The California Form 592-B plays a crucial role in the state's tax system, particularly for individuals and entities involved in withholding taxes. This form is utilized by withholding agents, such as corporations, partnerships, and trusts, to report amounts withheld from payments made to both resident and nonresident recipients. It provides detailed information about the income subject to withholding, including payments to independent contractors, estate distributions, and rents or royalties. The form also outlines the total tax withheld, which is essential for ensuring compliance with California tax laws. Notably, the form has specific sections that require the withholding agent to provide their identification details, the recipient's information, and the type of income involved. Additionally, it highlights important changes in tax rates and backup withholding requirements, making it essential for withholding agents to stay informed about current regulations. Completing the Form 592-B accurately and submitting it on time is vital, as failure to do so can result in penalties. Understanding the nuances of this form is essential for anyone involved in financial transactions that fall under California's tax jurisdiction.

TAXABLE YEAR |

Resident and Nonresident Withholding |

|

|

CALIFORNIA FORM |

|

|

|

|

|

|

|

|

||

2012 Tax Statement |

||||

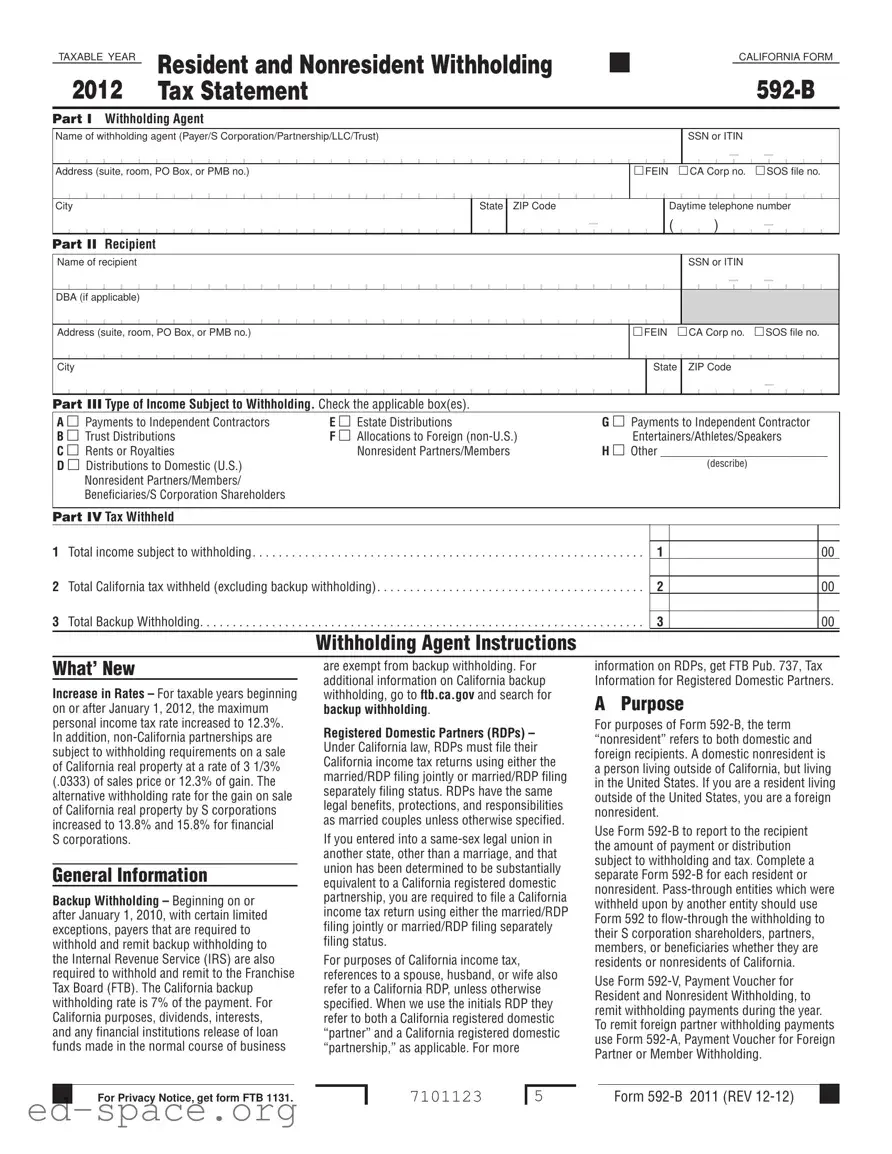

Part I Withholding Agent

Name of withholding agent (Payer/S Corporation/Partnership/LLC/Trust)

SSN or ITIN

Address (suite, room, PO Box, or PMB no.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEIN |

|

CA Corp no. SOS file no. |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State |

ZIP Code |

|

Daytime telephone number |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

|

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part II Recipient

Name of recipient

DBA (if applicable)

SSN or ITIN

Address (suite, room, PO Box, or PMB no.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEIN |

CA Corp no. SOS file no. |

||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

ZIP Code |

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part III Type of Income Subject to Withholding. Check the applicable box(es). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

A Payments to Independent Contractors |

|

E Estate Distributions |

|

G Payments to Independent Contractor |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

B Trust Distributions |

|

F Allocations to Foreign |

|

|

|

|

Entertainers/Athletes/Speakers |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

C Rents or Royalties |

|

|

|

|

|

Nonresident Partners/Members |

|

H Other ___________________________ |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

D Distributions to Domestic (U.S.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(describe) |

||||||||||||||||||||||||||||||||||||||||||||

|

|

Nonresident Partners/Members/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

Beneficiaries/S Corporation Shareholders |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

Part IV Tax Withheld |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

1 Total income subject to withholding. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2 Total California tax withheld (excluding backup withholding). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Total Backup Withholding. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2

3

00

00

00

Withholding Agent Instructions

What’ New

Increase in Rates – For taxable years beginning on or after January 1, 2012, the maximum personal income tax rate increased to 12.3%. In addition,

S corporations.

General Information

Backup Withholding – Beginning on or after January 1, 2010, with certain limited exceptions, payers that are required to withhold and remit backup withholding to the Internal Revenue Service (IRS) are also required to withhold and remit to the Franchise Tax Board (FTB). The California backup withholding rate is 7% of the payment. For California purposes, dividends, interests,

and any financial institutions release of loan funds made in the normal course of business

are exempt from backup withholding. For additional information on California backup withholding, go to ftb.ca.gov and search for backup withholding.

Registered Domestic Partners (RDPs) – Under California law, RDPs must file their California income tax returns using either the married/RDP filing jointly or married/RDP filing separately filing status. RDPs have the same legal benefits, protections, and responsibilities as married couples unless otherwise specified.

If you entered into a

For purposes of California income tax, references to a spouse, husband, or wife also refer to a California RDP, unless otherwise specified. When we use the initials RDP they refer to both a California registered domestic “partner” and a California registered domestic “partnership,” as applicable. For more

information on RDPs, get FTB Pub. 737, Tax Information for Registered Domestic Partners.

A Purpose

For purposes of Form

Use Form

Use Form

For Privacy Notice, get form FTB 1131.

7101123

5 |

Form |

THIS PAGE INTENTIONALLY LEFT BLANK

visit our website:

ftb.ca.gov

Page 2 Form

B Common Errors/Helpful Hints

•Get taxpayer identification numbers (TINs) from all payees.

•Complete all fields.

•Complete all forms timely to avoid penalties.

C Who Must Complete

Form

•Has withheld on payments to residents or nonresidents.

•Has withheld backup withholding on payments to residents or nonresidents.

•Is a

Record Keeping

The withholding agent retains the proof of withholding for a minimum of four years and must provide it to the FTB upon request. Form

D When To Complete

Form

•Each resident or nonresident by January 31 following the close of the calendar year, except for brokers as stated in Internal Revenue Code (IRC) Section 6045.

•A recipient before February 15 following the close of the calendar year for brokers.

•Foreign partners in a partnership or members in a limited liability company (LLC) on

or before the 15th day of the 4th month following the close of the taxable year.

If all the partners in the partnership or members in the LLC are foreign, Form(s)

When making a payment of withholding tax to the IRS under IRC Section 1446, a partnership must notify all foreign partners of their allocable shares of any IRC Section 1446 tax paid to the IRS by the partnership. The partners use this information to adjust the amount of estimated tax that they must otherwise pay to the IRS. The notification to the foreign partners must be provided within 10 days of the installment due date, or, if paid later, the date the installment payment is made. See Treas. Regs. Section

the notification and for exceptions to the notification requirement. For California withholding purposes, withholding agents should make a similar notification. No particular form is required for this notification, and it is commonly done on the statement

accompanying the distribution or payment. However, the withholding agent may choose to report the tax withheld to the payee on a Form

E Penalties

The withholding agent must furnish complete and correct copies of Form(s)

If the withholding agent fails to provide complete, correct, and timely Form(s)

•$50 for each payee statement not provided by the due date.

•$100 or 10 percent of the amount required to be reported (whichever is greater), if the failure is due to intentional disregard of the requirement.

Specific Instructions

Year – Make sure the year in the upper left corner of Form

For foreign partners in a partnership, or foreign members in an LLC, make sure the year in the upper left corner of Form

Private Mail Box (PMB) – Include the PMB in the address field. Write “PMB” first, then the box number. Example: 111 Main Street PMB 123.

Foreign Address – Enter the information in the following order: City, Country, Province/ Region, and Postal Code. Follow the country’s practice for entering the postal code. Do not abbreviate the country’s name.

Part I – Withholding Agent

Enter the withholding agent’s name, tax identification number, address, and telephone number.

Part II – Recipient

Enter the name of recipient, DBA (if applicable), tax identification number, and address for the recipient (payee).

If the recipient is a grantor trust, enter the grantor’s individual name and social security number (SSN) or individual taxpayer identification number (ITIN). Do not enter the name of the trust or trustee information. (For

tax purposes, grantor trusts are transparent. The individual grantor must report the income and claim the withholding on the individual’s California tax return.)

If the recipient is a

enter trustee information.

If the trust has applied for a FEIN, but it has not been received, zero fill the space for the trust’s FEIN and attach a copy of the federal application behind Form

Only withholding agents can complete an amended Form

If the recipients are married/RDP, enter only the name and SSN or ITIN of the primary spouse/RDP. However, if the recipients intend to file separate California tax returns, the withholding agent should split the withholding and complete a separate Form

Part III – Type of Income Subject to Withholding

Check the box(es) for the type of income subject to withholding.

Part IV – Tax Withheld

Line 1

Enter the total income subject to withholding.

Line 2

Enter the total California tax withheld (excluding backup withholding). The amount of tax to be withheld is computed by applying a rate of 7% on items of income subject to withholding, i.e. interest, dividends, rents and royalties, prizes and winnings, premiums, annuities, emoluments, compensation

for personal services, and other fixed or determinable annual or periodical gains, profits and income. For foreign partners, the rate is 8.84% for corporations, 10.84% for banks and financial institutions, and 12.3% for all others. For pass through entities, the amount withheld is allocated to partners, members,

S corporation shareholders, or beneficiaries, whether they are residents or nonresidents of California, in proportion to their ownership or beneficial interest.

Line 3

Enter the total backup withholding. Compute backup withholding by applying a 7% rate to all reportable payments subject to IRS backup withholding with a few exceptions. For California purposes dividends, interests, and any financial institutions release of loan funds made in the normal course of business are exempt from backup withholding.

Form

Instructions for Recipient

This withholding of tax does not relieve you of the requirement to file a California tax return within three months and fifteen days (two months and fifteen days for a corporation) after the close of your taxable year.

You may be assessed a penalty if:

•You do not file a California tax return.

•You file your tax return late.

•The amount of withholding does not satisfy your tax liability.

How to Claim the Withholding

Report the income as required and enter the amount from Form

If you have an amount in line 3, backup withholding, you must provide us with your TIN before filing your tax return. Using the information provided on this page, contact us as soon as you receive this form. Failure to provide your TIN will result in a denial of your backup withholding credit.

If you are an S corporation, partnership, or LLC, you may either

If the withholding exceeds the amount of tax you still owe on your tax return, you must

If you do not have an outstanding balance on your tax return, you must

If you are an estate or trust, you must flow- through the withholding to your beneficiaries if the related income was distributed. Use Form 592 to

The amount shown as “Total income subject to withholding” may be an estimate or may only reflect how withholding was calculated. Be sure to report your actual taxable California source income. If you are an independent contractor or receive rents or royalties, see your contract and/or Form 1099 to determine your California source income. If you are an S corporation shareholder, partner, member, or beneficiary of an S corporation, partnership, LLC, estate, or trust, see your California Schedule

Additional Information

For more information or to speak to a representative regarding this form, call the Withholding Services and Compliance’s automated telephone service at: 888.792.4900 or 916.845.4900.

OR write to:

WITHHOLDING SERVICES AND COMPLIANCE FRANCHISE TAX BOARD

PO BOX 942867 SACRAMENTO CA

For all other questions unrelated to withholding or to access the TTY/TDD number, see the information below.

Internet and Telephone Assistance Website: ftb.ca.gov

Telephone: 800.852.5711 from within the United States 916.845.6500 from outside the United States

TTY/TDD: 800.822.6268 for persons with hearing or speech impairments

OR to get forms by mail, write to:

TAX FORMS REQUEST UNIT FRANCHISE TAX BOARD PO BOX 307

RANCHO CORDOVA CA

Asistencia Por Internet y Teléfono

Sitio web: |

ftb.ca.gov |

Teléfono: |

800.852.5711 dentro de los |

|

Estados Unidos |

|

916.845.6500 fuera de los Estados |

|

Unidos |

TTY/TDD: |

800.822.6268 personas con |

|

discapacidades auditivas y del |

|

habla |

Page 4 Form

| Fact Name | Description |

|---|---|

| Purpose | The California Form 592-B is used to report amounts withheld from payments made to both resident and nonresident recipients. It ensures that the correct tax is withheld and reported to the state. |

| Who Must File | Any person or entity that withholds taxes on payments to residents or nonresidents, including partnerships and S corporations, must complete this form. |

| Filing Deadline | The form must be provided to recipients by January 31 of the year following the close of the calendar year, with some exceptions for brokers and foreign partners. |

| Backup Withholding Rate | The current backup withholding rate in California is 7% on reportable payments, unless exempted, such as dividends and interest under certain conditions. |

| Governing Law | The use and requirements for Form 592-B are governed by California Revenue and Taxation Code Sections 18662 and 18666, which outline withholding obligations for various entities. |

Completing the California 592-B form is a straightforward process that requires attention to detail. This form is essential for reporting payments subject to withholding and ensuring compliance with state tax regulations. Below are the steps to fill out the form accurately.

After completing the form, it is important to provide it to the recipient by the required deadline, which is typically January 31 of the following year. This ensures that the recipient can accurately report their income on their tax return. Keep in mind that failure to provide the form on time may result in penalties.

What is the purpose of California Form 592-B?

The California Form 592-B is used to report payments or distributions that are subject to withholding tax for both residents and nonresidents. This form provides recipients with a statement of the amount withheld, which they will need when filing their California tax returns. It is essential for ensuring compliance with California tax laws, especially for payments made to independent contractors, trusts, and foreign entertainers or athletes.

Who is required to complete Form 592-B?

Any person or entity that has withheld taxes on payments to residents or nonresidents must complete Form 592-B. This includes withholding agents such as S corporations, partnerships, LLCs, and trusts. Additionally, if backup withholding has been applied, Form 592-B must also be completed. It is important to provide accurate information to avoid penalties.

When is Form 592-B due?

Form 592-B must be provided to each recipient by January 31 of the year following the close of the calendar year. For brokers, the deadline is February 15. If dealing with foreign partners in a partnership or members of an LLC, the form must be provided by the 15th day of the fourth month following the close of the taxable year. Timely submission is crucial to avoid penalties.

What types of income are subject to withholding reported on Form 592-B?

Various types of income are subject to withholding and should be reported on Form 592-B. This includes payments to independent contractors, rents, royalties, estate distributions, and allocations to foreign entertainers or athletes. Each applicable type of income must be checked on the form to ensure proper reporting.

What happens if Form 592-B is not completed correctly or on time?

Failure to provide complete and accurate Form 592-B can result in penalties. The withholding agent may incur a $50 penalty for each statement not provided by the due date. If the failure is due to intentional disregard of the requirements, the penalty can increase to $100 or 10% of the amount required to be reported, whichever is greater. It is essential to ensure accuracy and timeliness to avoid these penalties.

How does a recipient claim the withholding reported on Form 592-B?

Recipients must report the income as required and include the amount from Form 592-B when filing their California tax return. Specifically, the amount shown in Part IV, line 2 should be entered as real estate and other withholding. It is also necessary to attach a copy of Form 592-B to the tax return. If backup withholding is indicated, recipients must provide their Tax Identification Number (TIN) to ensure they receive the appropriate credit.

Where can I find more information about Form 592-B?

For additional information regarding Form 592-B, individuals can visit the Franchise Tax Board’s website at ftb.ca.gov. They can also contact the Withholding Services and Compliance at 888.792.4900 for automated assistance or 916.845.4900 for direct inquiries. It is advisable to keep informed about any updates or changes to the form and its requirements.

Missing Taxpayer Identification Numbers: Ensure that you obtain and include taxpayer identification numbers (TINs) for all payees. Failing to do so can lead to complications and delays.

Incomplete Fields: Every field on the form should be filled out completely. Leaving any section blank may result in penalties or the form being rejected.

Timeliness: Submit the form on time to avoid penalties. The deadline for providing Form 592-B to recipients is January 31 of the following year.

Incorrect Tax Year: Verify that the year in the upper left corner matches the calendar year in which the withholding occurred. An incorrect year can lead to misreporting.

Improper Address Formatting: When entering addresses, especially for foreign recipients, follow the required format closely. This includes specifying “PMB” before the box number if applicable.

Failure to Check Income Types: Make sure to check all applicable boxes for the type of income subject to withholding. Omitting this step can result in inaccurate reporting.

Incorrect Tax Calculation: Ensure that the tax withheld is calculated correctly based on the applicable rates. Double-check the amounts entered on lines 1, 2, and 3 for accuracy.

Not Amending When Necessary: If an error is discovered after submission, promptly amend the form. Only the withholding agent can complete this process.

Ignoring Backup Withholding Requirements: Be aware of backup withholding obligations and ensure that you report any applicable amounts. Failure to do so can lead to penalties.

The California 592 B form is an essential document used for reporting withholding on payments made to both residents and nonresidents. When dealing with this form, it’s helpful to be aware of other related documents that often accompany it. Each of these forms serves a unique purpose in the tax reporting process, ensuring compliance with California's tax laws.

Understanding these forms can simplify the tax filing process and ensure compliance with California tax regulations. Each document plays a role in accurately reporting income and withholding, which is crucial for both individuals and entities involved in financial transactions within the state.

The California 592-B form is important for reporting withholding on payments to residents and nonresidents. Several other forms serve similar purposes in different contexts. Here’s a list of documents that share similarities with the California 592-B form:

When filling out the California 592 B form, there are several important dos and don'ts to keep in mind to ensure accuracy and compliance. Below is a list of these guidelines:

Understanding the California 592 B form is crucial for compliance. However, several misconceptions can lead to confusion. Here are eight common misconceptions and clarifications regarding the form:

This is incorrect. Both residents and non-residents who receive payments subject to withholding must be reported using this form.

While it includes payments to independent contractors, it also applies to various types of income, including estate distributions and payments to foreign entertainers.

This is false. The withholding agent must furnish a complete and correct copy of Form 592 B to the recipient by the due date.

In fact, California has its own backup withholding requirements, which can apply to certain payments.

This is misleading. The form must be provided to recipients by January 31 of the following year, with specific deadlines for brokers and foreign partners.

This is not true. Different types of income may have different withholding rates, especially for foreign partners and specific entities.

Errors must be corrected promptly. Failure to provide accurate information can lead to penalties for the withholding agent.

This is incorrect. Recipients are still required to file their California tax returns, regardless of the withholding.

Addressing these misconceptions is essential for ensuring compliance with California tax laws. If there are any uncertainties, it is advisable to seek assistance promptly.

Filling out and using the California 592-B form is essential for reporting income subject to withholding. Here are four key takeaways to consider: