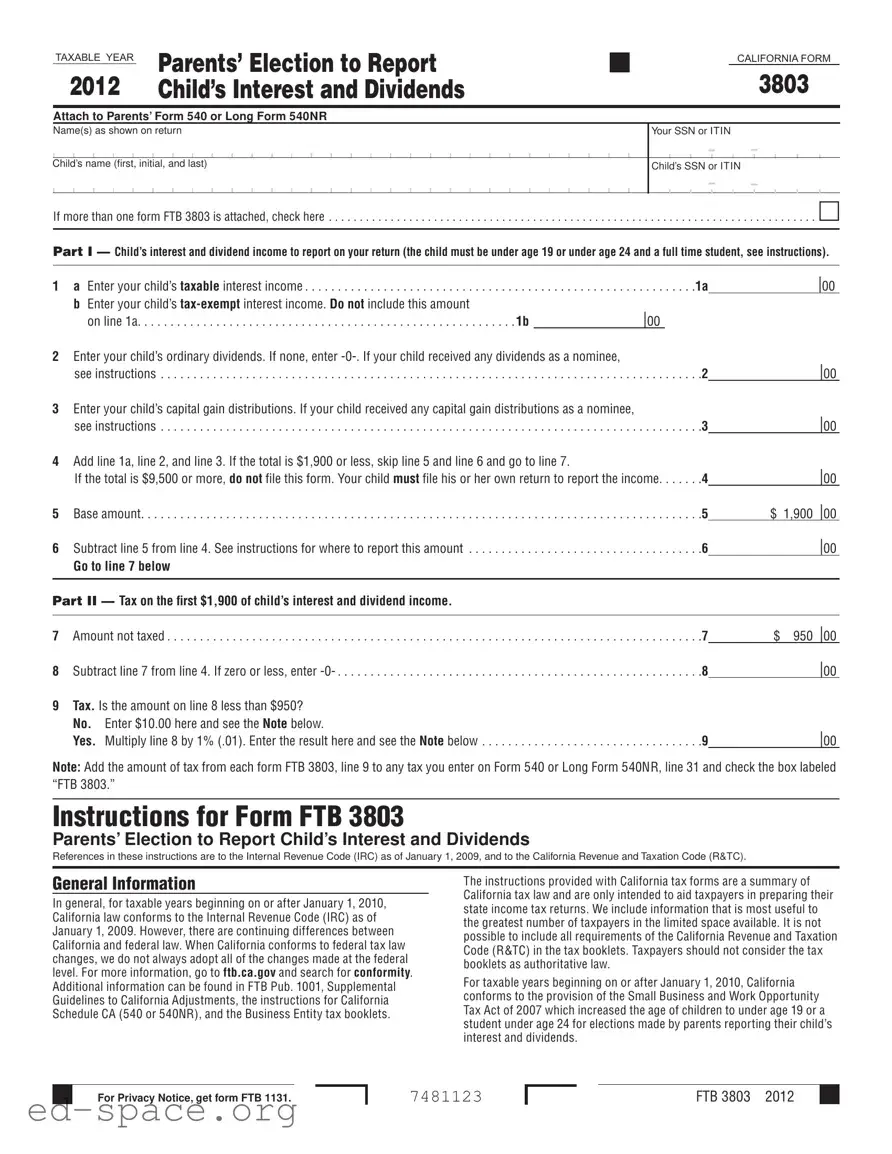

The California Form 3803, known as the Parents’ Election to Report Child’s Interest and Dividends, is an essential tool for parents managing their child's income from investments. This form allows parents to report their child's interest and dividend income on their own California income tax return, thereby sparing the child from the necessity of filing a separate return. To qualify for this election, the child must be under 19 years old or under 24 and a full-time student, with specific income limitations. The form requires detailed reporting of the child’s taxable interest, tax-exempt interest, ordinary dividends, and capital gain distributions. If the total income reported is $1,900 or less, the parents can bypass additional tax calculations. However, if the income exceeds $9,500, the child must file their own return. Parents must also meet certain criteria, including filing a joint return or being the custodial parent, to elect this option. Completing Form 3803 accurately and timely is crucial for compliance and to optimize tax benefits for both the parent and child.

TAXABLE YEAR |

Parents’ Election to Report |

|

|

CALIFORNIA FORM |

|

|

|

|

|

2012 |

Child’s Interest and Dividends |

3803 |

||

|

|

|

|

|

Attach to Parents’ Form 540 or Long Form 540NR

Name(s) as shown on return

Child’s name (first, initial, and last)

Your SSN or ITIN

Child’s SSN or ITIN

- -

If more than one form FTB 3803 is attached, check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Part I — Child’s interest and dividend income to report on your return (the child must be under age 19 or under age 24 and a full time student, see instructions).

1 a Enter your child’s taxable interest income |

1a |

|00 |

bEnter your child’s

on line 1a |

1b |

|00 |

2Enter your child’s ordinary dividends. If none, enter

see instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

3Enter your child’s capital gain distributions. If your child received any capital gain distributions as a nominee,

see instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

4Add line 1a, line 2, and line 3. If the total is $1,900 or less, skip line 5 and line 6 and go to line 7.

If the total is $9,500 or more, do not file this form. Your child must file his or her own return to report the income. . . . . . .4

5 Base amount. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

6 Subtract line 5 from line 4. See instructions for where to report this amount . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Go to line 7 below

|00

|00

|00

$1,900 |00 |00

Part II — Tax on the first $1,900 of child’s interest and dividend income.

7 |

Amount not taxed |

7 |

$ 950 |00 |

|

8 |

Subtract line 7 from line 4. If zero or less, enter |

8 |

|00 |

|

9 |

Tax. Is the amount on line 8 less than $950? |

|

|

|

|

No. |

Enter $10.00 here and see the Note below. |

|

|00 |

|

Yes. |

Multiply line 8 by 1% (.01). Enter the result here and see the Note below |

9 |

|

Note: Add the amount of tax from each form FTB 3803, line 9 to any tax you enter on Form 540 or Long Form 540NR, line 31 and check the box labeled “FTB 3803.”

Instructions for Form FTB 3803

Parents’ Election to Report Child’s Interest and Dividends

References in these instructions are to the Internal Revenue Code (IRC) as of January 1, 2009, and to the California Revenue and Taxation Code (R&TC).

General Information

In general, for taxable years beginning on or after January 1, 2010, California law conforms to the Internal Revenue Code (IRC) as of January 1, 2009. However, there are continuing differences between California and federal law. When California conforms to federal tax law changes, we do not always adopt all of the changes made at the federal level. For more information, go to ftb.ca.gov and search for conformity. Additional information can be found in FTB Pub. 1001, Supplemental Guidelines to California Adjustments, the instructions for California Schedule CA (540 or 540NR), and the Business Entity tax booklets.

The instructions provided with California tax forms are a summary of California tax law and are only intended to aid taxpayers in preparing their state income tax returns. We include information that is most useful to the greatest number of taxpayers in the limited space available. It is not possible to include all requirements of the California Revenue and Taxation Code (R&TC) in the tax booklets. Taxpayers should not consider the tax booklets as authoritative law.

For taxable years beginning on or after January 1, 2010, California conforms to the provision of the Small Business and Work Opportunity Tax Act of 2007 which increased the age of children to under age 19 or a student under age 24 for elections made by parents reporting their child’s interest and dividends.

For Privacy Notice, get form FTB 1131.

7481123

FTB 3803 2012

Registered Domestic Partners (RDP)

For purposes of California income tax, references to a spouse, husband, or wife also refer to a California RDP, unless otherwise specified.

When we use the initials RDP they refer to both a California registered domestic “partner” and a California registered domestic “partnership,” as applicable. For more information on RDPs, get FTB Pub. 737, Tax Information for Registered Domestic Partners.

A Purpose

Parents may elect to report their child’s income on their California income tax return by completing form FTB 3803, Parents’ Election to Report Child’s Interest and Dividends. If you make this election, the child will not have to file a return. You may report your child’s income on your California income tax return even if you do not do so on your federal income tax return. You may make this election if your child meets all of the following conditions:

•Was under age 19 or a student under age 24 at the end of 2012. A child born on January 1, 1994, is considered to be age 19 at the end of 2012. A child born on January 1, 1989, is considered to be age 24 at the end of 2012.

•Is required to file a 2012 income tax return.

•Had income only from interest and dividends.

•Had gross income for 2012 that was less than $9,500.

•Made no estimated tax payments for 2012.

•Did not have any overpayment of tax shown on his or her 2011 return applied to the 2012 estimated taxes.

•Had no state income tax withheld from his or her income (backup withholding).

As a parent, you must also qualify as explained in Section B.

B Parents Who Qualify to Make the Election

You qualify to make this election if you file Form 540, California Resident Income Tax Return, or Long Form 540NR, California Nonresident or Part- Year Resident Income Tax Return, and if any of the following applies to you:

•You and the child’s other parent were married to each other or in a registered domestic partnership and you file a joint return for 2012.

•You and the child’s other parent were married to each other or in a registered domestic partnership but you file separate returns for 2012 AND you had the higher taxable income. If you do not know if you had the higher taxable income, get federal Publication 929, Tax Rules for Children and Dependents.

•You were unmarried, treated as unmarried for state income tax purposes, or separated from the child’s other parent by a divorce, separate maintenance decree, or termination of a domestic partnership and you had custody of your child for most of the year (you were the custodial parent). If you were the custodial parent and you remarried or entered into another registered domestic partnership, you may make the election on a joint return with your new spouse/RDP (your child’s stepparent). But if you and your new spouse/RDP do not file a joint return, you qualify to make the election only if you had higher taxable income than your new spouse/RDP.

If you and the child’s other parent were not married or in a registered domestic partnership but you lived together during the year with the child, you qualify to make the election only if you are the parent with the higher taxable income.

If you elect to report your child’s income on your return, you may not reduce that income by any deductions that your child would be entitled to claim on his or her own return, such as the penalty on early withdrawal of child’s savings or any itemized deductions. For more information, get the instructions for federal Form 8814, Parents’ Election to Report Child’s Interest and Dividends.

C How to Make the Election

To make the election, complete and attach form FTB 3803 to your Form 540 or Long Form 540NR and file your return by the due date (including extensions).

File a separate form FTB 3803 for each child whose income you choose to report.

Specific Line Instructions

Use Part I to figure the amount of the child’s income to report on your return. Use Part II to figure any additional tax that must be added to your tax.

Name and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). Enter your name as shown on your tax return. If filing a joint return, include your spouse’s/RDP’s name but enter the SSN or ITIN of the person whose name is shown first on the return.

For more information about interest, dividends, and capital gain distributions taxable by California, get the instructions for Schedule CA (540), California Adjustments — Residents, or Schedule CA (540NR), California Adjustments — Nonresidents or

Part I Child’s Interest and Dividend Income to Report on Your Return

Line 1a

Enter all interest income taxable by California and received by your child in 2012. If, as a nominee, your child received interest that actually belongs to another person, write the amount and the initials “ND” (for “nominee distribution”) on the dotted line to the left of line 1a. Do not include amounts received by your child as a nominee in the total entered on line 1a.

If your child received Form

Line 1b

If your child received any interest income exempt from California tax, such as interest on United States savings bonds or California municipal bonds, enter the total

Line 2

Enter ordinary dividends received by your child in 2012. Ordinary dividends should be shown on Form

If your child received, as a nominee, ordinary dividends that actually belong to another person, enter the amount and the initials “ND” on the dotted line to the left of line 2. Do not include amounts received as a nominee in the total for line 2.

Line 3

Enter the capital gain distributions taxable by California and received by your child in 2012. Capital gain distributions should be shown on Form

Line 6

If the total amount on line 6 of all form(s) FTB 3803 is less than the total amount on line 6 of all your federal Form(s) 8814, enter the difference on Schedule CA (540 or 540NR), line 21f, column B and write “FTB 3803” on line 21f.

If the total amount on line 6 of all form(s) FTB 3803 is more than the total amount on line 6 of all your federal Form(s) 8814, enter the difference on Schedule CA (540 or 540NR), line 21f, column C and write “FTB 3803” on line 21f.

If you did not file federal Form 8814, enter the amount from form

FTB 3803, line 6, on Schedule CA (540 or 540NR), line 21f, column C and write “FTB 3803” on line 21f.

If your child received capital gain distributions (shown on Form

Part II Tax on the First $1,900 of Child’s Interest and Dividend Income

Line 9

Add the amount of tax from each form FTB 3803, line 9 to any tax you enter on Form 540 or Long Form 540NR, line 31 and check the box labeled “FTB 3803.”

