In the realm of real estate transactions, particularly during challenging financial times, the California Deed in Lieu of Foreclosure form serves as a crucial tool for homeowners facing foreclosure. This legal document allows a property owner to voluntarily transfer ownership of their home back to the lender, effectively sidestepping the lengthy and often stressful foreclosure process. By doing so, homeowners can mitigate the damage to their credit scores and potentially avoid the public stigma associated with foreclosure. The form outlines essential details, including the property description, the parties involved, and the terms of the transfer. Importantly, it often includes a clause that releases the homeowner from any further liability for the mortgage debt, providing a sense of closure and relief. Additionally, the process typically requires the lender's acceptance of the deed, ensuring that both parties agree to the terms laid out in the document. Understanding the nuances of this form can empower homeowners to make informed decisions during difficult financial times, paving the way for a fresh start while protecting their financial future.

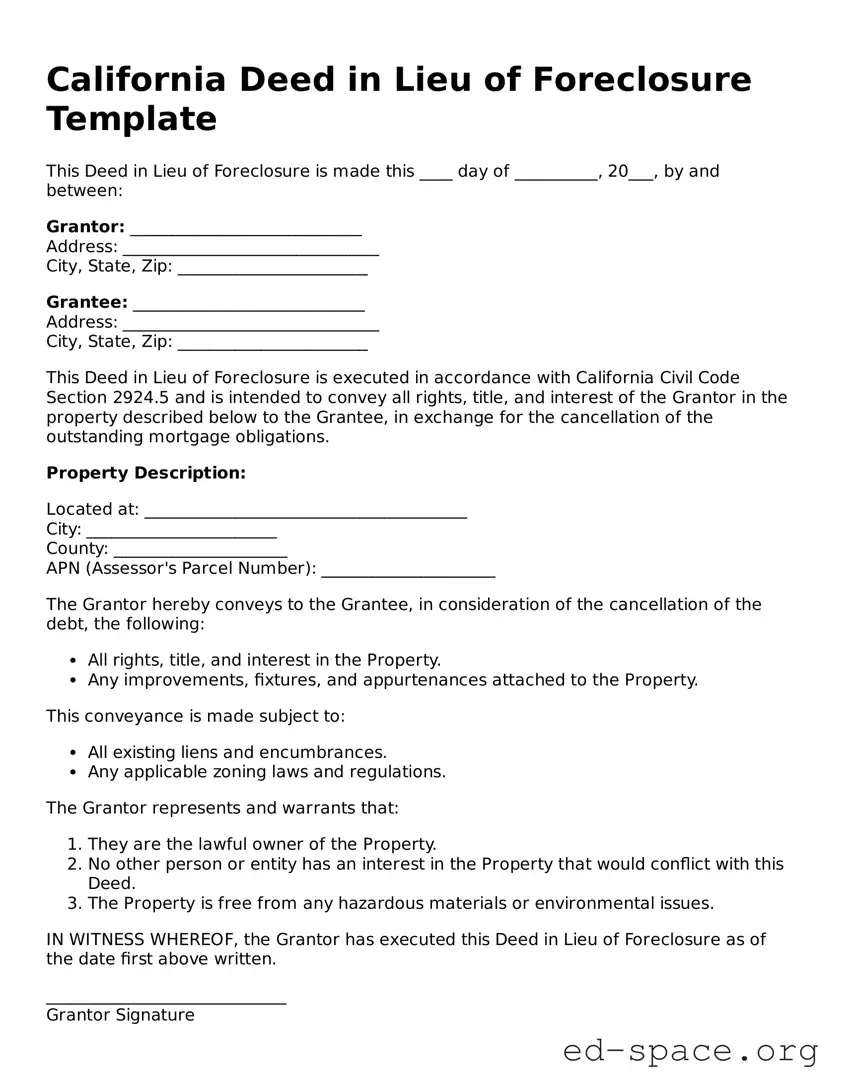

California Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is made this ____ day of __________, 20___, by and between:

Grantor: ____________________________

Address: _______________________________

City, State, Zip: _______________________

Grantee: ____________________________

Address: _______________________________

City, State, Zip: _______________________

This Deed in Lieu of Foreclosure is executed in accordance with California Civil Code Section 2924.5 and is intended to convey all rights, title, and interest of the Grantor in the property described below to the Grantee, in exchange for the cancellation of the outstanding mortgage obligations.

Property Description:

Located at: _______________________________________

City: _______________________

County: _____________________

APN (Assessor's Parcel Number): _____________________

The Grantor hereby conveys to the Grantee, in consideration of the cancellation of the debt, the following:

This conveyance is made subject to:

The Grantor represents and warrants that:

IN WITNESS WHEREOF, the Grantor has executed this Deed in Lieu of Foreclosure as of the date first above written.

_____________________________

Grantor Signature

_____________________________

Grantee Signature

_____________________________

Witness Signature

_____________________________

Witness Signature

State of California

County of ____________________

On this ____ day of __________, 20___, before me, a Notary Public in and for said State, personally appeared _______________________, known to me to be the person whose name is subscribed to the within instrument, and acknowledged that they executed the same.

WITNESS my hand and official seal.

_____________________________

Notary Public

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal agreement where a borrower voluntarily transfers property ownership to the lender to avoid foreclosure. |

| Governing Law | The California Deed in Lieu of Foreclosure is governed by California Civil Code Sections 580 and 726. |

| Eligibility | Borrowers must be in default on their mortgage payments to qualify for a deed in lieu of foreclosure. |

| Process | The borrower must submit a formal request to the lender, along with relevant documentation, to initiate the process. |

| Benefits | This option can help borrowers avoid the lengthy and stressful foreclosure process. |

| Impact on Credit | A deed in lieu of foreclosure may negatively impact the borrower's credit score, but typically less severely than a foreclosure. |

| Deficiency Judgments | In California, lenders generally cannot pursue deficiency judgments after a deed in lieu of foreclosure. |

| Tax Implications | Borrowers should consult a tax professional, as there may be tax implications associated with the cancellation of debt. |

| Timeframe | The entire process can vary in duration but typically takes several weeks to complete once initiated. |

| Alternatives | Borrowers may consider alternatives such as loan modification or short sale before opting for a deed in lieu of foreclosure. |

After completing the California Deed in Lieu of Foreclosure form, the next step involves submitting the document to the appropriate parties. This typically includes the lender and any relevant local government offices. Ensure that you keep copies of all documents for your records. Once submitted, the lender will review the form, and further actions will follow based on their response.

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal process where a homeowner voluntarily transfers ownership of their property to the lender to avoid foreclosure. This option can help borrowers escape the lengthy and costly foreclosure process while settling their mortgage debt more amicably.

Who is eligible for a Deed in Lieu of Foreclosure?

Typically, homeowners facing financial hardship and unable to keep up with mortgage payments may be eligible. Lenders often require that the borrower has tried other options, such as loan modifications or short sales, before considering a Deed in Lieu. Each lender may have specific eligibility criteria.

What are the benefits of choosing a Deed in Lieu of Foreclosure?

One significant benefit is that it can be less damaging to your credit score than a foreclosure. Additionally, it allows for a quicker resolution to the mortgage issue, and borrowers may be able to negotiate a release from any remaining debt. It can also provide peace of mind by avoiding the stress of foreclosure proceedings.

Are there any drawbacks to a Deed in Lieu of Foreclosure?

Yes, there are drawbacks. While it may be less harmful to your credit than foreclosure, it can still impact your credit score. Furthermore, you may not be able to negotiate favorable terms, and some lenders may pursue a deficiency judgment for any unpaid balance on the mortgage. Always consider these factors carefully.

How does the process work?

The process begins with contacting your lender to express your interest in a Deed in Lieu of Foreclosure. You will need to provide financial documentation to prove your hardship. If the lender agrees, you will sign a deed transferring ownership. The lender may then forgive the remaining debt, but this should be confirmed in writing.

Can I stay in my home after signing a Deed in Lieu of Foreclosure?

Generally, once the deed is signed, you will need to vacate the property. However, some lenders may offer a leaseback option that allows you to remain in the home for a certain period. It’s essential to discuss this possibility with your lender before proceeding.

What happens to my credit score?

A Deed in Lieu of Foreclosure can negatively impact your credit score, but usually less severely than a foreclosure. The exact effect will depend on your overall credit history. It’s advisable to monitor your credit report after the process is complete to understand its impact.

Should I consult a lawyer before proceeding with a Deed in Lieu of Foreclosure?

Yes, consulting a lawyer is highly recommended. They can provide guidance specific to your situation, help you understand your rights, and ensure that you are making an informed decision. Legal advice can be crucial in navigating the complexities of this process.

Not understanding the implications of a deed in lieu of foreclosure. Many homeowners mistakenly believe it is a straightforward process without fully grasping the long-term effects on their credit and future homeownership.

Failing to consult with a real estate attorney or financial advisor. Skipping this step can lead to critical oversights in the process.

Incorrectly filling out personal information. Missing or inaccurate names, addresses, or other identifying details can delay the process or cause complications.

Not including all necessary documentation. Essential paperwork, such as the mortgage statement or proof of ownership, may be overlooked.

Neglecting to provide a valid reason for the deed in lieu. A clear explanation can help the lender process the request more efficiently.

Ignoring the need for lender approval. Some homeowners mistakenly believe they can simply submit the deed without obtaining consent from their lender.

Overlooking tax implications. Many individuals do not consider how a deed in lieu may affect their tax situation, potentially leading to unexpected liabilities.

Failing to keep copies of all submitted documents. This can create issues if there are disputes or if proof of submission is needed later.

Not understanding the timeline for the process. Many individuals underestimate how long it may take for the lender to respond and finalize the deed.

A Deed in Lieu of Foreclosure is a useful tool for homeowners facing financial difficulties. It allows them to transfer their property back to the lender, avoiding the lengthy and often painful foreclosure process. Several other forms and documents typically accompany this deed to ensure a smooth transaction. Below are some of the most common documents associated with a Deed in Lieu of Foreclosure in California.

Each of these documents plays a vital role in facilitating the Deed in Lieu of Foreclosure process. Understanding them can help homeowners navigate their options and make informed decisions during a challenging time.

The Deed in Lieu of Foreclosure is a significant legal document that allows a homeowner to transfer their property to the lender to avoid foreclosure. Several other documents share similarities with this form, each serving distinct purposes in real estate transactions. Here are six documents that are comparable to the Deed in Lieu of Foreclosure:

Understanding these documents can empower homeowners to make informed decisions during challenging financial situations. Each serves a unique purpose, yet they all share the common goal of providing alternatives to foreclosure.

When filling out the California Deed in Lieu of Foreclosure form, it is important to approach the process carefully. Here are some guidelines to consider:

When it comes to the California Deed in Lieu of Foreclosure, there are several misconceptions that can lead to confusion for homeowners facing financial difficulties. Understanding the truth behind these myths can help you make informed decisions. Here are five common misconceptions:

Understanding these misconceptions can empower homeowners to navigate their options more effectively. Always consider consulting with a legal or financial professional to explore the best path forward for your specific situation.

Filling out and using the California Deed in Lieu of Foreclosure form can be a crucial step for homeowners facing financial difficulties. Here are some key takeaways to consider: