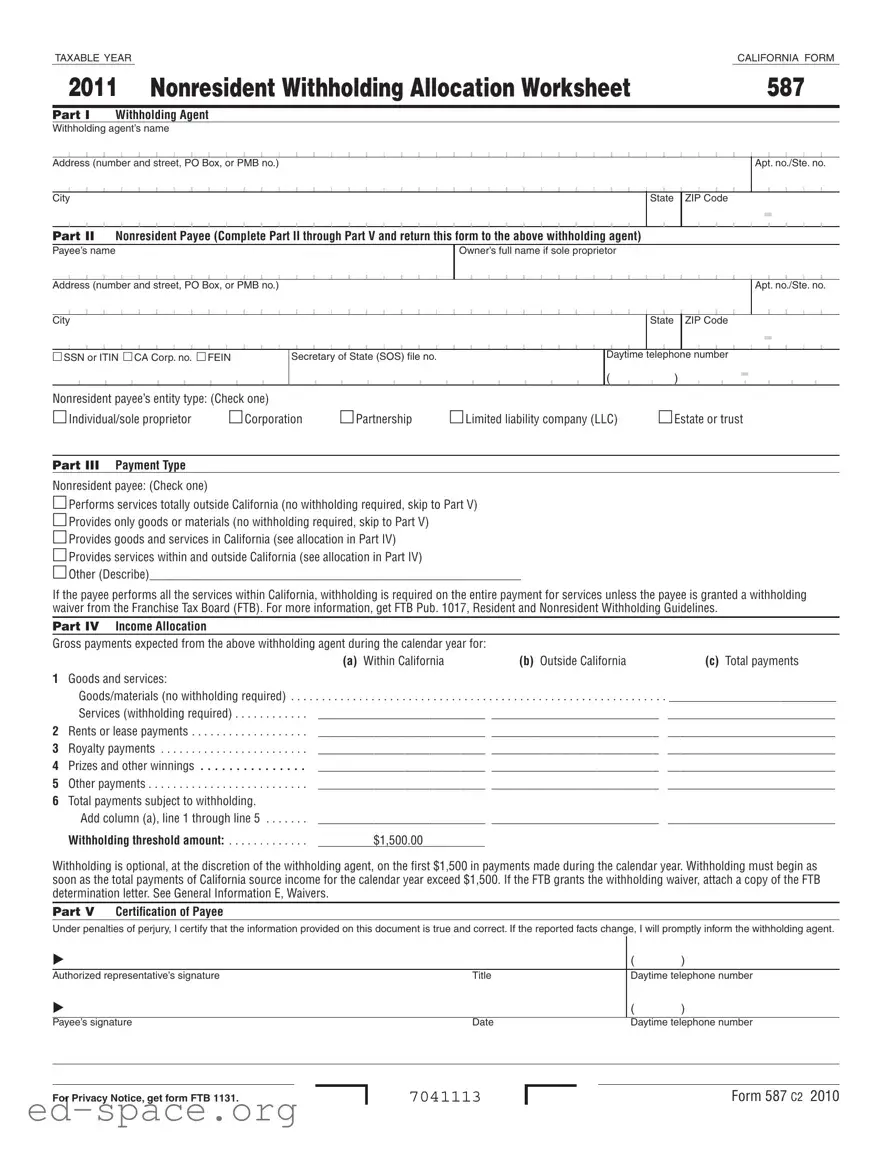

The California 587 form, known as the Nonresident Withholding Allocation Worksheet, serves a crucial role in determining the withholding tax obligations for payments made to nonresidents. This form is structured into several parts, each focusing on specific information that needs to be provided by both the withholding agent and the nonresident payee. In Part I, the withholding agent must detail their contact information, while Part II requires the nonresident payee to provide their name, address, and taxpayer identification details. The form also categorizes the payee's entity type, which can range from individuals to corporations. Part III addresses the nature of the payment, distinguishing between services performed entirely outside California and those that occur within the state. The importance of accurately reporting income allocation is emphasized in Part IV, where the payee must specify expected gross payments from the withholding agent, both for services rendered in California and elsewhere. Lastly, Part V includes a certification section, where the payee affirms the accuracy of the information provided under penalties of perjury. Understanding the nuances of Form 587 is essential for compliance with California's tax regulations and for ensuring proper withholding practices are followed.

TAXABLE YEARCALIFORNIA FORM

2011 Nonresident Withholding Allocation Worksheet |

587 |

Part I Withholding Agent

Withholding agent’s name

Address (number and street, PO Box, or PMB no.)

Apt. no./Ste. no.

City

State ZIP Code

-

Part II Nonresident Payee (Complete Part II through Part V and return this form to the above withholding agent)

Payee’s name

Owner’s full name if sole proprietor

Address (number and street, PO Box, or PMB no.)

Apt. no./Ste. no.

City |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

ZIP Code |

|||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SSN or ITIN CA Corp. no. FEIN |

Secretary of State (SOS) file no. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daytime telephone number |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

|

|

|

) |

|

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonresident payee’s entity type: (Check one) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

Individual/sole proprietor |

|

|

|

Corporation |

|

|

|

Partnership |

|

Limited liability company (LLC) |

|

|

Estate or trust |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Part III Payment Type

Nonresident payee: (Check one)

Performs services totally outside California (no withholding required, skip to Part V)

Provides only goods or materials (no withholding required, skip to Part V)

Provides goods and services in California (see allocation in Part IV)

Provides services within and outside California (see allocation in Part IV)

Other (Describe)____________________________________________________________

If the payee performs all the services within California, withholding is required on the entire payment for services unless the payee is granted a withholding waiver from the Franchise Tax Board (FTB). For more information, get FTB Pub. 1017, Resident and Nonresident Withholding Guidelines.

Part IV Income Allocation

Gross payments expected from the above withholding agent during the calendar year for:

|

|

(a) Within California |

(b) Outside California |

(c) Total payments |

1 |

Goods and services: |

|

|

|

|

Goods/materials (no withholding required) |

___________________________ |

||

|

Services (withholding required) |

___________________________ ___________________________ |

___________________________ |

|

2 |

Rents or lease payments |

___________________________ ___________________________ |

___________________________ |

|

3 |

Royalty payments |

___________________________ ___________________________ |

___________________________ |

|

4 |

Prizes and other winnings |

___________________________ ___________________________ |

___________________________ |

|

5 |

Other payments |

___________________________ ___________________________ |

___________________________ |

|

6 |

Total payments subject to withholding. |

|

|

|

|

Add column (a), line 1 through line 5 |

___________________________ ___________________________ |

___________________________ |

|

|

Withholding threshold amount: |

$1,500.00 |

|

|

Withholding is optional, at the discretion of the withholding agent, on the first $1,500 in payments made during the calendar year. Withholding must begin as soon as the total payments of California source income for the calendar year exceed $1,500. If the FTB grants the withholding waiver, attach a copy of the FTB determination letter. See General Information E, Waivers.

Part V Certiication of Payee

Under penalties of perjury, I certify that the information provided on this document is true and correct. If the reported facts change, I will promptly inform the withholding agent.

|

|

|

( |

) |

Authorized representative’s signature |

Title |

Daytime telephone number |

||

|

|

|

( |

) |

Payee’s signature |

Date |

Daytime telephone number |

||

For Privacy Notice, get form FTB 1131.

7041113

Form 587 C2 2010

Instructions for Form 587

Nonresident Withholding Allocation Worksheet

References in these instructions are to the California Revenue and Taxation Code (R&TC).

General Information

Beginning January 1, 2008, domestic nonresidents may use Form 589, Nonresident Reduced Withholding Request, to request the reduction in the standard seven percent withholding amount that is applicable to California source payments made to nonresidents.

Backup Withholding – Beginning on or after January 1, 2010, with certain limited exceptions, payers that are required to withhold and remit backup withholding to the Internal Revenue Service (IRS) are also required to withhold and remit to the Franchise Tax Board (FTB). The California backup withholding rate is 7% of the payment. For California purposes, dividends, interests, and any financial institutions, release of loan funds made in the normal course of business are exempt from backup withholding.

If a payee has backup withholding, the payee must contact the FTB to provide a valid Taxpayer Identification Number (ITIN) before filing a tax return. The following are acceptable TINs: social security number (SSN); individual taxpayer identification number (ITIN); federal employer identification number (FEIN); California corporation number (CA Corp No.); or California Secretary of State (SOS) file number. Failure to provide a valid TIN will result in the denial of

the backup withholding credit. For more information, go to ftb.ca.gov and search for backup withholding.

Private Mail Box (PMB) – Include the PMB in the address field. Write “PMB” first, then the box number. Example: 111 Main Street PMB 123.

Foreign Address – Enter the information in the following order: City, Country, Province/Region, and Postal Code. Follow the country’s practice for entering the postal code. Do not abbreviate the country’s name.

A Purpose

Use Form 587, Nonresident Withholding Allocation Worksheet, to determine

the amount of withholding required on payments to nonresidents.

The payee completes, signs, and returns Form 587 to the withholding agent. The withholding agent relies on the certification made by the payee to

determine the amount of withholding required, provided the completed and signed Form 587 is accepted in good faith. Retain the completed Form 587 for your records for a minimum of four years and provide it to the FTB upon request.

Do not use Form 587 if any of the following applies:

•Payment to a nonresident is only for the purchase of goods.

•You sold California real estate. Use Form

•The payee is a resident of California or is a

Use Form 590, Withholding Exemption Certificate.

•The payee is a corporation, partnership, or limited liability company (LLC) that has a permanent place of business in California or is qualified to do business in California. Foreign corporations must be qualified to transact intrastate business. Use Form 590.

•The payment is to an estate and the decedent was a California resident. Use Form 590.

B Requirement

California Revenue and Taxation Code (R&TC) Section 18662 and the related regulations require withholding of income or franchise tax on certain payments made to nonresidents of California for personal services performed in California and for rents on property located in California and royalties with activities in California. The withholding rate is seven percent (.07) unless the FTB grants a waiver. See General Information E, Waivers.

C When to File This Form

The withholding agent requests that the payee completes, signs, and returns Form 587 when a contract is entered into or before payment is made to the payee. The withholding agent retains Form 587 for a minimum of four years and must provide it to the FTB upon request.

Form 587 remains valid for the duration of the contract (or term of payments), provided there is no material change in the facts. By signing Form 587, the payee agrees to promptly notify the withholding agent of any changes in the facts.

D Withholding Requirements

Payments made to nonresident payees (including individuals, corporations, partnerships, LLCs, estates, and trusts) are subject to withholding. However, no withholding is required if total payments of California source income to the payee during the calendar year are $1,500 or less.

If the California resident, qualified corporation, LLC, or partnership is acting as an agent for the nonresident payee, the payment is subject to withholding if the nonresident payee does not meet any of the exceptions on Form 590.

Payments subject to withholding include the following:

•Payments for services performed in California by nonresidents.

•Payments made in connection with a California performance.

•Rent paid to nonresidents if the rent is paid in the course of the withholding agent’s business.

•Royalties paid to nonresidents from business activities in California.

•Payments of prizes for contests entered in California.

•Distributions of California source income to nonresident beneficiaries from an estate or trust.

•Other payments of California source income made to nonresidents.

Payments not subject to withholding include payments:

•To a resident of California or to a corporation with a permanent place of business in California.

•To a corporation qualified to do business in California.

•To a partnership or LLC that has a permanent place of business in California.

•For sale of goods.

•For income from intangible personal property, such as interest and dividends, unless the property has acquired a business situs in California.

•For services performed outside of California.

•To a payee that is a

Form 587 Instructions 2010 Page 1

•Representing wages paid to employees. Wage withholding is administered

by the California Employment Development Department (EDD). For more information, contact your local EDD office.

•To a payee that is a government entity.

•To reimburse a payee for expenses relating to services performed in California if the reimbursement is separately accounted for and not subject to federal Form 1099 reporting. Corporate payees, for purposes of this exception, are treated as individual persons.

E Waivers

A nonresident payee may request that withholding be waived. To apply for a withholding waiver, use Form 588, Nonresident Withholding Waiver Request. If the FTB has granted a waiver, you must attach a copy of FTB’s determination letter to Form 587.

FRequirement to File a California Tax Return

A payee’s exemption certification on Form 587, Form 590, or a determination letter from the FTB waiving withholding does not eliminate the requirement to file a California tax return and pay the tax due. For return filing requirements, see the instructions for Long or Short Form 540NR, California Nonresident or

Specific Instructions

Part I – Withholding Agent

The withholding agent must complete Part I before giving Form 587 to the payee.

Part II – Nonresident Payee

The payee must complete all information in Part II including the social security number, individual taxpayer identification number, California corporation number, FEIN, or SOS file number, and entity type.

Part III – Payment Type

The nonresident payee must check the box that identifies the type of payment being received.

No withholding is required when payees are residents or have a permanent place of business in California.

Part IV – Income Allocation

Use Part IV to identify payments that are subject to withholding. Only payments sourced within California are subject

to withholding. Services performed in California are sourced in California. In the case of payments for services performed when part of the services are performed outside California, enter the amount paid for performing services within California in column (a). Enter the amount paid for performing services while outside California in column (b). Enter the total amount paid for services in column (c).

If the payee’s trade, business, or profession carried on in California is an integral part of a unitary business carried on within and outside California, the amounts included on line 1 through line 5 should be computed by applying the payee’s California apportionment percentage (determined in accordance with the provisions of the Uniform Division of Income for Tax Purposes Act) to the payment amounts. For more information on apportionment, get California Schedule R, Apportionment and Allocation of Income.

Withholding agent. Withholding is optional, at your discretion, on the first $1,500 in payments made during the calendar year. Withholding must begin as soon as the total payments of California source income for the calendar year exceed $1,500. If circumstances change during the year (such as the total amount of payments), which would change the amount on line 6, the payee must submit a new Form 587 to the withholding agent reflecting those changes. The withholding agent should evaluate the need for a new Form 587 when a change in facts occurs.

Part V – Certification of Payee

The payee and/or the authorized representative must complete, sign, date, and return this form to the withholding agent.

Authorized representatives include those persons the payee authorized to act on their behalf through a power of attorney, third party designee, or other individual taxpayers authorized to view their confidential tax data via a waiver or release.

Additional Information

For additional information or to speak to a representative regarding this form, call the Withholding Services and Compliance automated telephone service at:

888.792.4900, or 916.845.4900 FAX 916.845.9512

OR write to:

WITHHOLDING SERVICES AND COMPLIANCE MS F182 FRANCHISE TAX BOARD

PO BOX 942867 SACRAMENTO CA

You can download, view, and print California tax forms and publications at ftb.ca.gov.

OR write to:

TAX FORMS REQUEST UNIT MS F284 FRANCHISE TAX BOARD

PO BOX 307

RANCHO CORDOVA CA

For all other questions unrelated to withholding or to access the TTY/TDD numbers, see the information below.

Internet and Telephone Assistance Website: ftb.ca.gov

Telephone: 800.852.5711 from within the United States 916.845.6500 from outside the United States

TTY/TDD: 800.822.6268 for persons with hearing or speech impairments

Asistencia Por Internet y Teléfono Sitio web: ftb.ca.gov

Teléfono: 800.852.5711 dentro de los

Estados Unidos 916.845.6500 fuera de los Estados Unidos

TTY/TDD: 800.822.6268 personas con discapacidades auditivas y del habla

By Automated Phone Service: Use this service to check the status of your refund, order California forms, obtain payment and balance due information, and hear recorded answers to general questions. This service is available 24 hours a day, 7 days a week, in English and Spanish.

Telephone: 800.338.0505 from within the United States 916.845.6600 from outside the United States

Follow the recorded instructions. Have paper and pencil available to take notes.

Page 2 Form 587 Instructions 2010

| Fact Name | Description |

|---|---|

| Purpose | Form 587 is used to determine the amount of withholding required on payments to nonresidents for services performed in California. |

| Governing Law | The form is governed by the California Revenue and Taxation Code (R&TC) Section 18662. |

| Filing Requirement | The withholding agent must request Form 587 to be completed before payment is made to the nonresident payee. |

| Withholding Rate | The standard withholding rate is 7% on payments made to nonresidents unless a waiver is granted by the Franchise Tax Board (FTB). |

| Minimum Payment Threshold | No withholding is required if total payments to the nonresident payee are $1,500 or less during the calendar year. |

| Certification | The payee must certify the accuracy of the information provided on Form 587 under penalties of perjury. |

| Retention Period | The withholding agent must retain completed Form 587 for a minimum of four years. |

| Exemptions | Payments to certain entities, such as California residents or corporations with a permanent business in California, are exempt from withholding. |

| Waiver Application | Nonresident payees may request a withholding waiver using Form 588, which must be attached to Form 587 if granted. |

After completing the California 587 form, submit it to the withholding agent. They will use this information to determine the appropriate withholding amounts for payments made to nonresidents. Ensure that all sections are filled out accurately to avoid any delays or issues.

What is the purpose of the California Form 587?

The California Form 587, also known as the Nonresident Withholding Allocation Worksheet, is used to determine the amount of withholding required on payments made to nonresidents. It helps the withholding agent assess whether withholding is necessary based on the type of payment and the location where services are performed. The payee must complete, sign, and return this form to the withholding agent, who will rely on the information provided to ensure compliance with California tax laws.

Who needs to fill out Form 587?

Form 587 must be completed by nonresident payees who receive payments for services performed in California or for other California source income. This includes individuals, corporations, partnerships, limited liability companies (LLCs), estates, and trusts. If the payee is a resident of California or has a permanent place of business in the state, they do not need to use this form. The withholding agent also plays a role by completing the first part of the form before providing it to the payee.

What are the withholding requirements for payments made to nonresidents?

Payments made to nonresident payees are generally subject to a withholding rate of 7% for services performed in California. However, if the total payments for California source income to the payee during the calendar year are $1,500 or less, no withholding is required. The withholding agent has the discretion to withhold on the first $1,500, but must begin withholding once the total exceeds this threshold. Payments for goods or services performed entirely outside of California are not subject to withholding.

How does a nonresident payee request a withholding waiver?

A nonresident payee can request a withholding waiver by submitting Form 588, the Nonresident Withholding Waiver Request. If granted, the payee must attach a copy of the Franchise Tax Board's (FTB) determination letter to Form 587 when submitting it to the withholding agent. It is important to note that receiving a waiver does not eliminate the requirement for the payee to file a California tax return and pay any taxes due.

Incomplete Information: Many people forget to fill out all required fields. Missing details like the payee's social security number or address can lead to delays or rejections.

Incorrect Payment Type: Selecting the wrong payment type can create confusion. It's crucial to accurately check the box that reflects the nature of the payment being received.

Failure to Sign: Some individuals neglect to sign the form. Without a signature, the form is not valid and will not be processed.

Ignoring Changes: If circumstances change, such as the total amount of payments, it's important to submit a new Form 587. Ignoring this requirement can result in incorrect withholding.

Incorrect Income Allocation: Miscalculating the income allocation can lead to withholding errors. Ensure that amounts are correctly divided between California and non-California sources.

The California Form 587, known as the Nonresident Withholding Allocation Worksheet, is essential for determining withholding amounts on payments made to nonresidents. However, it is often accompanied by several other forms and documents that help clarify tax obligations and ensure compliance with state regulations. Below is a list of common forms that may be used in conjunction with Form 587, each serving a specific purpose in the withholding process.

Understanding these forms and their purposes is crucial for nonresidents and withholding agents alike. Each document plays a vital role in ensuring that tax obligations are met while providing clarity and guidance through the withholding process. Properly completing and submitting these forms can help avoid complications and ensure compliance with California tax laws.

When dealing with nonresident withholding in California, the California Form 587 serves a specific purpose. However, there are other forms that share similarities with it. Here’s a look at ten documents that are comparable to the California Form 587, along with their key similarities:

Each of these forms plays a crucial role in the broader context of tax compliance and withholding, helping to ensure that both payees and withholding agents meet their obligations under California tax law.

When filling out the California Form 587, it is essential to approach the task with care and attention to detail. Here are four important guidelines to follow, along with some common pitfalls to avoid.

This form is applicable to various entities, including corporations, partnerships, and limited liability companies (LLCs). It is not limited to individual payees.

Withholding is required on payments made to nonresidents for services performed within California, unless specific exemptions apply.

The standard withholding rate is 7%, but this may vary based on the type of payment and whether a waiver has been granted by the Franchise Tax Board (FTB).

Form 587 is required only when payments exceed $1,500 during the calendar year. For amounts below this threshold, withholding is optional.

The withholding agent must complete Part I of the form and retain it for a minimum of four years. They are also responsible for ensuring that the form is properly filled out by the payee.

If there are any changes in the reported facts, the payee is required to inform the withholding agent and submit a new Form 587.

Submitting Form 587 does not exempt payees from the obligation to file a California tax return and pay any taxes due.

Both the payee and any authorized representative must sign Form 587 for it to be valid. A signature certifies the accuracy of the information provided.

Form 587 is not required for payments solely for the purchase of goods. However, if services are provided along with goods, the form may still be necessary.