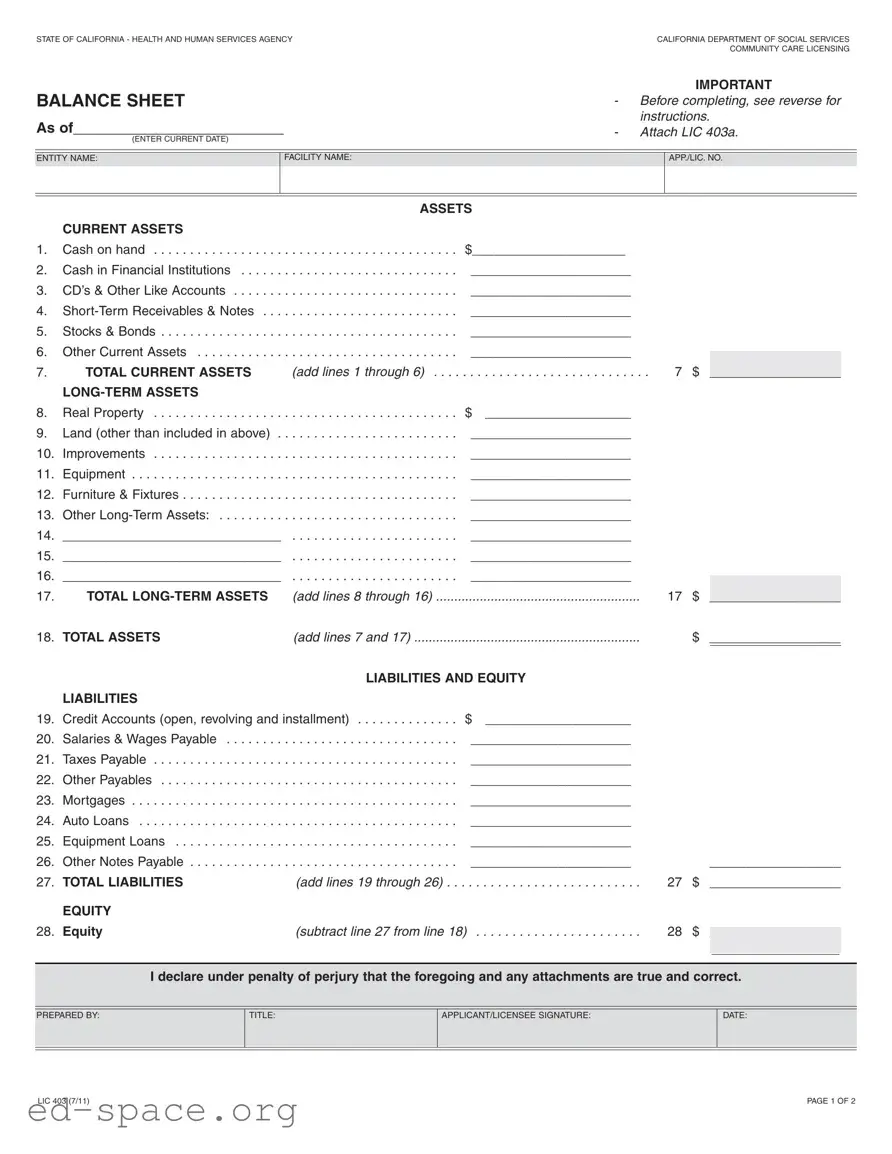

The California Balance Sheet form, known as LIC 403, is an essential document for entities involved in community care licensing. It provides a clear snapshot of an organization's financial position, detailing both assets and liabilities. This form helps in assessing the financial health of care facilities, ensuring they meet the necessary requirements for operation. The balance sheet is divided into two main sections: assets and liabilities. Within assets, current and long-term categories allow for a comprehensive view of cash, property, equipment, and other resources. On the liabilities side, it includes credit accounts, payables, and loans, giving insight into financial obligations. Additionally, the form requires the calculation of equity, which represents the difference between total assets and total liabilities. Completing the LIC 403 involves transferring totals from a supplemental schedule, LIC 403a, and accurately reporting all relevant financial information. This ensures transparency and accountability for both the facility and regulatory bodies.

STATE OF CALIFORNIA - HEALTH AND HUMAN SERVICES AGENCY |

CALIFORNIA DEPARTMENT OF SOCIAL SERVICES |

|

COMMUNITY CARE LICENSING |

|

|

|

|

IMPORTANT |

|

BALANCE SHEET |

- |

Before completing, see reverse for |

|||

As of__________________________ |

|

instructions. |

|||

- |

Attach LIC 403a. |

||||

(ENTER CURRENT DATE) |

|||||

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

ENTITY NAME: |

|

FACILITY NAME: |

|

APP./LIC. NO. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ASSETS |

|

|

|

|

|

|

|

CURRENT ASSETS |

|

|

|

|

|

|

|

1. |

Cash on hand |

. . . . . . . . . . . . . . . . . . . . . . . |

$_____________________ |

|

|

|

|

|

2. |

Cash in Financial Institutions |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

3. |

CD’s & Other Like Accounts |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

4. |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

||

5. |

Stocks & Bonds |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

6. |

Other Current Assets |

|

______________________ |

|

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . |

|

|

|

|

||||

7. |

TOTAL CURRENT ASSETS |

(add lines 1 through 6) . . . . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . 7 |

$ |

|

__________________ |

|

|

|

|

|

|

|

|

|

|

8. |

Real Property |

. . . . . . . . . . . . . . . . . . . . . . . |

$ |

____________________ |

|

|

|

|

9. |

Land (other than included in above) . . |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

10. |

Improvements |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

11. |

Equipment |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

12. |

Furniture & Fixtures |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

13. |

Other |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

14. |

______________________________ |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

15. |

______________________________ |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

16. |

______________________________ |

|

______________________ |

|

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . |

|

|

|

|

||||

17. |

TOTAL |

(add lines 8 through 16) |

17 |

$ |

|

__________________ |

|

|

18. |

TOTAL ASSETS |

(add lines 7 and 17) |

|

$ |

__________________ |

|

||

|

|

LIABILITIES AND EQUITY |

|

|

|

|

||

|

LIABILITIES |

|

|

|

|

|

|

|

19. |

Credit Accounts (open, revolving and installment) |

$ |

____________________ |

|

|

|

|

|

20. |

Salaries & Wages Payable |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

21. |

Taxes Payable |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

22. |

Other Payables |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

23. |

Mortgages |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

24. |

Auto Loans |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

25. |

Equipment Loans |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

|

|

|

|

26. |

Other Notes Payable |

. . . . . . . . . . . . . . . . . . . . . . . |

______________________ |

|

__________________ |

|

||

27. |

TOTAL LIABILITIES |

(add lines 19 through 26) |

. . . . . . . . . . . . . . . . . . . . . . 27 |

$ |

__________________ |

|

||

|

EQUITY |

|

|

|

|

|

|

|

28. |

Equity |

(subtract line 27 from line 18) |

28 |

$ |

|

|

|

|

__________________ |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I declare under penalty of perjury that the foregoing and any attachments are true and correct.

PREPARED BY:

TITLE:

APPLICANT/LICENSEE SIGNATURE:

DATE:

LIC 403 (7/11) |

PAGE 1 OF 2 |

BALANCE SHEET

GENERAL INFORMATION: To complete the Balance Sheet LIC 403, first complete the LIC 403a, Balance Sheet Supplemental Schedule. The LIC 403a is a worksheet to be used in compiling the detailed information which is then totaled and displayed on the Balance Sheet, LIC 403. Submit the LIC 403a attached to the LIC 403.

Each applicant/licensee (sole proprietorship, partnership or corporation) must submit a LIC 403, and a LIC 403a. Information to be reported is to disclose all the entity’s assets and liabilities, not just those related to the operation of the care facility.

FOR SOLE PROPRIETORSHIPS - For a facility operated by a husband or wife individually, information reported must pertain to both, such as individual credit card balances which are listed either solely under one name or under both the husband and wife, and which may be unrelated to the facility’s actual operation or the person who will actually operate the facility.

FOR GENERAL PARTNERS - In addition to financial statements for the partnership, each general partner must file a personal Balance Sheet, LIC 403, accompanied with a LIC 403a, to reflect their individual financial position.

Information shown on the LIC 403 and LIC 403a is subject to verification. Additional documentation may be requested to support any or all of the Balance Sheet amounts reported.

INSTRUCTIONS: Include the required information at the top of this form to identify: 1) current date for the Balance Sheet, 2) entity name, (this is the sole proprietorship, partner, partnership or corporate name for whom the information is being reported) 3) facility name and 4) application/license number. Transfer the totals from the worksheet LIC 403a to the corresponding lines on the LIC 403. Below is a brief description of the type of information to be contained on each line.

ASSETS

Line #

1.Cash on hand, not deposited in a financial institution.

2.Cash in checking accounts.

3.CD’s, savings account(s) and all other like accounts.

4.Revenues receivable and all

5.Stocks, bonds or other securities.

6.Other current assets readily converted to cash, such as the cash surrender value of whole life insurance policies.

7.Add the amounts on lines 1 through 6 and enter here.

8.Real property is buildings, land and structures.

9.Land (developed or undeveloped) not already included on line 8.

10.Improvements to real property or leasehold improvements as appropriate.

11.Business or personal equipment, (other than that being leased).

12.Business or personal furniture and fixtures, as appropriate, (other than that being leased).

17.Add the amounts reported on lines 8 through 16 and enter here.

18.Add the amounts on line 7 and line 17 and enter here.

LIABILITIES

19.Credit Accounts (Open, Revolving and Installment).

20.Salaries, wages, bonuses and other benefits payable.

21.Federal, state or local income, sales or payroll taxes.

22.Other notes or payables not included above.

23.Current balances for all of the outstanding mortgages.

24.Vehicle loans.

25.Loans payable for furniture and equipment.

26.Other

27.Add the amounts on lines 19 through 26 and enter here.

EQUITY

28.The equity is the difference between your total assets and total liabilities. Subtract line 27 from line 18 and enter here.

SIGNATURE BLOCK

The name of the preparer is to be printed in the space provided. The applicant or licensee is required to sign this form attesting to the financial information. Failure to sign, date and attest to the accuracy of the information reported on the Balance Sheet (LIC 403) shall constitute

LIC 403 (7/11) |

PAGE 2 OF 2 |

| Fact Name | Details |

|---|---|

| Governing Law | The California Balance Sheet form is governed by the California Health and Safety Code. |

| Purpose | This form is used to report the financial position of a care facility. |

| Entities Required | Sole proprietorships, partnerships, and corporations must complete this form. |

| Supplemental Schedule | Attach LIC 403a, the Balance Sheet Supplemental Schedule, to the main form. |

| Asset Categories | Assets are divided into current and long-term categories, including cash and real property. |

| Liabilities Section | Includes credit accounts, salaries payable, and other financial obligations. |

| Equity Calculation | Equity is calculated by subtracting total liabilities from total assets. |

| Signature Requirement | The form must be signed by the applicant or licensee to attest to its accuracy. |

| Non-Compliance Consequence | Failure to sign may lead to rejection of the Balance Sheet submission. |

Completing the California Balance Sheet form requires careful attention to detail. The information provided will reflect the financial position of the entity, including both assets and liabilities. Ensure all figures are accurate and that the necessary supporting documents are attached.

What is the purpose of the California Balance Sheet form?

The California Balance Sheet form, also known as LIC 403, serves as a financial snapshot of a care facility's assets, liabilities, and equity. It is essential for applicants and licensees in the health and human services sector to provide a clear picture of their financial standing. This form helps regulatory bodies assess the financial viability of the facility, ensuring that it can operate effectively and meet its obligations to clients and employees.

Who is required to complete the California Balance Sheet form?

All applicants and licensees, whether operating as sole proprietorships, partnerships, or corporations, must complete the California Balance Sheet form. This includes individual operators, general partners, and corporate entities. Each entity must provide a comprehensive view of its financial position, which includes not only the facility's assets and liabilities but also those that may be personally held by the operators or partners.

What information is needed to complete the form?

To complete the form accurately, you will need to gather detailed financial information regarding both current and long-term assets, as well as liabilities. This includes cash on hand, bank account balances, real estate holdings, loans, and any other relevant financial data. Additionally, you will need to attach the LIC 403a, which serves as a supplemental schedule to help compile and organize this information before transferring the totals to the LIC 403 form.

What are the key components of the Balance Sheet?

The California Balance Sheet is divided into three main sections: assets, liabilities, and equity. The assets section includes both current assets, such as cash and receivables, and long-term assets, like real property and equipment. The liabilities section lists all debts and obligations, including loans and payables. Finally, equity is calculated by subtracting total liabilities from total assets, providing insight into the net worth of the entity.

What happens if the form is not signed or dated?

Failure to sign and date the California Balance Sheet form constitutes non-compliance. This oversight may lead to the rejection of the report, which could hinder the licensing process or affect the facility's operational status. It is crucial for the applicant or licensee to attest to the accuracy of the reported information by providing their signature, ensuring that all data is truthful and complete.

Can the information on the Balance Sheet be verified?

Yes, the information provided on the California Balance Sheet is subject to verification. Regulatory authorities may request additional documentation to support any amounts reported. It is important to maintain accurate records and be prepared to provide evidence of the financial figures included in the Balance Sheet. This verification process helps ensure the integrity of the financial information presented and supports the overall accountability of the facility.

Omitting Required Information: Many individuals fail to include the necessary identifying information at the top of the form, such as the current date, entity name, facility name, and application/license number. This can lead to processing delays.

Incorrectly Calculating Totals: A common mistake is miscalculating the totals for current assets and long-term assets. It is essential to double-check the addition of lines 1 through 6 for current assets and lines 8 through 16 for long-term assets.

Failure to Attach Supplemental Schedule: The LIC 403a, which provides detailed information, must be attached to the Balance Sheet. Neglecting to do so can result in incomplete submissions.

Inaccurate Reporting of Liabilities: Individuals often misreport their liabilities. It is crucial to include all relevant debts, such as credit accounts, loans, and other payables, to present an accurate financial position.

Not Signing or Dating the Form: The applicant or licensee must sign and date the form. Failing to do so can lead to non-compliance and rejection of the report.

Ignoring Verification Requirements: Some individuals do not prepare for potential verification of the reported amounts. Supporting documentation may be requested, and having this ready can expedite the review process.

The California Balance Sheet form is an essential document used by applicants and licensees in the health and human services sector. Along with this form, there are several other documents that help provide a complete financial picture of the entity. Below is a list of related forms that are often used in conjunction with the California Balance Sheet.

Each of these documents plays a vital role in the application and licensing process for community care facilities in California. Together, they help ensure that facilities meet state standards and provide safe, quality care to their clients.

The California Balance Sheet form has similarities with several other financial documents. Here are seven such documents and how they relate to the Balance Sheet:

When filling out the California Balance Sheet form, it is essential to follow certain guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do:

Understanding the California Balance Sheet form is crucial for accurate financial reporting. However, several misconceptions can lead to confusion. Here are five common misconceptions:

By addressing these misconceptions, individuals can ensure they complete the California Balance Sheet form accurately and in compliance with regulations.

When filling out the California Balance Sheet form, there are several important points to keep in mind. Here are key takeaways to ensure accuracy and compliance: