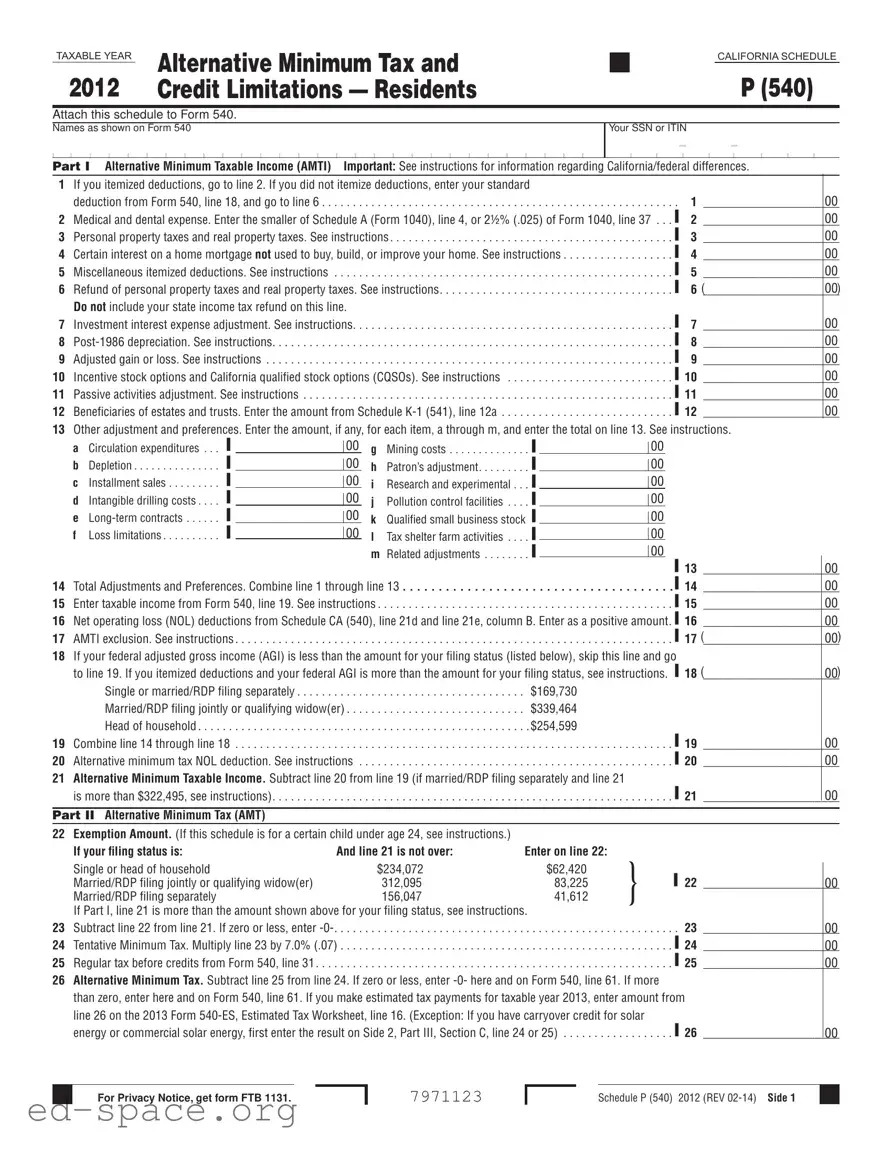

The California 540 Schedule P form is a crucial document for residents who may be subject to the Alternative Minimum Tax (AMT) and need to calculate specific credit limitations. This form must be attached to the California Form 540 when filing state income taxes. It is designed to help taxpayers determine their Alternative Minimum Taxable Income (AMTI) by accounting for various adjustments and preferences. The form includes sections for reporting medical and dental expenses, property taxes, mortgage interest, and other deductions that may influence the AMT calculation. Additionally, it addresses the necessary calculations for determining the tentative minimum tax and the actual alternative minimum tax owed. Taxpayers will also find sections dedicated to credits that can reduce their tax liability, ensuring that they can accurately report any excess tax that may be offset by available credits. Understanding the nuances of the Schedule P form is essential for California residents to ensure compliance and optimize their tax situation.

TAXABLE YEAR |

ALTERNATIVE MINIMUM TAX AND |

|

CALIFORNIA SCHEDULE |

|

|

|

|

2012 |

CREDIT LIMITATIONS — RESIDENTS |

|

P (540) |

ATTACH THIS SCHEDULE TO FORM 540.

NAMES AS SHOWN ON FORM 540

YOUR SSN OR ITIN

- -

PART I Alternative Minimum Taxable Income (AMTI) Important: See instructions for information regarding California/federal differences.

1If you itemized deductions, go to line 2. If you did not itemize deductions, enter your standard

|

deduction from Form 540, line 18, and go to line 6 |

.▌ |

1 |

|

2 |

Medical and dental expense. Enter the smaller of Schedule A (Form 1040), line 4, or 2½% (.025) of Form 1040, line 37 . . . |

2 |

|

|

3 |

Personal property taxes and real property taxes. See instructions |

▌ |

3 |

|

4 |

Certain interest on a home mortgage not used to buy, build, or improve your home. See instructions |

▌ |

4 |

|

5 |

Miscellaneous itemized deductions. See instructions |

▌ |

5 |

|

6 |

Refund of personal property taxes and real property taxes. See instructions |

▌ |

6 |

( |

|

Do not include your state income tax refund on this line. |

▌ |

|

|

7 |

Investment interest expense adjustment. See instructions |

7 |

|

|

8 |

▌ |

8 |

|

|

9 |

Adjusted gain or loss. See instructions |

▌ |

9 |

|

10 |

Incentive stock options and California qualified stock options (CQSOs). See instructions |

▌ 10 |

|

|

11 |

Passive activities adjustment. See instructions |

▌ 11 |

|

|

12 |

Beneficiaries of estates and trusts. Enter the amount from Schedule |

▌ 12 |

|

|

13Other adjustment and preferences. Enter the amount, if any, for each item, a through m, and enter the total on line 13. See instructions.

a |

Circulation expenditures |

▐ |

|

|

00 |

g |

Mining costs |

▐ |

|

|

00 |

|

|

|

|

|

|||||||||

b |

Depletion |

▐ |

|

|

00 |

h |

Patron’s adjustment |

▐ |

|

|

00 |

|

|

|

|

|

|||||||||

c |

Installment sales |

▐ |

|

|

00 |

i |

Research and experimental |

▐ |

|

|

00 |

|

|

|

|

|

|||||||||

d |

Intangible drilling costs . |

▐ |

|

|

00 |

j |

Pollution control facilities . |

▐ |

|

|

00 |

|

|

|

|

|

|||||||||

e |

▐ |

|

|

00 |

k |

Qualified small business stock ▐ |

|

|

00 |

|

||

|

|

|

|

|||||||||

f |

Loss limitations |

▐ |

|

|

00 |

l |

Tax shelter farm activities . |

▐ |

|

|

|

|

|

|

|

|

00 |

|

|||||||

|

|

|

|

|

||||||||

|

|

|

|

|

|

m Related adjustments |

▐ |

|

▐ 13 |

|||

|

|

|

|

|

|

|

|

00 |

||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Total Adjustments and Preferences. Combine line 1 through line 13 |

. . . . . . . . . . . . . . . . |

. . |

. ▌ 14 |

|||||||||

15 Enter taxable income from Form 540, line 19. See instructions . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . |

. ▌ 15 |

||||||||

16Net operating loss (NOL) deductions from Schedule CA (540), line 21d and line 21e, column B. Enter as a positive amount. ▌ 16

17 AMTI exclusion. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▌ 17 (

18If your federal adjusted gross income (AGI) is less than the amount for your filing status (listed below), skip this line and go

to line 19. If you itemized deductions and your federal AGI is more than the amount for your filing status, see instructions. ▌ 18 (

|

Single or married/RDP filing separately |

$169,730 |

|

Married/RDP filing jointly or qualifying widow(er) |

$339,464 |

|

Head of household |

$254,599 |

19 |

Combine line 14 through line 18 |

. . . . . . . . . . . . . . . . . . . . . . . ▌ 19 |

20 |

Alternative minimum tax NOL deduction. See instructions |

. . . . . . . . . . . . . . . . . . . . . . . ▌ 20 |

21Alternative Minimum Taxable Income. Subtract line 20 from line 19 (if married/RDP filing separately and line 21

is more than $322,495, see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

PART II Alternative Minimum Tax (AMT)

22Exemption Amount. (If this schedule is for a certain child under age 24, see instructions.)

|

If your filing status is: |

And line 21 is not over: |

Enter on line 22: |

|

|

|

Single or head of household |

$234,072 |

$62,420 |

} |

▌ 22 |

|

Married/RDP filing jointly or qualifying widow(er) |

312,095 |

83,225 |

||

|

Married/RDP filing separately |

156,047 |

41,612 |

|

|

|

If Part I, line 21 is more than the amount shown above for your filing status, see instructions. |

|

|

||

23 |

Subtract line 22 from line 21. If zero or less, enter |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . |

. . . . . . . |

. 23 |

24 |

Tentative Minimum Tax. Multiply line 23 by 7.0% (.07) |

. . . . . . . . . . . . . . . . . |

. . . . . . . |

▌ 24 |

|

25 |

Regular tax before credits from Form 540, line 31 . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . |

. . . . . . . |

▌ 25 |

26Alternative Minimum Tax. Subtract line 25 from line 24. If zero or less, enter

than zero, enter here and on Form 540, line 61. If you make estimated tax payments for taxable year 2013, enter amount from line 26 on the 2013 Form

energy or commercial solar energy, first enter the result on Side 2, Part III, Section C, line 24 or 25) . . . . . . . . . . . . . . . . . . ▌ 26

00

00

00

00

00

00)

00

00

00

00

00

00

00

00

00

00

00)

00)

00

00

00

00

00

00

00

00

For Privacy Notice, get form FTB 1131.

7971123

Schedule P (540) 2012 (REV

PART III Credits that Reduce Tax Note: Be sure to attach your credit forms to Form 540.

1 |

Enter the amount from Form 540, line 35 |

|

|

|

1 |

|

|

00 |

. . . . |

. . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

2 |

Enter the tentative minimum tax from Side 1, Part II, line 24 |

. . . . |

. . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

2. |

|

|

00 |

|

|

|

|

|||||

|

|

|

(a) |

(b) |

(c) |

(d) |

||

|

|

|

Credit |

Credit used |

Tax balance that |

Credit |

||

SECTION A – Credits that reduce excess tax. |

|

amount |

this year |

may be offset |

carryover |

|||

|

|

|

by credits |

|

|

|

||

3 |

Subtract line 2 from line 1. If zero or less enter |

|

|

|

|

|

|

|

|

This is your excess tax which may be offset by credits |

3 |

|

|

|

|

|

|

A1 Credits that reduce excess tax and have no carryover provisions. |

|

|

|

|

|

|

|

|

4 |

Code: 162 Prison inmate labor credit (FTB 3507) |

4 |

|

|

|

|

|

|

5 |

Code: 169 Enterprise zone employee credit (FTB 3553) |

5 |

|

|

|

|

|

|

6 |

Code: ____ ____ ____ New Home Credit or First Time Buyer Credit |

6 |

|

|

|

|

|

|

7 |

Code: 232 Child and dependent care expenses credit (FTB 3506) |

7 |

|

|

|

|

|

|

A2 Credits that reduce excess tax and have carryover provisions. See instructions. |

|

|

|

|

▌ |

|||

8 |

Code: ▌____ ____ ____ Credit Name: |

8 |

|

|

|

|||

9 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Code: ▌____ ____ ____ Credit Name: |

9 |

|

|

|

▌ |

||

10 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Code: ▌____ ____ ____ Credit Name: |

10 |

|

|

|

▌ |

||

11 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Code: ▌____ ____ ____ Credit Name: |

11 |

|

|

|

▌ |

||

12 |

Code: 188 Credit for prior year alternative minimum tax |

12 |

▌ |

▌ |

|

▌ |

||

SECTION B – Credits that may reduce tax below tentative minimum tax. |

|

|

|

|

|

|

|

|

13 |

If Part III, line 3 is zero, enter the amount from line 1. If line 3 is more than |

|

|

|

|

|

|

|

|

zero, enter the total of line 2 and the last entry in column (c) |

13 |

|

|

|

|

|

|

B1 Credits that reduce net tax and have no carryover provisions. |

|

|

|

|

|

|

|

|

14 |

Code: 170 Credit for joint custody head of household |

14 |

|

|

|

|

|

|

15 |

Code: 173 Credit for dependent parent |

15 |

|

|

|

|

|

|

16 |

Code: 163 Credit for senior head of household |

16 |

|

|

|

|

|

|

17 |

Nonrefundable renter’s credit |

17 |

|

|

|

|

|

|

B2 Credits that reduce net tax and have carryover provisions. See instructions. |

|

|

|

|

▌ |

|||

18 |

Code: ▌____ ____ ____ Credit Name: |

18 |

|

|

|

|||

19 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Code: ▌____ ____ ____ Credit Name: |

19 |

|

|

|

▌ |

||

20 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Code: ▌____ ____ ____ Credit Name: |

20 |

|

|

|

▌ |

||

21 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Code: ▌____ ____ ____ Credit Name: |

21 |

|

|

|

▌ |

||

B3 Other state tax credit. |

|

|

|

|

|

|

|

|

22 |

Code: 187 Other state tax credit |

22 |

|

|

|

|

|

|

SECTION C – Credits that may reduce alternative minimum tax. |

|

|

|

|

|

|

|

|

23 |

Enter your alternative minimum tax from Side 1, Part II, line 26 |

23 |

|

|

|

|

|

|

24 |

Code: 180 Solar energy credit carryover from Section B2, column (d) |

24 |

|

|

|

▌ |

||

25 |

Code: 181 Commercial solar energy credit carryover from Section B2, column (d) . . |

25 |

|

|

|

▌ |

||

26 |

Adjusted AMT. Enter the balance from line 25, column (c) here |

|

|

|

|

|

|

|

|

and on Form 540, line 61 |

26 |

|

|

|

|

|

|

Side 2 Schedule P (540) 2012

7972123

| Fact Name | Fact Description |

|---|---|

| Purpose | The California 540 Schedule P form is used to calculate Alternative Minimum Tax (AMT) for residents. |

| Filing Requirement | Schedule P must be attached to Form 540 when filing your state income tax return. |

| Taxable Year | The form is specific to the taxable year, and the 2012 version is for the tax year ending December 31, 2012. |

| Alternative Minimum Taxable Income (AMTI) | AMTI is calculated using a series of adjustments and preferences outlined in the form. |

| Exemption Amounts | Exemption amounts vary by filing status, with specific thresholds for single, married, and head of household filers. |

| Governing Laws | The form is governed by California Revenue and Taxation Code sections related to income taxation. |

| Credits | Schedule P includes sections for credits that can reduce tax liability, such as the solar energy credit. |

| Instructions | Taxpayers must refer to the instructions for guidance on completing each line item accurately. |

| Important Note | It is crucial to report any adjustments and preferences correctly to avoid discrepancies with the tax authority. |

Completing the California 540 Schedule P form involves several steps to ensure accurate reporting of your Alternative Minimum Taxable Income and related credits. After gathering all necessary information, you can begin filling out the form. It is crucial to follow each step carefully to avoid any errors that could affect your tax obligations.

What is the California 540 Schedule P form?

The California 540 Schedule P form is used by residents of California to calculate their Alternative Minimum Tax (AMT) and to report certain credits that may reduce their tax liability. This form is attached to the California Form 540, which is the standard income tax return for residents. It helps ensure that individuals pay a minimum amount of tax, regardless of deductions and credits they may qualify for.

Who needs to file the Schedule P?

How do I determine my Alternative Minimum Taxable Income (AMTI)?

What are some common adjustments that affect AMTI?

What is the purpose of the AMT exemption amount?

How is the tentative minimum tax calculated?

What should I do if I have credits that may reduce my tax liability?

Where can I find additional information or assistance with the Schedule P?

Incorrectly entering personal information. Ensure that your name and Social Security Number (SSN) match exactly with what is on your Form 540.

Failing to attach the Schedule P to Form 540. Always remember to attach this schedule; otherwise, your return may be incomplete.

Not following the instructions for itemized deductions. If you itemized deductions, you must go to line 2; otherwise, enter your standard deduction and proceed to line 6.

Leaving out necessary adjustments. Review lines 1 through 13 carefully to ensure all adjustments and preferences are included.

Ignoring the federal and California differences. Pay attention to the instructions regarding AMTI, as there may be discrepancies between federal and state calculations.

Miscalculating the Alternative Minimum Taxable Income (AMTI). Ensure that you subtract the correct amounts from your taxable income to arrive at the AMTI.

Overlooking the exemption amounts. Be aware of the exemption amounts for your filing status, as this will impact your tax calculations.

Failing to report carryover credits correctly. If you have credits that may carry over, ensure you enter them accurately in the appropriate sections.

Not double-checking for zero balances. If any line indicates a zero balance, ensure you enter -0- where required to avoid confusion.

Skipping the review of all lines. Before submitting, review every line of the form to catch any potential errors or omissions.

The California 540 Schedule P form is essential for residents who need to calculate their Alternative Minimum Tax (AMT) and credit limitations. However, this form is often accompanied by several other documents that provide additional information and context for taxpayers. Below is a list of related forms and documents that you may need to consider when filing your taxes.

Understanding these forms and their purposes can help ensure a smooth tax filing process. Make sure to gather all necessary documentation to support your claims and calculations when completing your California tax forms.

The California 540 Schedule P form shares similarities with several other tax-related documents. Here’s a list of eight documents that are comparable:

When filling out the California 540 Schedule P form, it's important to be mindful of certain best practices and common pitfalls. Here’s a list to help you navigate the process effectively.

Here are some common misconceptions about the California 540 Schedule P form:

This is not true. While the form does apply to those who may have to pay Alternative Minimum Tax (AMT), it can affect various income levels. Anyone with specific deductions or credits may need to file it.

Many people think they can skip the form if they don't owe AMT. However, you must complete it to determine if you qualify for certain credits or deductions, even if you end up with no AMT liability.

While both forms address alternative minimum tax, they are not identical. California has its own rules and adjustments that differ from federal guidelines, so it’s essential to follow the state-specific instructions.

This is incorrect. You can still claim certain deductions on your California tax return. Schedule P helps calculate how these deductions affect your AMT liability.

Many find the form daunting, but it is designed to be straightforward. With clear instructions, most taxpayers can complete it without needing professional help.

Even if you qualify for credits, you may still need to file Schedule P. It helps determine how these credits impact your overall tax situation, ensuring you maximize your benefits.

The California 540 Schedule P form is essential for calculating your Alternative Minimum Tax (AMT) liability. It must be attached to your Form 540 when filing.

Start by determining your Alternative Minimum Taxable Income (AMTI). This involves adjusting your taxable income by adding or subtracting various adjustments and preferences listed on the form.

Be aware of the income thresholds based on your filing status. If your federal adjusted gross income (AGI) exceeds certain limits, specific deductions may not apply, which can affect your AMTI calculation.

Carefully review the instructions for each line item. Some entries require specific calculations or references to other forms, such as Schedule A or Form 1040.

When calculating your AMT, remember to include any applicable credits that can reduce your tax liability. Ensure you attach all necessary credit forms to your primary tax return.

Finally, if you are uncertain about any part of the process, consider seeking assistance from a tax professional. They can provide clarity and ensure that you comply with all regulations while maximizing your potential deductions.