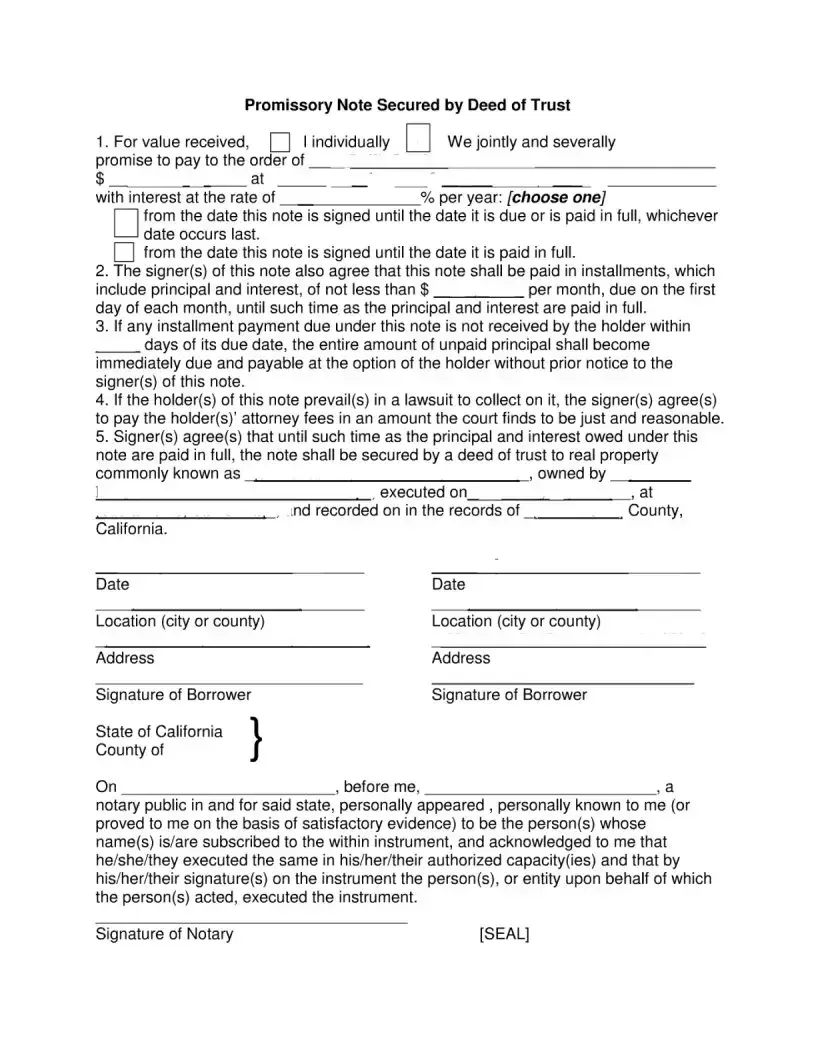

The California Note Secured form serves as a crucial document for individuals and entities entering into a loan agreement where a promissory note is backed by a deed of trust. This form outlines the borrower's commitment to repay a specified amount of money, along with interest, under agreed-upon terms. Borrowers must understand that payments are structured in installments, with specific monthly amounts due on the first day of each month until the loan is fully repaid. If a payment is missed, the lender has the right to demand the entire outstanding balance without prior notification. Additionally, should a legal dispute arise regarding the collection of the debt, the borrower is responsible for covering the lender's attorney fees, as determined by the court. The note is secured by a deed of trust on a designated property, providing the lender with a level of security in case of default. Proper execution of this form, including notarization, is essential to ensure its validity and enforceability in the state of California.

| Fact Name | Description |

|---|---|

| Purpose | The California Note Secured form is used to document a loan agreement secured by a deed of trust on real property. |

| Payment Terms | Borrowers must repay the loan in installments that include both principal and interest. |

| Interest Rate | The interest rate is specified in the note and can vary based on the agreement between the parties. |

| Late Payments | If a payment is not received within a certain number of days, the entire unpaid amount can become due immediately. |

| Attorney Fees | Should the lender need to pursue legal action, the borrower agrees to pay reasonable attorney fees incurred by the lender. |

| Security | The note is secured by a deed of trust on a specific property, which serves as collateral for the loan. |

| Governing Law | This form is governed by California law, specifically the California Civil Code. |

| Notarization | The signatures on the note must be notarized to verify the identity of the parties involved. |

| Record Keeping | Once executed, the deed of trust must be recorded in the county where the property is located to ensure legal enforceability. |

Filling out the California Note Secured form is a straightforward process, but it requires careful attention to detail. This form is essential for documenting a loan secured by real property. Once completed, it establishes the obligations of the borrower and the rights of the lender. Follow these steps to ensure that you fill out the form correctly.

What is a California Note Secured form?

The California Note Secured form is a legal document that outlines a borrower's promise to repay a loan. This form is secured by a deed of trust, which means that the loan is backed by real property. In essence, if the borrower fails to repay the loan as agreed, the lender has the right to take possession of the property to recover the owed amount. This document details the terms of repayment, including the amount borrowed, interest rates, and payment schedule.

How does the repayment process work?

Repayment under the California Note Secured form typically occurs in monthly installments. The borrower agrees to pay a specified amount each month, which includes both principal and interest. The payments are due on the first day of each month until the loan is fully repaid. This structure helps borrowers manage their finances by spreading the repayment over time, making it more manageable.

What happens if a payment is missed?

If a borrower fails to make a payment on time, the lender has the option to declare the entire unpaid principal amount due immediately. This means that the borrower could be required to pay back the full amount of the loan without any prior notice. It is crucial for borrowers to stay on top of their payments to avoid this situation, as it can lead to serious financial consequences.

Are there any legal fees involved if the lender takes action?

Yes, if the lender needs to take legal action to collect the debt, the borrower may be responsible for the lender's attorney fees. The borrower agrees to pay these fees if the lender prevails in a lawsuit. This provision emphasizes the importance of adhering to the terms of the note, as legal proceedings can be costly and stressful for all parties involved.

What does it mean for the note to be secured by a deed of trust?

A deed of trust is a legal instrument that secures the loan with real property. This means that the property serves as collateral for the loan. If the borrower defaults on the loan, the lender can initiate foreclosure proceedings to recover the owed amount by selling the property. This arrangement provides security for the lender and can help ensure that the borrower takes their repayment obligations seriously.

What is required for the form to be legally binding?

For the California Note Secured form to be legally binding, it must be signed by the borrower(s) and may require notarization. The notary public verifies the identities of the signers and ensures that they understand the document before signing. This step adds a layer of authenticity and protection, ensuring that all parties are entering into the agreement willingly and with full understanding of their obligations.

Incomplete Information: Many people forget to fill in all required fields. This includes the names of the parties involved, the amount of the loan, and the interest rate. Leaving any of these blank can lead to confusion and potential legal issues.

Incorrect Dates: It's common to see mistakes with dates. Ensure that the date the note is signed and any other relevant dates are accurate. An incorrect date can affect the validity of the note.

Not Specifying Payment Terms: Failing to clearly outline the payment terms is a frequent error. The amount of each installment, due dates, and whether the payments include both principal and interest should be explicitly stated.

Neglecting Notary Requirements: Some individuals overlook the need for notarization. If the form requires a notary, ensure that it is properly signed and stamped. This step is crucial for the document's legal enforceability.

The California Note Secured form is often accompanied by several other important documents that provide additional context and security for the transaction. Below is a list of these documents, each described briefly to clarify their purpose and relevance.

These documents work together to ensure that both the lender and borrower understand their rights and obligations, providing a framework for a secure and transparent transaction. Properly managing these forms is crucial for a successful lending process in California.

The California Note Secured form shares similarities with several other legal documents. Each of these documents serves a purpose related to loans, security interests, or agreements between parties. Here’s a breakdown of eight similar documents:

When filling out the California Note Secured form, it is essential to approach the task with care. Here are five things you should and shouldn't do:

There are several misconceptions surrounding the California Note Secured form. Understanding these can help clarify its purpose and function.