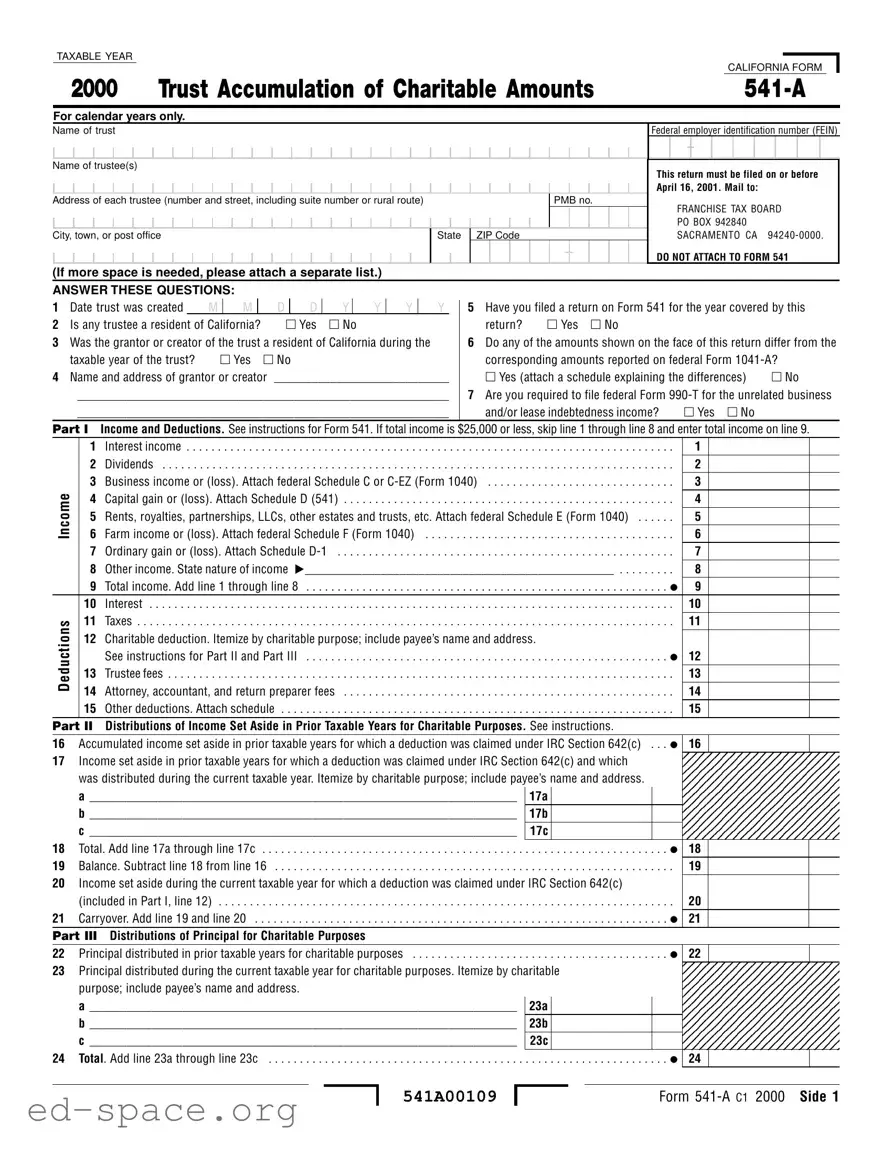

The California Form 541-A is an essential document for trustees managing charitable trusts or split-interest trusts. This form is specifically designed to report the accumulation of charitable amounts for a taxable year, ensuring compliance with California tax laws. It requires detailed information about the trust, including the name, federal employer identification number (FEIN), and the addresses of the trustees. The form also mandates answers to key questions regarding the trust's creation date, residency of trustees, and any discrepancies with federal tax filings. Furthermore, trustees must provide a comprehensive breakdown of income and deductions, detailing various sources such as interest, dividends, and business income. The form includes sections for reporting distributions made for charitable purposes, both from income set aside in prior years and from the principal. Notably, it must be filed by April 16 of the following year, although an automatic six-month extension is available. By completing this form accurately, trustees can ensure that they meet their reporting obligations while also supporting the charitable purposes of their trust.

TAXABLE YEAR

|

|

CALIFORNIA FORM |

2000 |

TRUST ACCUMULATION OF CHARITABLE AMOUNTS |

For calendar years only.

Name of trust

Federal employer identification number (FEIN)

-

Name of trustee(s)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of each trustee (number and street, including suite number or rural route) |

|

|

|

|

|

|

PMB no. |

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, town, or post office |

State |

ZIP Code |

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This return must be filed on or before April 16, 2001. Mail to:

FRANCHISE TAX BOARD PO BOX 942840 SACRAMENTO CA

DO NOT ATTACH TO FORM 541

(If more space is needed, please attach a separate list.)

ANSWER THESE QUESTIONS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

1 Date trust was created |

|

M |

M |

|

D |

|

D |

|

Y |

|

Y |

Y |

|

Y |

|

5 |

Have you filed a return on Form 541 for the year covered by this |

||||||||||

2 Is any trustee a resident of California? |

|

|

Yes |

No |

|

|

|

|

|

|

return? |

Yes |

No |

|

|

|

|

|

|||||||||

3 Was the grantor or creator of the trust a resident of California during the |

|

|

6 |

Do any of the amounts shown on the face of this return differ from the |

|||||||||||||||||||||||

|

taxable year of the trust? |

|

Yes |

No |

|

|

|

|

|

|

|

|

|

|

corresponding amounts reported on federal Form |

|

|

||||||||||

4 Name and address of grantor or creator |

____________________________ |

|

Yes (attach a schedule explaining the differences) |

No |

|||||||||||||||||||||||

|

____________________________________________________________ |

|

7 |

Are you required to file federal Form |

|||||||||||||||||||||||

|

____________________________________________________________ |

|

|

and/or lease indebtedness income? |

Yes |

No |

|

|

|||||||||||||||||||

PART I |

Income and Deductions. See instructions for Form 541. If total income is $25,000 or less, skip line 1 through line 8 and enter total income on line 9. |

||||||||||||||||||||||||||

|

|

1 |

Interest income |

. . . . . . |

. . |

. . . |

. |

. . . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

1 |

|

|

|

|

||

|

|

2 |

. . .Dividends . . . . |

. . . |

. . . . . . |

. . |

. . . |

. |

. . . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

2 |

|

|

|

|

|

|

|

3 |

Business income or (loss). Attach federal Schedule C or |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

3 |

|

|

|

|

||||||||||||||||

Income |

|

4 |

Capital gain or (loss). Attach Schedule D (541) |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

4 |

|

|

|

|

||||||||

|

5 |

. . . . . .Rents, royalties, partnerships, LLCs, other estates and trusts, etc. Attach federal Schedule E (Form 1040) |

5 |

|

|

|

|

||||||||||||||||||||

|

6 |

. .Farm income or (loss). Attach federal Schedule F (Form 1040) |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

6 |

|

|

|

|

||||||||||||||

|

|

7 |

.Ordinary gain or (loss). Attach Schedule |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

7 |

|

|

|

|

||||||||

|

|

8 |

Other income. State nature of income |

. . . . . . . . ._________________________________________________ |

8 |

|

|

|

|

||||||||||||||||||

|

|

9 |

Total income. Add line 1 through line 8 |

. . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . |

9 |

|

|

|

|

||||||

|

|

10 |

Interest |

. . . |

. . . . . . |

. . |

. . . |

. |

. . . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

10 |

|

|

|

|

|

Deductions |

|

11 |

. . .Taxes |

. . . |

. . . . . . |

. . |

. . . |

. |

. . . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

11 |

|

|

|

|

|

|

12 |

Charitable deduction. Itemize by charitable purpose; include payee’s name and address. |

|

|

|

|

|

|

|

||||||||||||||||||

|

|

See instructions for Part II and Part III |

. . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . |

12 |

|

|

|

|

|||||||

|

13 |

. . .Trustee fees . . . |

. . . |

. . . . . . |

. . |

. . . |

. |

. . . . |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

13 |

|

|

|

|

||

|

14 |

Attorney, accountant, and return preparer fees |

|

|

|

|

|

|

|

|

|

|

|

14 |

|

|

|

|

|||||||||

|

|

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

|

|

|

|

|||||||||||

|

|

15 |

. . . . . . .Other deductions. Attach schedule |

. . . |

. . |

. . . |

. . |

. . . . . |

. . . |

. . |

. . |

. . . . |

. . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . |

15 |

|

|

|

|

|||||||

PART II Distributions of Income Set Aside in Prior Taxable Years for Charitable Purposes. See instructions. |

|

|

|

|

|

||||||||||||||||||||||

16 |

|

Accumulated income set aside in prior taxable years for which a deduction was claimed under IRC Section 642(c) . . . |

16 |

|

|

|

|

||||||||||||||||||||

17Income set aside in prior taxable years for which a deduction was claimed under IRC Section 642(c) and which

|

was distributed during the current taxable year. Itemize by charitable purpose; include payee’s name and address. |

|

|

a _____________________________________________________________________ |

17a |

|

b _____________________________________________________________________ |

17b |

|

c _____________________________________________________________________ |

17c |

18 |

Total. Add line 17a through line 17c |

. . . . . . . . . . . . . . . . . . . . . . 18 |

19 |

Balance. Subtract line 18 from line 16 |

. . . . . . . . . . . . . . . . . . . . . . . 19 |

20 |

Income set aside during the current taxable year for which a deduction was claimed under IRC Section 642(c) |

|

|

(included in Part I, line 12) |

. . . . . . . . . . . . . . . . . . . . . . . 20 |

21 |

Carryover. Add line 19 and line 20 |

. . . . . . . . . . . . . . . . . . . . . . 21 |

PART III Distributions of Principal for Charitable Purposes |

|

|

22 |

Principal distributed in prior taxable years for charitable purposes |

. . . . . . . . . . . . . . . . . . . . . . 22 |

23 |

Principal distributed during the current taxable year for charitable purposes. Itemize by charitable |

|

|

purpose; include payee’s name and address. |

|

|

a _____________________________________________________________________ |

23a |

|

b _____________________________________________________________________ |

23b |

|

c _____________________________________________________________________ |

23c |

24 |

Total. Add line 23a through line 23c |

. . . . . . . . . . . . . . . . . . . . . . 24 |

|

541A00109 |

|

PART IV |

Balance Sheet. If line 9 is $25,000 or less, complete only line 38, line 42, and line 45. If books of account do not agree, please reconcile all differences. |

|

|

|

|||||||||||||||||||||

|

|||||||||||||||||||||||||

|

|

|

|

|

ASSETS |

|

|

|

|

|

(a) |

(b) |

|

||||||||||||

|

Cash — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

25 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

26 |

. . . . . . . . . . . . . . . . . . . .Savings and temporary cash investments |

. . . . |

. . . . . . . |

. . . . . . . . . . |

26 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

27 |

a |

. . . . . . . . . . .Accounts receivable |

. . . . . . . . . . . . . . . . . . . . . . |

27a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

. . . . . . . . . . . . . . . . . .b Less: allowance for doubtful accounts |

27b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

28 |

. . . . . . . . . . . . . . . . . . . . . . . . . . .a Notes and loans receivable |

28a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

. . . . . . . . . . . . . . . . . .b Less: allowance for doubtful accounts |

28b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

29 |

Inventories for sale or use |

. . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

. . . . . . . |

. . . . . . . . . . |

29 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

30 |

. . . . . . . . . . . . . . . . . . . . .Prepaid expenses and deferred charges |

. . . . |

. . . . . . . |

. . . . . . . . . . |

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

31 |

. . . . . . . . . . . . . . . . .Investments — U.S. and state government obligations. Attach schedule |

31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

Investments — corporate stock. Attach schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

32 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

32 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

33 |

. . . . . . . . . . . . .Investments — corporate bonds. Attach schedule |

. . . . |

. . . . . . . |

. . . . . . . . . . |

33 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

34 |

a |

Investments — land, buildings, and equipment: basis |

34a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

b |

. . . . . . . . . . . . . . . . . . . . . . .Less: accumulated depreciation |

34b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Investments — other. Attach schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

35 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

36 |

a |

Land, buildings, and equipment (trade or business): basis . . |

36a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

b |

. . . . . . . . . . . . . . . . . . . . . . .Less: accumulated depreciation |

36b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

37 |

Other assets. Describe. |

_____________________________________________________ |

37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

38 |

. . . . . . . . . . . . . . . . . . .Total assets. Add line 25 through line 37 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

39 |

Accounts payable and accrued expenses |

. . . . . |

. . . . . . |

. . . . . . . . . . |

39 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

40 |

. . . . . . . . . . .Mortgages and other notes payable. Attach schedule |

. . . . |

. . . . . . . |

. . . . . . . . . . |

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

41 |

Other liabilities. Describe. |

___________________________________________________ |

41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

42 |

. . . . . . . . . . . . . . . . .Total liabilities. Add line 39 through line 41 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

NET ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

43 Trust principal or corpus |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

. . . . . . . |

. . . . . . . . . . |

43 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. . . . . . . . . . . . . . . . . . . . . . . . . .44 Undistributed income and profits |

. . . . |

. . . . . . . |

. . . . . . . . . . |

44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

. . . . . . . . . . . . . . . . . . . .45 Total net assets. Add line 43 and line 44 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. . . . . . . .46 Total liabilities and net assets. Add line 42 and line 45 |

. . . . |

. . . . . . . |

. . . . . . . . . . |

46 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is |

|

|||||||||||||||||||||

Please |

|

true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

||||||||||||||||||||||

Sign |

|

|

|

|

|

|

|

|

|

|

Date |

Trustee’s SSN/FEIN |

|

||||||||||||

Here |

|

|

___________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

Signature of trustee or officer representing trustee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Date |

|

|

|

Paid preparer’s SSN/PTIN |

|

||||||||||||

Paid |

|

|

Preparer’s |

|

|

|

|

|

|

|

Check if self- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

employed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Preparer’s |

signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Use Only |

Firm’s name (or yours, if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Side 2 Form

541A00209

For Privacy Act Notice, get form FTB 1131.

Instructions for FTB Form

Trust Accumulation of Charitable Amounts

General Information

In general, California tax law conforms to the Internal Revenue Code (IRC) as of

January 1, 1998. However, there are continuing differences between California and federal tax law. California has not conformed to most of the changes made to the IRC by the federal Internal Revenue Service Restructuring and Reform Act of 1998 (Public Law

Law

A Purpose

Use Form

BWho Must File

A trustee must file a calendar year Form

A charitable trust is a trust which:

•Is not exempt from taxation under R&TC Section 23701d; and

•Has all the unexpired interests devoted to charitable purposes described in IRC Section 170(c); and

•Had a charitable contribution deduction allowed for all the unexpired interests under the R&TC.

A

•Is not exempt from taxation under R&TC Section 23701d; and

•Has some of the unexpired interests devoted to one or more charitable purposes described in IRC Section 170(c); and

•Has amounts in trust for which a chari- table contributions deduction was allowed under the R&TC. Pooled income funds (IRC Section 642(c)(5)), charitable remainder annuity trusts (IRC

Section 664(d)(1)), and remainder unitrusts (IRC Section 664(d)(2)), are considered

Simple trusts which received a letter from the Franchise Tax Board (FTB) granting exemption from tax under R&TC Section 23701d are considered to be corporations for tax purposes. They may be required to file Form 199, California Exempt Organization Annual Information Return. See the instructions for that form.

Nonexempt charitable trusts, described in IRC Section 4947(a)(1), must file Form 199.

Private Mailbox (PMB) No.

If you lease a mailbox from a private business rather than a PO box from the United States Postal Service, enter your PMB number in the field labeled “PMB no.”

CWhen to File

File Form

DWhere to File

Mail Form

FRANCHISE TAX BOARD PO BOX 942840 SACRAMENTO CA

Specific Instructions

Part II and Part III

Describe in detail on an attached statement the purpose for which charitable disburse- ments were made from income set aside in prior taxable years and amounts which were paid out of principal for charitable purposes. Examples of appropriate descriptions are: payments for nursing service, laboratory construction, fellowships, or assistance to indigent families (not simply charitable, educational, religious, or scientific).

Part IV

If the balance sheet does not agree with the books of account, all differences must be reconciled in an attached statement.

Form

| Fact Name | Detail |

|---|---|

| Purpose | The California Form 541-A is used to report charitable information required by Revenue and Taxation Code (R&TC) Section 18635. |

| Filing Deadline | This form must be filed on or before April 16, 2001. An automatic six-month extension is available without a request form. |

| Who Must File | A trustee must file Form 541-A for a trust claiming a charitable deduction under IRC Section 642(c) or for a charitable or split-interest trust. |

| Mailing Address | Form 541-A should be mailed to the Franchise Tax Board at PO Box 942840, Sacramento, CA 94240-0000. |

| Governing Law | The form is governed by California Revenue and Taxation Code (R&TC) Section 18635 and conforms to the Internal Revenue Code (IRC) as of January 1, 1998. |

Filling out the California 541 A form requires attention to detail and accuracy. Follow these steps to ensure you complete the form correctly. After filling out the form, it must be submitted to the Franchise Tax Board by the specified deadline.

What is the purpose of the California Form 541-A?

The California Form 541-A is designed to report charitable information required by the Revenue and Taxation Code Section 18635. This form is primarily used by trustees of charitable or split-interest trusts that claim deductions under IRC Section 642(c). It allows these trusts to report their income, deductions, and distributions related to charitable purposes.

Who is required to file Form 541-A?

A trustee must file Form 541-A for any trust that claims a charitable deduction under IRC Section 642(c) or for a charitable or split-interest trust. However, if the governing instrument and applicable local law require the trustee to distribute all income currently, then filing Form 541-A is not necessary for that taxable year. This includes charitable trusts and split-interest trusts that meet specific criteria set forth in the tax code.

When is Form 541-A due?

Form 541-A must be filed on or before April 16 of the year following the taxable year it covers. For example, if the trust's taxable year ends in 2000, the form must be submitted by April 16, 2001. If additional time is needed, California provides an automatic six-month extension without requiring a request form.

What information needs to be included in the form?

The form requires detailed information about the trust, including the name and address of the trustee, the date the trust was created, and whether any trustees are California residents. It also asks for specifics about income, deductions, and distributions related to charitable purposes. If there are discrepancies between amounts reported on Form 541-A and federal Form 1041-A, an explanation must be attached.

Where should Form 541-A be mailed?

Completed Form 541-A should be mailed to the Franchise Tax Board at the following address: PO Box 942840, Sacramento, CA 94240-0000. It is important to ensure that the form is sent to the correct address to avoid any processing delays.

What happens if the trust's income is $25,000 or less?

If the trust's total income is $25,000 or less, the trustee can skip several lines in the income section of the form and simply report the total income on line 9. This simplifies the reporting process for smaller trusts, allowing for a more straightforward filing experience.

Are there any specific instructions for reporting distributions?

Yes, when reporting distributions of income set aside for charitable purposes, trustees must provide detailed descriptions of the purposes for which the funds were used. This includes itemizing the amounts distributed and specifying the charitable organizations or causes that received the funds. Clear descriptions help ensure compliance with tax regulations and provide transparency in the trust's charitable activities.

Incorrect Trustee Information: Many individuals fail to provide accurate names or addresses for the trustee(s). This can lead to delays or complications in processing the form.

Missing Signatures: Some filers neglect to sign the form. A signature is essential for the form to be considered valid and accepted by the Franchise Tax Board.

Failure to Attach Required Schedules: When there are discrepancies between the amounts reported on Form 541-A and federal Form 1041-A, a detailed schedule explaining these differences must be attached. Not doing so can result in rejection of the return.

Incorrect Filing Deadline: Many people overlook the filing deadline of April 16. Failing to file on time can incur penalties and interest charges.

Inaccurate Income Reporting: Errors in reporting total income can occur when individuals miscalculate or misclassify income sources. This can lead to an incorrect tax liability.

The California Form 541-A is an essential document for trustees of charitable trusts. It reports the accumulation of charitable amounts and is often accompanied by other forms and documents that provide additional information or fulfill specific requirements. Below is a list of related documents commonly used alongside the California 541-A form.

These documents collectively ensure that trustees meet their reporting obligations and maintain compliance with both state and federal tax laws. Properly completing and submitting these forms is crucial for the effective management of charitable trusts.

When filling out the California Form 541-A, there are several important practices to keep in mind. Below is a list of things you should and shouldn't do to ensure the process goes smoothly.

This form is used by any trust that claims a charitable deduction under IRC Section 642(c), not just charitable trusts. Split-interest trusts also need to file this form.

A trust is not required to file if the governing instrument mandates that all income be distributed currently for the year.

California allows an automatic six-month extension for filing, which does not require a request form.

While both forms report similar information, California tax law has specific requirements and differences from federal law.

If any amounts differ from federal Form 1041-A, a schedule explaining the differences must be attached.

The form requires details about the grantor or creator of the trust, as well as the trustee's information.

Even if total income is $25,000 or less, specific lines on the balance sheet must still be completed.

Itemization of charitable deductions is required, including the payee’s name and address, to substantiate the claims.

It must be sent to the specific address of the Franchise Tax Board as indicated in the instructions.

Filing does not automatically grant tax-exempt status; trusts must meet specific criteria to qualify for exemptions under California tax law.