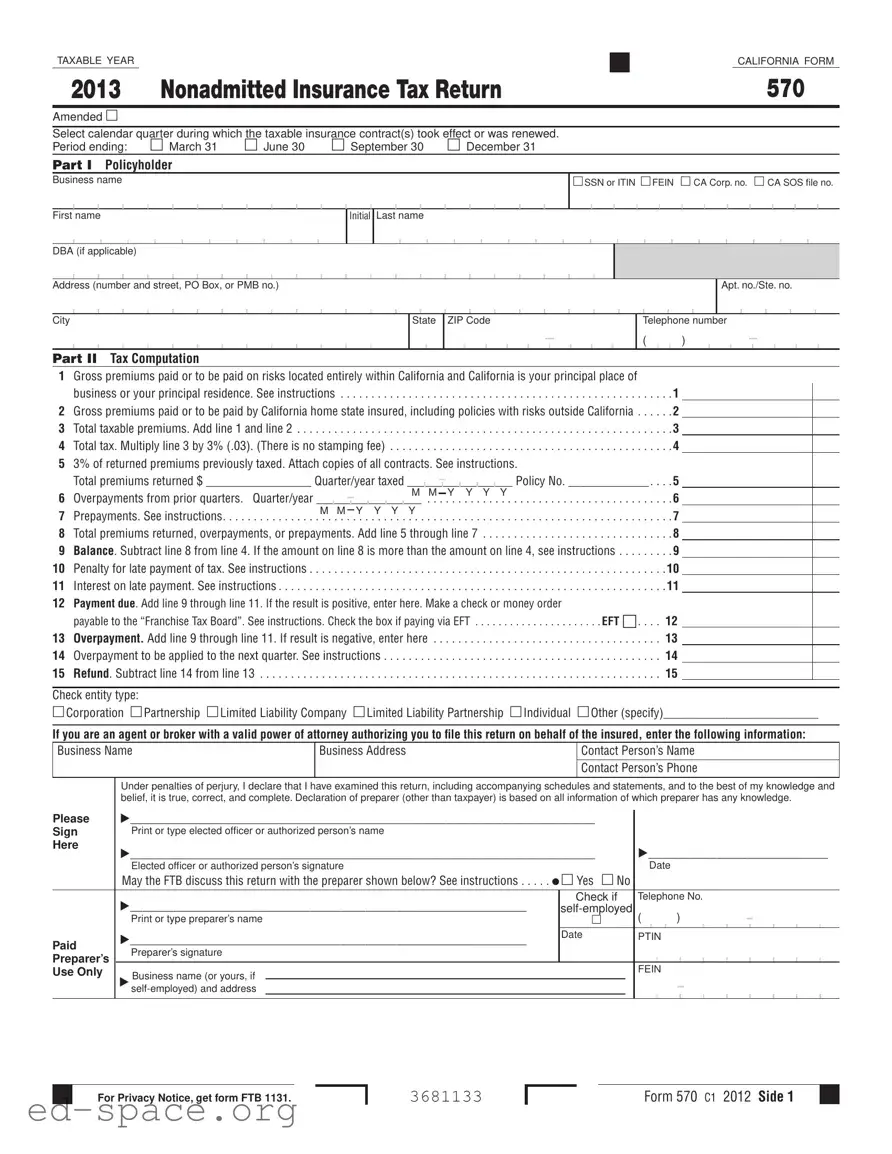

The California Form 570, also known as the Nonadmitted Insurance Tax Return, plays a critical role in the taxation of nonadmitted insurance contracts within the state. This form is required for individuals or businesses that engage with nonadmitted insurers, which are those not authorized to conduct insurance business in California. Each year, policyholders may need to file up to four returns, corresponding to the calendar quarters in which their insurance contracts take effect or are renewed. The form captures essential details, such as the policyholder's name, address, and identification numbers, alongside a comprehensive breakdown of gross premiums paid on risks located entirely within California and those involving California home state insureds. The tax rate is set at three percent of the total taxable premiums, and the form also allows for adjustments related to returned premiums, overpayments, and prepayments. It is imperative for filers to adhere to specific deadlines, as late submissions may incur penalties and interest. Additionally, the form provides space for reporting multiple insurance contracts, ensuring that policyholders can accurately disclose all relevant information. Understanding the nuances of Form 570 is essential for compliance and to avoid potential financial repercussions.

TAXABLE YEAR CALIFORNIA FORM

2013 |

NONADMITTED INSURANCE TAX RETURN |

570 |

|

|

|

Amended |

|

|

|

|

|

Select calendar quarter during which the taxable insurance contract(s) took effect or was renewed. |

|

|

Period ending: |

March 31 June 30 September 30 December 31 |

|

PART I Policyholder

Business name

First name

DBA (if applicable)

SSN or ITIN FEIN CA Corp. no. CA SOS file no.

Initial Last name

Address (number and street, PO Box, or PMB no.)

Apt. no./Ste. no.

City

State

ZIP Code

Telephone number

()

PART II Tax Computation

1Gross premiums paid or to be paid on risks located entirely within California and California is your principal place of

business or your principal residence. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Gross premiums paid or to be paid by California home state insured, including policies with risks outside California . . . . . . 2 3 Total taxable premiums. Add line 1 and line 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 4 Total tax. Multiply line 3 by 3% (.03). (There is no stamping fee) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

53% of returned premiums previously taxed. Attach copies of all contracts. See instructions.

|

Total premiums returned $ _________________ Quarter/year taxed _________________ Policy No. _____________ . . . |

. 5 |

|

|

|

M M Y Y Y Y |

|

6 |

Overpayments from prior quarters. Quarter/year _________________ |

. 6 |

|

|

|

M M Y Y Y Y |

|

7 |

Prepayments. See instructions |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. 7 |

8 |

Total premiums returned, overpayments, or prepayments. Add line 5 through line 7 |

. 8 |

|

9 |

Balance. Subtract line 8 from line 4. If the amount on line 8 is more than the amount on line 4, see instructions |

. 9 |

|

10 |

Penalty for late payment of tax. See instructions . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

10 |

11 |

Interest on late payment. See instructions |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

11 |

12Payment due. Add line 9 through line 11. If the result is positive, enter here. Make a check or money order

payable to the “Franchise Tax Board”. See instructions. Check the box if paying via EFT . . . . . . . . . . . . . . . . . . . . . . EFT n . . . . 12

13 Overpayment. Add line 9 through line 11. If result is negative, enter here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 14 Overpayment to be applied to the next quarter. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 15 Refund. Subtract line 14 from line 13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Check entity type:

Corporation Partnership Limited Liability Company Limited Liability Partnership Individual Other (specify)_________________________

If you are an agent or broker with a valid power of attorney authorizing you to file this return on behalf of the insured, enter the following information:

Business Name |

Business Address |

Contact Person’s Name |

|

|

|

|

|

Contact Person’s Phone |

|

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Please |

___________________________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Sign |

Print or type elected officer or authorized person’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Here |

___________________________________________________________________________ |

_____________________________ |

|||||||||||||||||||||||||

|

|||||||||||||||||||||||||||

|

Elected officer or authorized person’s signature |

|

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

May the FTB discuss this return with the preparer shown below? See instructions . . . . . Yes No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

________________________________________________________________ |

Check if |

Telephone No. |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

( |

|

|

|

|

|

|

) |

|

|

- |

|

|

|

|

|

|

||||||||||

|

Print or type preparer’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

________________________________________________________________ |

Date |

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Paid |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Preparer’s signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Preparer’s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Use Only |

Business name (or yours, if |

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Privacy Notice, get form FTB 1131.

3681133

Form 570 C1 2012 Side 1

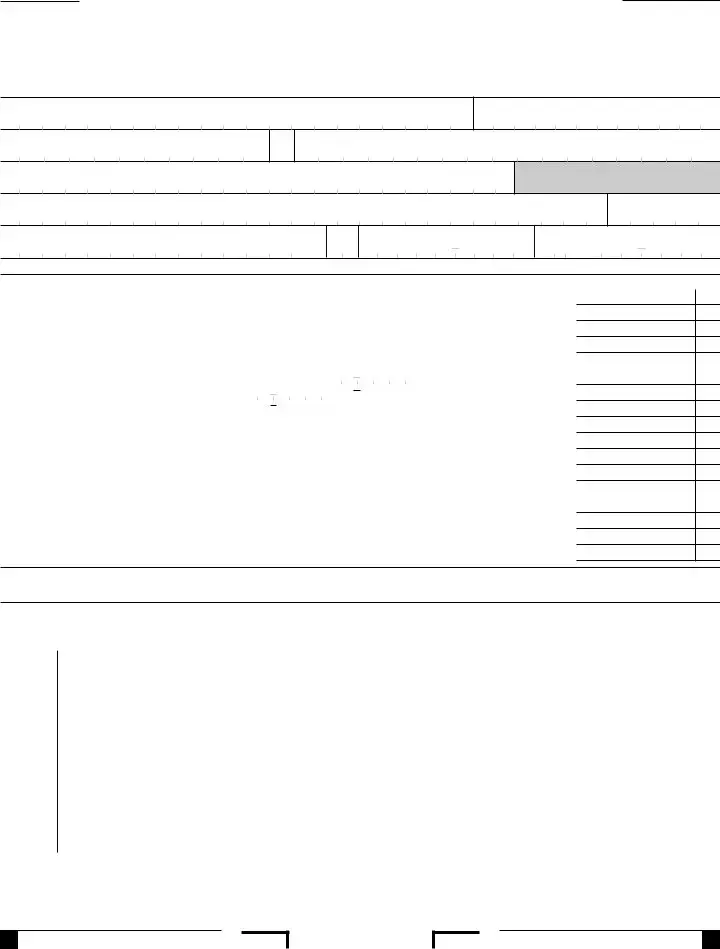

Policyholder Name: ________________________________________________________ Policyholder’s ID No.:________________________

PART III Insurance Contracts – If you have more than 24 policies to report, enter the additional policies on another Side 2 of Form 570. Total each Side 2 on the bottom separately. Do not create a schedule to report additional policies. We only accept and process official versions of Side 2 of Form 570.

|

|

|

|

PRINT CLEARLY |

|

|

|

|

|

a |

b |

c |

d |

e |

Policy Number |

Name of each Nonadmitted Insurance Company |

Type of Insurance Coverage |

Location of Risks |

Total Premium |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Side 2 Form 570 C1 2012

3682133

Instructions for Form 570

Nonadmitted Insurance Tax Return

References in these instructions are to the California Revenue and Taxation Code (R&TC) and the California Insurance Code.

What’s New

Do Not Round Cents to Dollars – On this form, do not round cents to the nearest whole dollar. Enter the amounts with dollars and cents.

General Information

A user of this form may have to file up to four Form 570 tax returns in one year if the user purchases nonadmitted insurance contracts in each calendar quarter.

Assembly Bill (AB) 315, effective July 21, 2011, conforms California law to the Nonadmitted and Reinsurance Reform Act (NRRA) that is part of the

is a change from when California only taxed premiums related to California risk. The NRRA only allows one state to tax a home state insured, so proration of premiums among the states for taxation no longer occurs.

For more information, go to ftb.ca.gov and search for nonadmitted insurance tax.

To receive nonadmitted insurance tax information by email, go to ftb.ca.gov and search for subscription services.

Definitions:

•Home state – the state where the insured maintains its principal place of business, or if individual, the individual’s principal residence; if 100% of the insured risk is located in a state outside the insured’s principal place

of business or principal residence, then it is where the greatest percent of the insured’s taxable premium for that insurance contract is allocated.

•Principal place of business – the state where the insured maintains its headquarters and where the insured’s

•Principal residence – the state where the insured resides for the greatest number of days during a calendar year; or if the insured’s principal residence is located outside the U.S., the state to which the greatest percentage

of the insured’s taxable premium for that insurance contract is allocated.

•Home state insured – or “home state insured applicant” – a person whose home state is California and who has received a certificate or evidence of coverage as set forth in Section 1764 of the Insurance Code or a policy as issued by an eligible surplus line insurer, or a person who is an applicant.

•Multistate risk – means a risk covered by a nonadmitted insurer with insured exposures in more than one state.

The total gross premium paid or to be paid for all nonadmitted insurance placed in a single transaction with one underwriter or group of underwriters, whether in one or more policies, in that calendar quarter during which the taxable insurance contract or contracts took effect or were renewed, is now the entire gross premium charged on all nonadmitted insurance for the California home state insured. Enter only premiums for policies related to risks within the U.S.

Private Mail Box (PMB) – Include the PMB in the address field. Write “PMB” first, then the box number. Example: 111 Main Street PMB 123.

Foreign Address – Enter the information in the following order: City, Country, Province/Region, and Postal Code. Follow the country’s practice for entering the postal code. Do not abbreviate the country’s name.

A Purpose

Use Form 570, Nonadmitted Insurance Tax Return, to determine the tax on premiums paid or to be paid to nonadmitted insurers on contracts covering risks. Also, use Form 570 to file an amended return. See Section E, Amended Returns, for more information.

B Who Must Pay Nonadmitted Insurance Tax

The tax is imposed on a home state insured who independently purchases or renews an insurance contract during the calendar quarter from an insurer, including

If you do not know if the insurer is authorized to conduct business in California, call the FTB Nonadmitted Insurance Desk at 916.845.7448.

The tax will not be imposed on any of the following:

•Insurance coverage for which a tax on the gross premium is due or has been paid by surplus line brokers pursuant to Insurance Code Section 1775.5 (surplus lines tax).

•Gross premiums on businesses governed by provisions of Insurance Code Section 1760.5 (reinsurance of the liability of an admitted insurer and marine, aircraft, and interstate railroad insurance).

•Insurance coverage for which a tax on the gross premium is due or has been paid by risk retention groups pursuant to Insurance Code Section 132.

Agents or brokers with a valid power of attorney to file a return on behalf of the insured must enter the requested information in the space below line 15.

C Tax Rate

The tax rate is three percent (.03). This rate is applied to the gross premium paid or to be paid, less premiums returned because of cancellation or reduction of premium on which a tax has been paid. Do not include a stamping fee.

D When and Where to File

File Form 570 on or before the first day of the third month following the close of any calendar quarter during which a nonadmitted insurance contract took effect or was renewed:

Contract effective date |

Return due date |

January - March |

June 1 |

April - June |

September 1 |

July - September |

December 1 |

October - December |

March 1 |

Mail Form 570 and payment to:

FRANCHISE TAX BOARD

PO BOX 942867

SACRAMENTO CA

EAmended Returns

Use Form 570 to file an amended return. File an amended return to correct an error on the original return or to claim a refund.

Check the “Amended” box at the top of the form. Attach a copy of the original return behind the amended return and write “copy” in red across the face of the original return. When completing line 1 through line 15 of the amended return, use the amounts that should have been reported on the original return.

Amended returns must be filed within four years of the original due date or within one year from the date of the overpayment, whichever period expires later.

Attach copies of all contracts for changes to correct an error on the original return or to claim a refund.

Do not file an amended return to claim returned premiums. See the Specific Line Instructions for line 5.

F Third Party Designee

If the entity wants to allow the FTB to discuss its 2013 return with the paid preparer who signed it, check the “Yes” box in the signature area of the return. This authorization applies only to the individual whose signature appears in the “Paid Preparer’s Use Only” section of the return. It does not apply to the business, if any, shown in that section.

If the “Yes” box is checked, the entity is authorizing the FTB to call the paid preparer to answer any questions that may arise during the processing of its return. The entity is also authorizing the paid preparer to:

Form 570 Instructions 2012 Page 1

•Give the FTB any information that is missing from the return.

•Call the FTB for information about the processing of the return or the status of any related refund or payments.

•Respond to certain FTB notices about math errors, offsets, and return preparation.

•The entity is not authorizing the paid preparer to receive any refund check, bind the entity to anything (including any additional tax liability), or otherwise represent the entity before the FTB.

The authorization will automatically end one year from the date this tax return was filed. If the entity wants to expand the paid preparer’s authorization, get form FTB 3520, Power of Attorney Declaration for the Franchise Tax Board. If the entity wants to revoke the authorization before it ends, notify the FTB in writing or call 800.852.5711.

Specific Instructions

Part I – Policyholder

Enter the business or individual policy holder name, Doing Business As (DBA), if applicable, address, and identification number. Print

all information using CAPITAL LETTERS. If completing Form 570 by hand, enter all the information requested using black or blue ink.

Part II – Tax Computation

Do not show net or negative amounts on line 1 through line 4 to account for returned premiums. See line 5 for returned premiums. Only use line 1 through line 4 to report taxable premiums paid or to be paid during the calendar quarter.

Line 1 – Enter all gross premiums paid or to be paid on risks located entirely within California for policies entered into or renewed during the calendar quarter.

Line 2 – Enter all gross premiums paid or to be paid by California home state insured for all policies issued by a nonadmitted insurer for coverage both inside and outside of California which were entered into or renewed during the calendar quarter. Note: Enter only premiums for policies related to risks within the U.S.

Line 5 – Enter three percent (.03) of the premiums returned during the calendar quarter because of cancellation or reduction of premiums on which nonadmitted insurance tax was paid.

Enter the quarter that the returned premiums were originally taxed. If the returned premiums are from more than one quarter or policy, attach a schedule showing the amount of returned premiums from each quarter and/or policy.

Returned premiums must be claimed on a return for the calendar quarter during which the returned premiums were received. Refunds resulting from returned premiums must be claimed within four years from the original due date of the return, four years from the date the return was filed or one year from the date of cancellation or reduction of premium, whichever is later.

If you are an agent or broker filing this return on behalf of the insured, the refund will be mailed to you in the name of the insured if a signed Power of Attorney is on file allowing the FTB to do so.

Attach copies of all contracts where there was a reduction of premiums returned or cancellation on which nonadmitted insurance tax was paid.

Line 6 – Enter the amount of overpayment you requested to be applied from a prior quarter that was not applied on a previously filed return. These payments may include amounts from an amended Form 570. Enter the calendar quarter and taxable year as

Line 7 – Enter any payments made before filing the return. If the return is being filed after the due date, see the instructions for line 10.

Line 9 – If the amount on line 4 is more than the amount on line 8, subtract line 8 from line 4 and enter the balance on line 9, you have tax due. If the amount on line 8 is more than the amount on line 4, subtract line 4 from line 8 and enter the result in brackets on line 9, your credits exceed your tax.

Line 10 – If you do not pay the tax due by the due date, a penalty of 10% of the amount of tax due will be imposed. Enter 10% of the amount of tax not paid by the due date. (A penalty of 25% of the amount of tax due will be imposed when nonpayment or late payment is due to fraud.)

Line 11 – Interest will be charged on any late payment and penalty from the due date to the date paid. Interest compounds daily and the interest rate is adjusted twice a year. If you do not include interest with your late payment or include only a portion of it, the FTB will compute the interest and bill you for it.

Line 12 – Enter the total amount due. Make your check or money order payable to the “Franchise Tax Board.” Write the calendar quarter (March, June, September, or December), the applicable taxable year, Form 570, and your social security number (SSN), individual taxpayer identification number (ITIN), California corporation number, federal employer identification number (FEIN), or California Secretary of State (SOS) file no. on the check or money order. Check the EFT box if you made your payment by EFT.

Electronic Funds Transfer (EFT) – To submit your nonadmitted insurance tax payment using EFT, use the following tax type code, EFT code 02020. You must use the correct EFT code to ensure proper credit to your FTB account.

Line 14 – Enter the amount of overpayment to be credited to your next quarter’s return.

Part III – Insurance Contracts

Column a – Enter the policy number for each contract. Enter only policies related to risks within the U.S.

Column b – Enter the name of all the Nonadmitted Insurance Companies for each contract.

Column c – Enter the type of insurance coverage provided by the contract.

Column d – Enter the full name or the two letter abbreviation of the state where the risk is located for each contract. If your policy covers more than one state, then use additional lines to list the locations of the risk separately.

Column e – Enter the total premium amount for each contract.

Total – Enter the total of Form 570, Side 2, column e.

Additional Information

If you have questions, contact: FTB Nonadmitted Insurance Desk at 916.845.7448 or call the Withholding Services and Compliance automated number at 888.792.4900.

OR write to:

WITHHOLDING SERVICES AND COMPLIANCE MS F182 FRANCHISE TAX BOARD

PO BOX 942867 SACRAMENTO CA

You can download, view, and print California tax forms and publications at ftb.ca.gov.

OR to get forms by mail write to:

TAX FORMS REQUEST UNIT MS F284 FRANCHISE TAX BOARD

PO BOX 307

RANCHO CORDOVA CA

For all other questions unrelated to withholding or to access the TTY/TDD numbers, see the information below.

Internet and Telephone Assistance

Website: |

ftb.ca.gov |

Telephone: 800.852.5711 from within the |

|

|

United States |

|

916.845.6500 from outside the |

|

United States |

TTY/TDD: |

800.822.6268 for persons with |

|

hearing or speech impairments |

Asistencia Por Internet y Teléfono |

|

Sitio web: |

ftb.ca.gov |

Teléfono: |

800.852.5711 dentro de los Estados |

|

Unidos |

|

916.845.6500 fuera de los Estados |

|

Unidos |

TTY/TDD: |

800.822.6268 personas con |

|

discapacidades auditivas y del habla |

Page 2 Form 570 Instructions 2012

| Fact Name | Description |

|---|---|

| Purpose of Form 570 | This form is used to report and calculate taxes on premiums paid to nonadmitted insurers covering risks in California. |

| Tax Rate | The tax rate for nonadmitted insurance is set at 3% of the gross premiums paid or to be paid. |

| Filing Frequency | Taxpayers may need to file Form 570 up to four times a year, corresponding to each calendar quarter. |

| Governing Laws | California Revenue and Taxation Code and California Insurance Code govern the use of Form 570. |

| Amended Returns | Form 570 can be amended to correct errors or claim refunds, but must be filed within four years of the original due date. |

| Who Must File | Home state insureds who purchase or renew nonadmitted insurance contracts must file this form. |

| Returned Premiums | Taxpayers can report returned premiums on line 5 of the form, which can reduce taxable amounts. |

| Payment Instructions | Payments should be made payable to the “Franchise Tax Board” and sent along with the form to the specified address. |

| Late Payment Penalties | A penalty of 10% applies to late payments, and interest will accrue on any unpaid tax. |

| Contact Information | For questions, taxpayers can reach the FTB Nonadmitted Insurance Desk at 916.845.7448. |

Completing the California Form 570 is essential for reporting nonadmitted insurance tax. This form must be filled out accurately to ensure compliance with California tax regulations. Follow the steps below to fill out the form correctly.

Once the form is completed, ensure all information is accurate and legible. Submit the form along with any payment to the address specified in the instructions. This ensures compliance with California's tax regulations and avoids potential penalties.

What is the purpose of the California Form 570?

The California Form 570, also known as the Nonadmitted Insurance Tax Return, is used to determine the tax owed on premiums paid or to be paid to nonadmitted insurers for contracts covering risks. This form is essential for individuals and businesses that independently purchase or renew insurance contracts during a calendar quarter from insurers not authorized to conduct business in California. It can also be used to file an amended return if necessary.

Who is required to file Form 570?

Individuals or businesses that qualify as "home state insureds" must file Form 570. A home state insured is defined as a person whose principal place of business or residence is in California and who has purchased nonadmitted insurance. If you are unsure whether your insurer is authorized to operate in California, you may contact the Franchise Tax Board (FTB) Nonadmitted Insurance Desk for assistance.

What is the tax rate for nonadmitted insurance premiums reported on Form 570?

The tax rate applied to the gross premiums paid or to be paid for nonadmitted insurance is three percent (3%). This rate is applied to the total gross premium amount, excluding any stamping fees. It's important to report only premiums related to risks located within the United States.

When is Form 570 due?

Form 570 must be filed on or before the first day of the third month following the close of any calendar quarter during which a nonadmitted insurance contract took effect or was renewed. For example, if a contract took effect between January and March, the return would be due by June 1. Timely filing is crucial to avoid penalties and interest on late payments.

How can one amend a previously filed Form 570?

To amend a previously filed Form 570, you must check the "Amended" box at the top of the form. Attach a copy of the original return behind the amended return and mark it as "copy" in red. The amended return should include the correct amounts that should have been reported initially. Be mindful that amended returns must be filed within four years of the original due date or within one year from the date of the overpayment, whichever is later.

What information is required on Form 570 regarding insurance contracts?

Form 570 requires detailed information about each insurance contract. This includes the policy number, the name of the nonadmitted insurance company, the type of insurance coverage, the location of risks, and the total premium for each contract. If there are more than 24 policies to report, additional pages (Side 2 of Form 570) must be used. Accurate reporting is essential for proper tax assessment.

Incorrect Identification Numbers: One common mistake is entering the wrong identification number, such as the Social Security Number (SSN), Individual Taxpayer Identification Number (ITIN), or Federal Employer Identification Number (FEIN). This can lead to processing delays or rejections.

Failure to Report All Premiums: Some individuals neglect to include all gross premiums paid or to be paid. Ensure that you account for all premiums related to risks located entirely within California and those from California home state insureds.

Misunderstanding Tax Computation: Miscalculating the total tax due is another frequent error. Remember to multiply the total taxable premiums by the correct tax rate of 3%. Double-check your math to avoid penalties.

Ignoring Instructions for Returned Premiums: Many filers forget to follow the specific instructions for reporting returned premiums. It's crucial to attach copies of all contracts related to any returned premiums claimed.

Late Filing or Payment: Failing to file the form by the due date can incur penalties. Be aware of the filing deadlines for each quarter and ensure timely submission to avoid additional fees.

The California Form 570, also known as the Nonadmitted Insurance Tax Return, is essential for individuals and businesses engaged in nonadmitted insurance transactions. When filing this form, several other documents may be required to ensure compliance with California tax regulations. Below is a list of common forms and documents that often accompany the California Form 570.

Understanding these forms and documents is crucial for ensuring compliance with California tax laws related to nonadmitted insurance. Properly preparing and submitting all required paperwork can help prevent delays and potential penalties. Always consult with a tax professional for personalized guidance tailored to specific situations.

When filling out the California Form 570, it's essential to approach the task with care. Here are some important dos and don’ts to keep in mind to ensure your submission is accurate and complete.

By following these guidelines, you can help ensure that your Form 570 is processed smoothly and efficiently. If you have questions or need assistance, don’t hesitate to reach out to the appropriate resources for help.

This form is applicable to both individuals and businesses. Any person or entity that qualifies as a home state insured in California must file this return, regardless of their business structure.

The tax applies to all premiums related to insurance contracts for California home state insureds, even if the risks are located outside of California, as long as the insured maintains their principal place of business or residence in California.

The tax rate is fixed at three percent (0.03) of the gross premiums paid or to be paid. This rate is established by California law and is not subject to negotiation.

Filing is mandatory for any home state insured who purchases or renews a nonadmitted insurance contract during a calendar quarter. Failure to file can result in penalties and interest.

Returned premiums must be reported on the form. Line 5 specifically addresses premiums returned due to cancellation or reduction, and these amounts affect the overall tax calculation.

Amended returns must be filed within four years of the original due date or within one year from the date of overpayment, whichever period expires later. This time limitation is important to consider when making corrections.

When filling out and using the California Form 570, there are several important points to keep in mind. Here are some key takeaways:

By following these guidelines, you can navigate the process of completing and submitting the California Form 570 more effectively.