Page 2 FTB 3803 2012

| Fact Name | Details |

|---|---|

| Purpose | The California Form 3803 allows parents to report their child's interest and dividends on their tax return. |

| Eligibility | To qualify, the child must be under age 19 or a full-time student under age 24. |

| Income Limits | The child's gross income must be less than $9,500 for the year. |

| Tax Reporting | Parents can report their child's income even if it differs from their federal return. |

| Filing Requirement | If the child's income exceeds $1,900, the child must file their own tax return. |

| Form Attachment | Form 3803 must be attached to either Form 540 or Long Form 540NR. |

| Tax Calculation | The first $1,900 of the child's income is not taxed. Any amount over this is taxed at 1%. |

| Governing Law | California Revenue and Taxation Code governs the use of Form 3803. |

| Privacy Notice | For privacy concerns, refer to Form FTB 1131. |

Completing the California Form 3803 is an essential step for parents wishing to report their child's interest and dividend income on their tax return. The process requires careful attention to detail to ensure accurate reporting. Below are the steps to guide you through filling out the form.

What is the purpose of California Form 3803?

California Form 3803, also known as the Parents’ Election to Report Child’s Interest and Dividends, allows parents to report their child's interest and dividend income on their own tax return. This can simplify the tax process for families, as it means that the child does not need to file a separate tax return if certain conditions are met. The form is particularly useful for children under age 19 or under age 24 who are full-time students, and whose income is solely from interest and dividends.

Who qualifies to use Form 3803?

To qualify for using Form 3803, parents must file either Form 540 or Long Form 540NR. Additionally, the child must be under age 19 or a full-time student under age 24 at the end of the tax year. The child should have gross income less than $9,500 and must not have made any estimated tax payments or had state income tax withheld. Parents must also meet specific criteria, such as being the custodial parent or having higher taxable income if filing separately.

What income can be reported on Form 3803?

Form 3803 is designed to report a child’s interest and dividend income. This includes taxable interest income, tax-exempt interest income, ordinary dividends, and capital gain distributions. However, if the total income exceeds $9,500, the child must file their own return. It's essential to ensure that only the relevant income is reported to avoid complications.

How do I complete Form 3803?

To complete Form 3803, parents should first gather all necessary information about the child’s interest and dividend income. The form consists of two parts: Part I is for reporting the child’s income, while Part II calculates any additional tax owed. Parents must fill out each line accurately and attach the completed form to their Form 540 or Long Form 540NR when filing their tax return. If reporting for multiple children, a separate Form 3803 must be filled out for each child.

What happens if I don’t file Form 3803?

If Form 3803 is not filed when it is applicable, the child may be required to file their own tax return if their income exceeds the thresholds. This could lead to additional paperwork and potential tax liabilities. Furthermore, failing to report the child’s income correctly could result in penalties or interest on unpaid taxes. It's always best to ensure compliance with tax regulations to avoid any issues down the line.

Failing to include the correct Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) for both the parent and child. This can lead to delays or rejections.

Not checking the box if more than one form FTB 3803 is attached. Omitting this step can create confusion for tax authorities.

Incorrectly reporting the child’s income. Parents often mix up taxable and tax-exempt interest, leading to inaccurate totals.

Forgetting to add up the child’s interest and dividend income correctly. This can result in skipped lines or incorrect calculations.

Not understanding the income limits. If the total is $9,500 or more, parents must file a separate return for the child, which many overlook.

Ignoring the specific instructions for nominees. If the child received income as a nominee, it must be clearly indicated, or it will be included incorrectly.

Leaving out the necessary forms. Parents sometimes forget to attach the FTB 3803 to their Form 540 or Long Form 540NR, which is crucial for processing.

Misunderstanding the tax calculation on the first $1,900 of income. Parents often miscalculate the tax owed, especially when determining if it’s less than $950.

Not filing on time. Late submissions can result in penalties, so it’s important to be aware of deadlines.

Failing to keep copies of all submitted forms. Parents should always retain copies for their records, in case of future inquiries or audits.

The California 3803 form is used by parents to elect to report their child's interest and dividend income on their own tax return. This can simplify the tax process for families where the child meets specific criteria. In addition to the California 3803 form, there are several other forms and documents that are commonly used in conjunction with it. Below is a brief description of each of these documents.

Each of these documents plays a role in ensuring that parents can accurately report their child's income while complying with both state and federal tax regulations. Understanding these forms and how they interconnect can help streamline the tax filing process for families.

The California Form 3803 is specifically designed for parents who want to report their child's interest and dividend income on their tax return. Here are nine other documents that share similarities with the California 3803 form:

When filling out the California 3803 form, there are several important dos and don'ts to keep in mind. Following these guidelines will help ensure that you complete the form correctly and avoid potential issues.

Here are five common misconceptions about the California 3803 form:

Filling out and using the California Form 3803 is essential for parents wishing to report their child's interest and dividend income on their tax return. Here are key takeaways regarding the process: