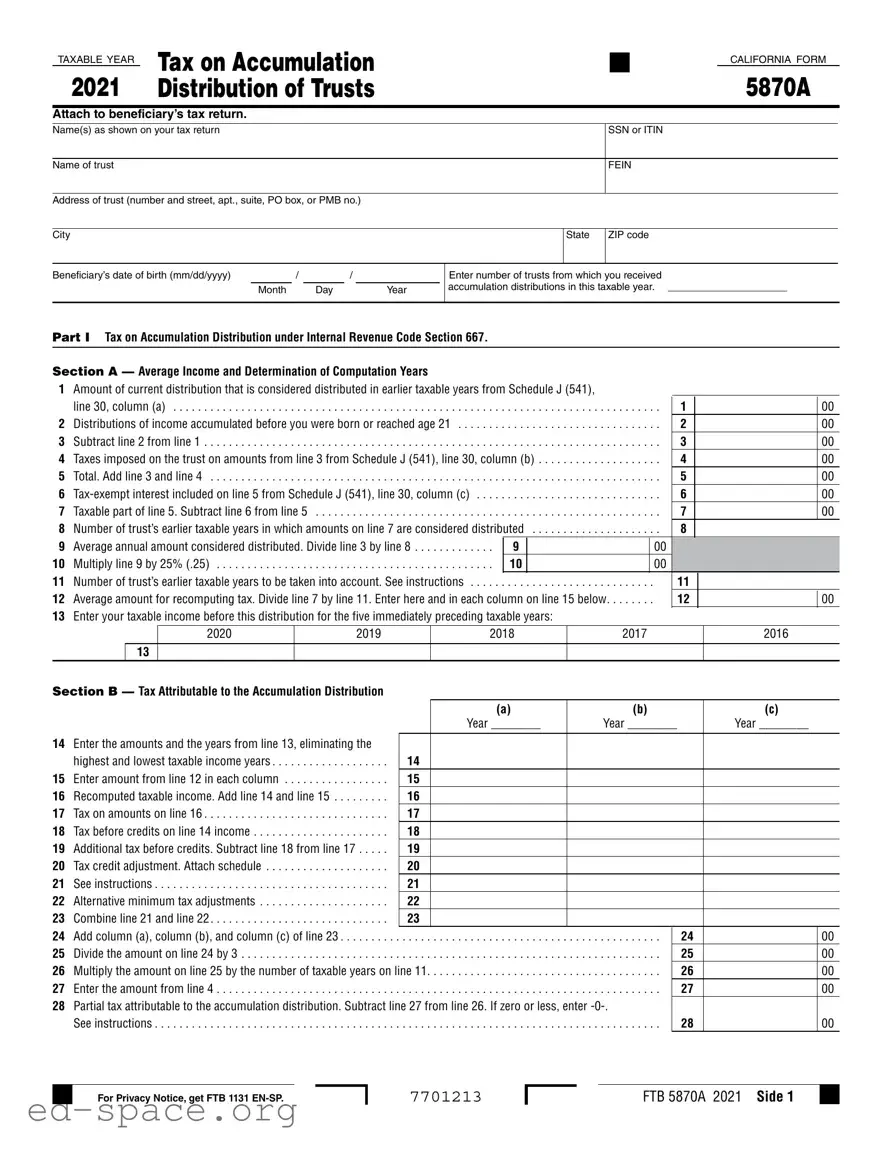

The California 5870A form serves as an essential document for beneficiaries receiving distributions from trusts, particularly those that involve accumulated income. This form is specifically designed to calculate taxes on accumulation distributions under Internal Revenue Code Section 667, as well as address previously untaxed trust income under California Revenue and Taxation Code Section 17745. Beneficiaries must provide their personal information, including Social Security Number or Individual Taxpayer Identification Number, along with details about the trust, such as its name and address. The form includes multiple sections that guide users through various calculations, including the average income and tax attributable to accumulation distributions, as well as mental health services tax considerations. By accurately completing the 5870A, beneficiaries can ensure compliance with tax regulations and determine the appropriate tax liabilities associated with their trust distributions. Understanding the intricacies of this form is crucial for effective tax planning and reporting.

TAXABLE YEAR |

TAX ON ACCUMULATION |

|

|

|

|

|

|

|

CALIFORNIA FORM |

|||||

2021 |

|

|

|

|

|

|

|

5870A |

||||||

DISTRIBUTION OF TRUSTS |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attach to beneficiary’s tax return. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Name(s) as shown on your tax return |

|

|

|

|

|

|

|

|

|

SSN or ITIN |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

Name of trust |

|

|

|

|

|

|

|

|

|

|

FEIN |

|||

|

|

|

|

|

|

|

|

|

||||||

Address of trust (number and street, apt., suite, PO box, or PMB no.) |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||

City |

|

|

|

|

|

|

|

|

|

State |

ZIP code |

|||

|

|

|

|

|

|

|

|

|

|

|

||||

Beneficiary’s date of birth (mm/dd/yyyy) |

|

/ |

|

/ |

|

|

|

Enter number of trusts from which you received |

||||||

|

|

Month |

Day |

Year |

accumulation distributions in this taxable year. _____________________ |

|||||||||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART I Tax on Accumulation Distribution under Internal Revenue Code Section 667.

SECTION A — Average Income and Determination of Computation Years

1Amount of current distribution that is considered distributed in earlier taxable years from Schedule J (541),

|

line 30, column (a) |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. . |

1 |

|

00 |

|

2 |

Distributions of income accumulated before you were born or reached age 21 |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. . |

2 |

|

|

00 |

3 |

Subtract line 2 from line 1 |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. . |

3 |

|

|

00 |

4 |

Taxes imposed on the trust on amounts from line 3 from Schedule J (541), line 30, column (b) |

. . |

4 |

|

|

00 |

||

5 |

Total. Add line 3 and line 4 |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. . |

5 |

|

|

00 |

6 |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. . |

6 |

|

|

00 |

|

7 |

Taxable part of line 5. Subtract line 6 from line 5 |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. . |

7 |

|

|

00 |

8 |

. . . . . . . . . . . . . . . . . . .Number of trust’s earlier taxable years in which amounts on line 7 are considered distributed |

. . |

8 |

|

|

|

||

9 |

Average annual amount considered distributed. Divide line 3 by line 8 |

9 |

|

00 |

|

|

|

|

10 |

Multiply line 9 by 25% (.25) |

10 |

|

00 |

|

|

|

|

11 |

Number of trust’s earlier taxable years to be taken into account. See instructions |

. . . . |

. . . . . . . . . . . . . . . . . . . |

. |

11 |

|

|

|

12 |

. . . . . . .Average amount for recomputing tax. Divide line 7 by line 11. Enter here and in each column on line 15 below |

. |

12 |

|

|

00 |

||

13Enter your taxable income before this distribution for the five immediately preceding taxable years:

2020 |

2019 |

2018 |

2017 |

2016 |

13

SECTION B — Tax Attributable to the Accumulation Distribution

(a) |

(b) |

(c) |

Year ________ |

Year ________ |

Year ________ |

14Enter the amounts and the years from line 13, eliminating the

|

highest and lowest taxable income years |

14 |

|

|

15 |

Enter amount from line 12 in each column |

15 |

|

|

16 |

Recomputed taxable income. Add line 14 and line 15 |

16 |

|

|

17 |

Tax on amounts on line 16 |

17 |

|

|

18 |

Tax before credits on line 14 income |

18 |

|

|

19 |

Additional tax before credits. Subtract line 18 from line 17 |

19 |

|

|

20 |

Tax credit adjustment. Attach schedule |

20 |

|

|

21 |

See instructions |

21 |

|

|

22 |

Alternative minimum tax adjustments |

22 |

|

|

23 |

Combine line 21 and line 22 |

23 |

|

|

24 |

Add column (a), column (b), and column (c) of line 23 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

24 |

00 |

25 |

Divide the amount on line 24 by 3 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

25 |

00 |

26 |

Multiply the amount on line 25 by the number of taxable years on line 11 |

26 |

00 |

|

27 |

Enter the amount from line 4 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

27 |

00 |

28Partial tax attributable to the accumulation distribution. Subtract line 27 from line 26. If zero or less, enter

See instructions |

28 |

00 |

For Privacy Notice, get FTB 1131

7701213

FTB 5870A 2021 Side 1

PART II Tax on Distributions of Previously Untaxed Trust Income under Revenue and Taxation Code Section 17745 (b) and (d):

#If the income was accumulated over a period of five taxable years or more, complete Section A.

#If the income was accumulated over a period of less than five taxable years, complete Section B.

SECTION A — See instructions. |

|

|

1 Income accumulated over five taxable years or more |

1 |

00 |

2Divide line 1 by six. Enter here and on Schedules CA (540), Part I, Section B, line 8z, column C,

|

or CA (540NR), Part II, Section B, line 8z, column C |

2 |

|

00 |

|||||

|

|

|

(a) |

(b) |

(c) |

|

(d) |

(e) |

|

|

|

|

2020 |

2019 |

2018 |

2017 |

2016 |

|

|

3 |

Were you a resident or |

3 |

• Yes |

• Yes |

• Yes |

• Yes |

• Yes |

||

|

(Answer “No” for nonresident years.) |

|

• No |

• No |

• No |

• No |

• No |

||

4 |

Enter your taxable income before this distribution for the five immediately |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

preceding years. See instructions |

4 |

|

|

|

|

|

|

|

5 |

Enter the amount from line 2 in col. (a) through col. (e) if the distribution |

|

|

|

|

|

|

|

|

|

is ordinary income. For a capital gain distribution, see instructions |

5 |

|

|

|

|

|

|

|

6 |

Recomputed taxable income. Add line 4 and line 5 |

6 |

|

|

|

|

|

|

|

7 |

Tax on amounts on line 6 |

7 |

|

|

|

|

|

|

|

8 |

Tax before credits on line 4 income |

8 |

|

|

|

|

|

|

|

9 |

Additional tax before credits. Subtract line 8 from line 7 |

9 |

|

|

|

|

|

|

|

10 |

Tax credit adjustment. Attach schedule |

10 |

|

|

|

|

|

|

|

11 |

Subtract line 10 from line 9. See instructions |

11 |

|

|

|

|

|

|

|

12 |

Alternative minimum tax adjustments |

12 |

|

|

|

|

|

|

|

13 |

Add line 11 and line 12 |

13 |

|

|

|

|

|

|

|

14 |

Add line 13, column (a) through column (e) for all taxable years that you checked “Yes” on line 3. Enter here and on |

|

|

|

|

||||

|

Form 540, line 34; Form 540NR, line 41; or Form 541, line 21b. See instructions. . |

. . . . . . . . . . . . |

. . . . . . . . . . . |

. . . . . . . . . . . |

14 |

|

|

00 |

|

SECTION B — See instructions. |

|

|

|

1 |

Income accumulated less than five taxable years |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . 1 |

2 |

Averaging factor: |

|

|

|

a Enter the number of years the trust accumulated the amount on line 1 |

2a |

|

|

b Distribution year |

2b |

1 |

3 |

Add line 2a and line 2b |

. . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . 3 |

4Divide line 1 by line 3. Enter here and on Schedule CA (540), Part I, Section B, line 8z, column C,

or Schedule CA (540NR), Part II, Section B, line 8z, column C |

4 |

00

00

|

|

|

(a) |

(b) |

(c) |

(d) |

|||

|

|

|

2020 |

2019 |

2018 |

|

2017 |

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Were you a resident or |

5 |

• Yes |

• Yes |

• Yes |

• Yes |

|||

|

(Answer “No” for nonresident years.) |

|

• No |

• No |

• No |

• No |

|||

6 |

Enter your taxable income before this distribution for the number of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

preceding years entered on line 2a. See instructions |

6 |

|

|

|

|

|

|

|

7 |

Enter the amount from line 4 in col. (a) through col. (d). See instructions . . |

7 |

|

|

|

|

|

|

|

8 |

Recomputed taxable income. Add line 6 and line 7 |

8 |

|

|

|

|

|

|

|

9 |

Tax on amounts on line 8 |

9 |

|

|

|

|

|

|

|

10 |

Tax before credits on line 6 income |

10 |

|

|

|

|

|

|

|

11 |

Additional tax before credits. Subtract line 10 from line 9 |

11 |

|

|

|

|

|

|

|

12 |

Tax credit adjustment. Attach schedule |

12 |

|

|

|

|

|

|

|

13 |

Subtract line 12 from line 11. See instructions |

13 |

|

|

|

|

|

|

|

14 |

Alternative minimum tax adjustments |

14 |

|

|

|

|

|

|

|

15 |

Add line 13 and line 14 |

15 |

|

|

|

|

|

|

|

16 |

Add line 15, column (a) through column (d) for all taxable years that you checked “Yes” on line 5. Enter here and on |

|

|

|

|

|

|||

|

Form 540, line 34; Form 540NR, line 41; or Form 541, line 21b. See instructions. . |

. . . . . . . . . . . . . |

. . . . . . . . . . . . . . . |

. . . . . |

16 |

|

|

00 |

|

Side 2 FTB 5870A 2021

7702213

PART III Mental Health Services Tax under Revenue and Taxation Code Section 17043:

#If the income was accumulated over a period of five taxable years or more, complete Section A.

#If the income was accumulated over a period of less than five taxable years, complete Section B.

SECTION A — See instructions. |

|

|

|

|

|

|

|

List the tax year where you selected “Yes” to Part II, Section A, line 3. |

|

(a) |

(b) |

(c) |

(d) |

(e) |

|

|

|

|

Year _____ |

Year _____ |

Year _____ |

Year _____ |

Year _____ |

|

|

|

|

|

|

|

|

1 |

Enter the recomputed taxable income from Part II, Section A, line 6 |

1 |

|

|

|

|

|

2 |

Subtract 1,000,000 from line 1. If zero or less, enter |

2 |

|

|

|

|

|

3 |

Multiply line 2 by 1% |

3 |

|

|

|

|

|

4 |

Mental Health Services Tax paid on taxable income before distribution . . . |

4 |

|

|

|

|

|

5 |

Subtract line 4 from line 3 |

5 |

|

|

|

|

|

6Add line 5, columns (a) through (e). Enter here and on Form 540, line 62; Form 540NR, line 72; or

|

Form 541, line 27. See instructions |

. . . . |

. . . . . . . . . . . |

. . . . . . . . . . . |

6 |

00 |

SECTION B — See instructions. |

|

|

|

|

|

|

List the tax year where you selected “Yes” to Part II, Section B, line 5. |

|

(a) |

(b) |

(c) |

(d) |

|

|

|

|

Year _____ |

Year _____ |

Year _____ |

Year _____ |

|

|

|

|

|

|

|

1 |

Enter the recomputed taxable income from Part II, Section B, line 8 |

1 |

|

|

|

|

2 |

Subtract 1,000,000 from line 1. If zero or less enter |

2 |

|

|

|

|

3 |

Multiply line 2 by 1% |

3 |

|

|

|

|

4 |

Mental Health Services Tax paid on taxable income before distribution |

4 |

|

|

|

|

5 |

Subtract line 4 from line 3 |

5 |

|

|

|

|

6Add line 5, columns (a) through (d). Enter here and on Form 540, line 62; Form 540NR, line 72; or

Form 541, line 27. See instructions |

6 |

00 |

7703213

FTB 5870A 2021 Side 3

| Fact Name | Details |

|---|---|

| Purpose | The California 5870A form is used to report the tax on accumulation distributions from trusts. |

| Governing Law | This form is governed by the Internal Revenue Code Section 667 and California Revenue and Taxation Code Section 17745. |

| Filing Requirement | Beneficiaries must attach this form to their tax return when they receive accumulation distributions from a trust. |

| Taxable Year | The form is specific to the taxable year, with the 2020 version being applicable for that year. |

| Information Required | Key details needed include the beneficiary's name, Social Security Number, trust name, and income information from previous years. |

Filling out the California 5870A form requires careful attention to detail. This form is used for reporting the tax on accumulation distributions from trusts. To ensure accuracy and compliance, follow these steps closely.

Next, move on to Part I, where you will compute the tax on accumulation distributions. Follow the instructions carefully, filling in each line with the appropriate information from your records and any attached schedules. After completing Part I, proceed to Parts II and III as applicable, depending on the nature of the distributions. Double-check your calculations to ensure everything is accurate before submitting the form with the beneficiary's tax return.

What is the California 5870A form used for?

The California 5870A form is used to report the tax on accumulation distributions from trusts. If you received distributions from a trust that has accumulated income, this form helps you calculate the tax owed on those distributions. It is typically attached to the beneficiary's tax return.

Who needs to file the 5870A form?

