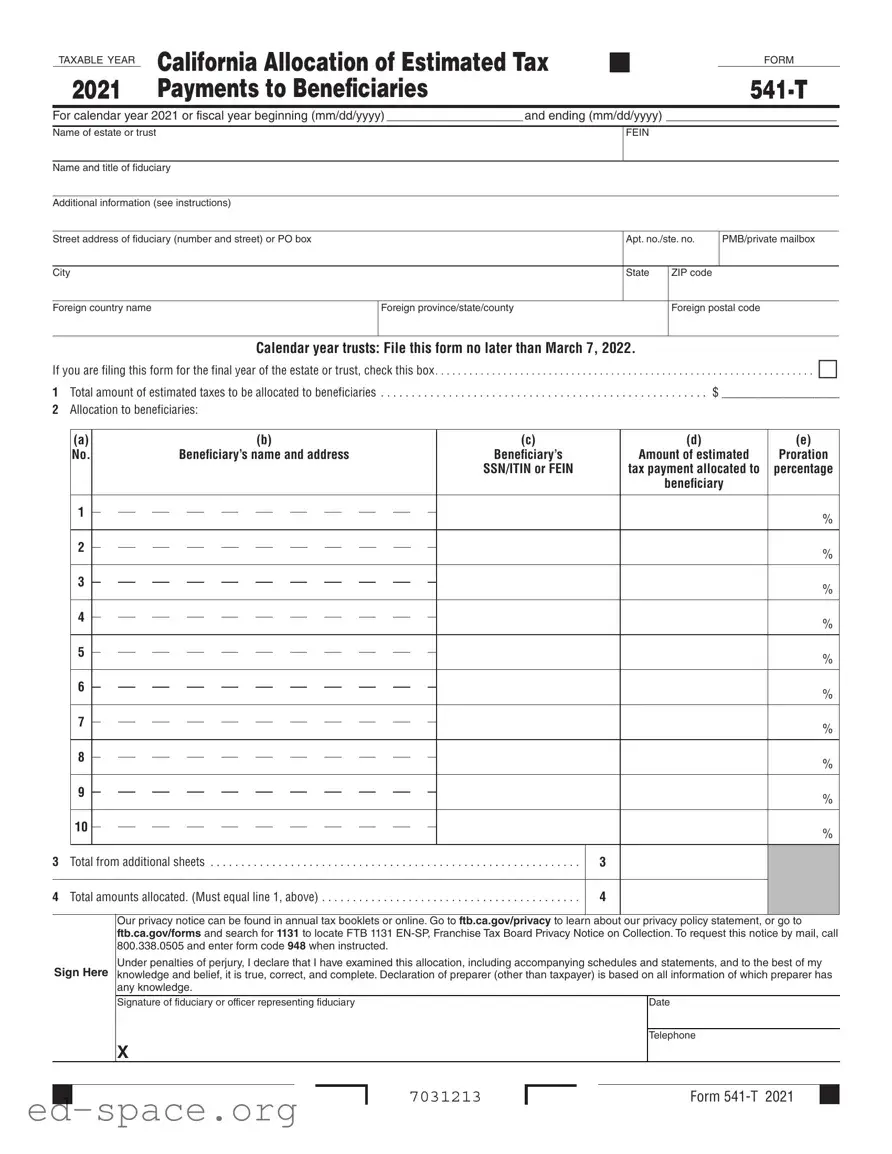

The California 541 T form serves as a crucial tool for fiduciaries managing estates or trusts that wish to allocate estimated tax payments to beneficiaries. This form enables the fiduciary to elect to treat part of the estimated tax payments made by the estate or trust as if they were made directly by the beneficiaries. It is important to note that this election, once made, is irrevocable. The form requires detailed information, including the fiduciary's name, address, and federal employer identification number (FEIN), as well as the names, addresses, and identifying numbers of the beneficiaries receiving the allocations. Additionally, the fiduciary must report the total estimated tax payments and specify how these payments are divided among the beneficiaries, ensuring that the total allocations equal the initial amount reported. The form must be filed separately from the California Fiduciary Income Tax Return (Form 541) and submitted to the Franchise Tax Board by a specific deadline, typically 65 days after the close of the tax year. Accurate completion of this form is essential to avoid penalties and ensure that beneficiaries receive their appropriate tax credits.

TAXABLE YEAR |

CALIFORNIA ALLOCATION OF ESTIMATED TAX |

■ |

|

FORM |

|

|

|

||

2021 |

Payments to Beneficiaries |

|

|

For calendar year 2021 or fiscal year beginning (mm/dd/yyyy) ____________________ and ending (mm/dd/yyyy) _________________________

Name of estate or trust

FEIN

Name and title of fiduciary

Additional information (see instructions)

Street address of fiduciary (number and street) or PO box |

|

Apt. no./ste. no. |

PMB/private mailbox |

|

|

|

|

|

I |

City |

|

State |

ZIP code |

|

|

|

|

|

|

Foreign country name |

Foreign province/state/county |

Foreign postal code |

||

|

I |

|

|

|

Calendar year trusts: File this form no later than March 7, 2022.