If you are a beneficiary of a trust that has made accumulation distributions, you will need to file the 5870A form. This applies if you received income that was accumulated in the trust before you were born or before you turned 21 years old.

What information is required on the 5870A form?

You will need to provide details such as your name, Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), the name of the trust, its address, and your date of birth. Additionally, you will need to report the number of trusts from which you received accumulation distributions during the taxable year.

How do I determine the tax on accumulation distributions?

The form contains sections where you will calculate the tax based on the accumulated income. You will need to complete calculations that involve your previous taxable income, the amounts distributed from the trust, and any applicable tax credits. Following the instructions carefully will help ensure accurate calculations.

What should I do if I received distributions from multiple trusts?

If you received accumulation distributions from more than one trust, you will need to report the details for each trust separately on the form. Ensure you accurately list the number of trusts and provide the required information for each to avoid confusion and potential errors in your tax filing.

Are there any specific deadlines for filing the 5870A form?

The 5870A form must be filed by the tax return due date for the year in which you received the distributions. This is typically April 15th, but it may vary if you file for an extension. Always check the current tax year deadlines to ensure timely submission.

What happens if I don’t file the 5870A form?

Failing to file the 5870A form when required can lead to penalties and interest on any unpaid taxes. It is important to comply with tax regulations to avoid complications with the California Franchise Tax Board. If you are unsure about your obligations, consulting a tax professional can be beneficial.

Can I amend my tax return if I realize I need to file the 5870A form?

Yes, if you discover that you should have filed the 5870A form after you have already submitted your tax return, you can amend your return. Use Form 540X to make the necessary corrections and include the 5870A form with your amended return.

Where can I find additional help or resources for filling out the 5870A form?

The California Franchise Tax Board (FTB) provides resources and instructions for filling out the 5870A form. Their website offers guidance, FAQs, and contact information for assistance. Additionally, tax professionals can offer personalized help if you have specific questions or concerns.

Is there a privacy notice associated with the 5870A form?

Yes, there is a privacy notice associated with the 5870A form. It is important to review this notice to understand how your personal information will be used and protected. You can find the privacy notice on the California FTB website or by referring to Form FTB 1131.

Incorrect Personal Information: Many individuals fail to provide accurate personal details, such as the beneficiary's Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). This mistake can lead to processing delays or complications with the IRS.

Omitting Trust Details: Some people neglect to include the trust's Employer Identification Number (FEIN) or its address. This omission can hinder the identification of the trust and affect the distribution process.

Errors in Tax Calculations: It is common for filers to miscalculate the amounts in various sections, particularly in the tax computation parts. For instance, failing to accurately subtract tax-exempt interest from taxable income can result in incorrect tax obligations.

Missing Required Attachments: Many individuals forget to attach necessary schedules or documentation required by the form. This can lead to incomplete submissions, which may trigger audits or additional inquiries from tax authorities.

The California 5870A form is essential for reporting taxes on accumulation distributions from trusts. When filling out this form, you may also need several other documents to ensure accurate reporting and compliance with tax regulations. Here’s a list of forms commonly used alongside the California 5870A.

Using these forms in conjunction with the California 5870A can help ensure that all tax obligations are met and that beneficiaries accurately report their income. Always consult a tax professional if you have questions about your specific situation.

The California 5870A form is used for reporting tax on accumulation distributions from trusts. It shares similarities with several other tax-related documents. Below is a list of nine forms that are comparable to the California 5870A, along with a brief explanation of how they are similar.

When filling out the California 5870A form, there are several important dos and don'ts to keep in mind. Here’s a helpful list to guide you.

Here are ten common misconceptions about the California 5870A form, along with clarifications for each:

The California 5870A form is used to report tax on accumulation distributions from trusts. It should be attached to the beneficiary's tax return.

Accurate information is crucial. Ensure that the names, Social Security Numbers (SSNs), and trust details are correctly filled out to avoid delays.

Identify the taxable year for which the form is being completed. This is important for proper tax reporting and compliance.

Section A focuses on determining the average income and computation years. Carefully follow the steps to calculate the taxable amounts.

Be aware of the tax implications. The form requires calculations related to prior years’ distributions, which may affect the current tax liability.

For distributions accumulated over five years or more, complete Section A. If accumulated for less than five years, use Section B.

Review the instructions thoroughly before submission. Proper understanding of the form can prevent errors and potential audits.