If you are filing this form for the final year of the estate or trust, check this box. |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . • |

|||||

1 Total amount of estimated taxes to be allocated to beneficiaries |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . $ ___________________ |

||||||

2 |

Allocation to beneficiaries: |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

(b) |

(c) |

(d) |

(e) |

|

|

|

No. |

|

Beneficiary’s name and address |

Beneficiary’s |

Amount of estimated |

Proration |

|

|

|

|

|

|

|

SSN/ITIN or FEIN |

tax payment allocated to |

percentage |

|

|

|

|

|

|

|

beneficiary |

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

% |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Total from additional sheets |

3 |

|

|||||

4 Total amounts allocated. (Must equal line 1, above) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

Sign Here

Our privacy notice can be found in annual tax booklets or online. Go to ftb.ca.gov/privacy to learn about our privacy policy statement, or go to ftb.ca.gov/forms and search for 1131 to locate FTB 1131

Under penalties of perjury, I declare that I have examined this allocation, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Signature of fiduciary or officer representing fiduciary |

Date |

Telephone

X

■

7031213

FORM |

■ |

| Fact Name | Description |

|---|---|

| Purpose | The California 541-T form allows a trust or decedent's estate to elect to treat part of its estimated tax payments as made by beneficiaries. |

| Governing Law | This form is governed by the Revenue and Taxation Code Section 17731 and the Internal Revenue Code Section 643(g)(1)(B). |

| Filing Deadline | Form 541-T must be filed by the 65th day after the close of the tax year for the election to be valid. |

| Where to File | Mail the completed form to the Franchise Tax Board at PO Box 942840, Sacramento, CA 94240-0002. |

| Final Year Indication | If filing for the final year of the estate or trust, a box must be checked on the form to indicate this status. |

| Estimated Tax Allocation | The total estimated taxes allocated to beneficiaries must equal the amount reported on line 1 of the form. |

Filling out the California 541 T form requires careful attention to detail to ensure accurate reporting of estimated tax payments allocated to beneficiaries. The following steps outline the process for completing this form, which is essential for fiduciaries managing estates or trusts.

After completing the form, it must be filed separately from Form 541. The completed California 541 T form should be mailed to the Franchise Tax Board at the specified address. It is important to adhere to the filing deadline to ensure compliance with tax regulations.

What is the purpose of the California 541 T form?

The California 541 T form is used by trusts or decedents’ estates to elect to treat any part of their estimated tax payments as made by specific beneficiaries. This election is governed by both California and federal tax laws. Once the election is made, it cannot be revoked, making it crucial to understand its implications before filing.

Who needs to file the California 541 T form?

This form must be filed by the fiduciary of a trust or a decedent’s estate that wishes to allocate estimated tax payments to its beneficiaries. If you are managing an estate or trust and want to ensure that tax payments are credited to beneficiaries, filing this form is essential.

When is the California 541 T form due?

The form must be filed by the 65th day after the close of the tax year. For trusts operating on a calendar year, this means it is due by March 6 of the following year. If this date falls on a weekend or holiday, you should file on the next business day to ensure compliance.

How do I file the California 541 T form?

To file, you must complete the form and mail it separately from Form 541, the California Fiduciary Income Tax Return. Do not attach the 541 T form to the 541 form. Instead, send it directly to the Franchise Tax Board at the specified address.

What information do I need to provide on the form?

You will need to include details such as the total amount of estimated taxes to be allocated, the names and addresses of beneficiaries, their Social Security Numbers (SSNs) or Federal Employer Identification Numbers (FEINs), and the amounts of estimated tax payments allocated to each beneficiary. Accurate information is crucial to avoid processing delays and potential penalties.

Can I allocate estimated tax payments to more than ten beneficiaries?

Yes, if you have more than ten beneficiaries, you can list them on an additional sheet that follows the same format as the main form. Make sure to include the fiduciary's name and FEIN on this additional sheet to ensure proper processing.

What happens if I fail to file the California 541 T form on time?

Failing to file the form by the deadline can result in penalties and complications for both the fiduciary and the beneficiaries. It’s essential to adhere to the filing requirements to avoid these issues and ensure that the tax payments are properly credited to the beneficiaries’ accounts.

Incorrectly Filling Out Beneficiary Information: Many people overlook the importance of accurately entering each beneficiary's name and address. Ensure that the information is complete and correctly spelled to avoid delays in processing.

Missing Social Security Numbers (SSNs) or Federal Employer Identification Numbers (FEINs): Failing to provide valid SSNs or FEINs for beneficiaries can lead to penalties and processing delays. Always double-check these numbers for accuracy.

Not Allocating Total Estimated Taxes Correctly: Line 4 must equal the total amount listed on line 1. Many individuals miscalculate or forget to check their math, which can result in significant issues.

Ignoring the Filing Deadline: The form must be filed by the 65th day after the close of the tax year. Missing this deadline can invalidate the election, so it's crucial to keep track of dates.

Not Separating Individual and Entity Beneficiaries: Grouping all beneficiaries together without distinguishing between individuals and entities can lead to confusion. Proper categorization helps ensure that the right information is submitted.

Failing to Sign the Form: A common oversight is neglecting to sign the form. The fiduciary's signature is essential for the form's validity. Without it, the form may be rejected.

The California 541 T form is essential for trusts and estates to allocate estimated tax payments to beneficiaries. However, it is often accompanied by several other documents that help clarify and support the information provided. Understanding these forms can simplify the process for fiduciaries and beneficiaries alike.

Each of these documents plays a significant role in the tax reporting process for trusts and estates in California. By understanding the purpose of each form, fiduciaries can navigate their responsibilities with greater confidence, ensuring that beneficiaries receive accurate information for their own tax filings.

The California 541 T form serves a specific purpose in the realm of tax allocation for trusts and estates. Several other documents share similarities with this form, particularly in their function of allocating income, deductions, or tax payments among beneficiaries. Below are five documents that are comparable to the California 541 T form, along with explanations of their similarities:

When filling out the California 541 T form, consider the following guidelines:

Conversely, avoid the following mistakes:

Misconceptions about the California 541 T Form

Here are some key takeaways for filling out and using the California 541 T form: