The California Form 3800, officially titled "Tax Computation for Certain Children with Investment Income," serves as a crucial tool for parents managing the tax obligations of their children under specific circumstances. Designed for children aged 18 and under, or students under 24, this form is applicable when the child has investment income exceeding $1,900. The form is attached to the child’s Form 540 or Long Form 540NR and helps determine the tax rate based on the parent’s income, particularly when the parent's tax rate is higher than the child's. The form includes sections for reporting the child's net investment income, calculating tentative tax based on the parent's income, and ultimately determining the child's tax liability. It is essential for parents to complete this form accurately to ensure compliance with California tax regulations while optimizing their tax outcomes. Understanding the nuances of Form 3800 can significantly impact the financial responsibilities of families, particularly those with children who have substantial investment earnings.

|

TAXABLE YEAR |

|

Tax Computation for Certain Children |

|

|

|

|

|

|

|

|

|

|

|

|

|

CALIFORNIA FORM |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2011 |

|

|

|

with Investment Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

3800 |

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attach ONLY to the child’s Form 540 or Long Form 540NR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Child’s name as shown on return |

Child’s SSN or ITIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

|

- |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Parent’s name (first, initial, and last). (Caution: See instructions before completing.) |

Parent’s SSN or ITIN |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

|

- |

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

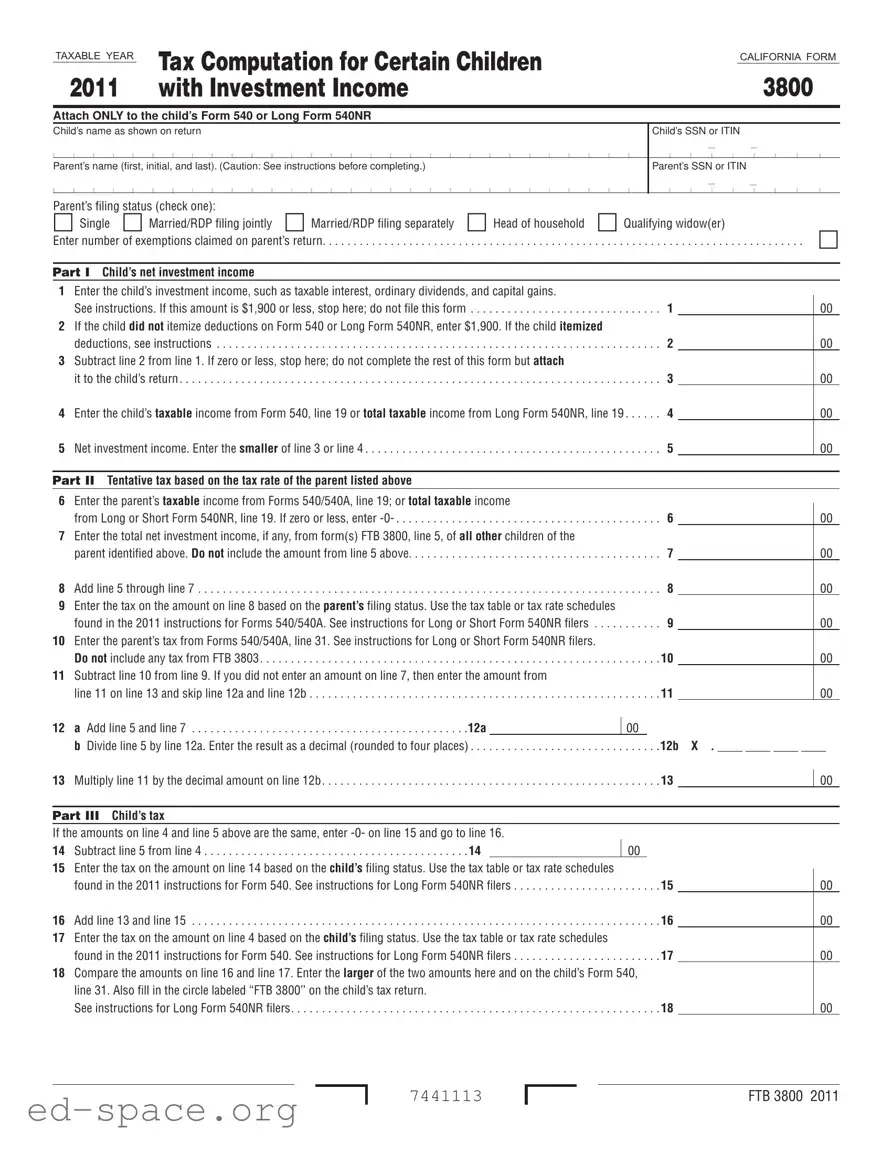

Parent’s filing status (check one):

Single Married/RDP filing jointly Married/RDP filing separately Head of household Qualifying widow(er)

Enter number of exemptions claimed on parent’s return. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Part I Child’s net investment income

1Enter the child’s investment income, such as taxable interest, ordinary dividends, and capital gains.

See instructions. If this amount is $1,900 or less, stop here; do not file this form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2If the child did not itemize deductions on Form 540 or Long Form 540NR, enter $1,900. If the child itemized

deductions, see instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3Subtract line 2 from line 1. If zero or less, stop here; do not complete the rest of this form but attach

it to the child’s return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

00

00

00

4 Enter the child’s taxable income from Form 540, line 19 or total taxable income from Long Form 540NR, line 19 . . . . . . 4

00

5 Net investment income. Enter the smaller of line 3 or line 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

00

Part II Tentative tax based on the tax rate of the parent listed above

6Enter the parent’s taxable income from Forms 540/540A, line 19; or total taxable income

from Long or Short Form 540NR, line 19. If zero or less, enter

7Enter the total net investment income, if any, from form(s) FTB 3800, line 5, of all other children of the

parent identified above. Do not include the amount from line 5 above. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Add line 5 through line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

9Enter the tax on the amount on line 8 based on the parent’s filing status. Use the tax table or tax rate schedules

found in the 2011 instructions for Forms 540/540A. See instructions for Long or Short Form 540NR filers . . . . . . . . . . . 9

10Enter the parent’s tax from Forms 540/540A, line 31. See instructions for Long or Short Form 540NR filers.

Do not include any tax from FTB 3803 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11Subtract line 10 from line 9. If you did not enter an amount on line 7, then enter the amount from

line 11 on line 13 and skip line 12a and line 12b . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

00

00

00

00

00

00

12 a |

Add line 5 and line 7 |

12a |

00 |

b |

Divide line 5 by line 12a. Enter the result as a decimal (rounded to four places) |

. . . . . .12b X . ____ ____ ____ ____ |

|

13 Multiply line 11 by the decimal amount on line 12b . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Part III Child’s tax

If the amounts on line 4 and line 5 above are the same, enter

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14 Subtract line 5 from line 4 |

14 |

|

00 |

15Enter the tax on the amount on line 14 based on the child’s filing status. Use the tax table or tax rate schedules

found in the 2011 instructions for Form 540. See instructions for Long Form 540NR filers . . . . . . . . . . . . . . . . . . . . . . . . 15

16 Add line 13 and line 15 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

17Enter the tax on the amount on line 4 based on the child’s filing status. Use the tax table or tax rate schedules

found in the 2011 instructions for Form 540. See instructions for Long Form 540NR filers . . . . . . . . . . . . . . . . . . . . . . . . 17

18Compare the amounts on line 16 and line 17. Enter the larger of the two amounts here and on the child’s Form 540, line 31. Also fill in the circle labeled “FTB 3800’’ on the child’s tax return.

See instructions for Long Form 540NR filers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

00

00

00

00

00

7441113

FTB 3800 2011

Instructions for Form FTB 3800

Tax Computation for Certain Children with Investment Income

References in these instructions are to the Internal Revenue Code (IRC) as of January 1, 2009, and to the California Revenue and Taxation Code (R&TC).

General Information

For taxable years beginning on or after January 1, 2010, California conforms to the provision of the Small Business and Work Opportunity Act of 2007 which increased the age of children to 18 and under or

a student under age 24 for elections made by parents reporting their child’s interest and dividends.

Registered Domestic Partners (RDP) – For purposes of California income tax, references to a spouse, husband, or wife also refer to a California RDP, unless otherwise specified. When we use the initials RDP they refer to both a California registered domestic “partner” and a California registered domestic “partnership,” as applicable. For more information on RDPs, get FTB Pub. 737, Tax Information for Registered Domestic Partners.

Purpose

For certain children, investment income over $1,900 is taxed at the parent’s rate if the parent’s rate is higher. Use form FTB 3800, Tax Computation for Certain Children with Investment Income, to figure the child’s tax.

Complete form FTB 3800 if all of the following apply:

•The child is 18 and under or a student under age 24 at the end of 2011. A child born on January 1, 1994, is considered to be age 18 at the end of 2011. A child born on January 1, 1988, is considered to be age 24 at the end of 2011.

•The child had investment income taxable by California of more than $1,900.

•At least one of the child’s parents was alive at the end of 2011.

If the child uses form FTB 3800, file Form 540, California Resident Income Tax Return, or Long Form 540NR, California Nonresident or

If the child does not file form FTB 3800, figure the tax in the normal manner on the child’s Forms 540/540A, or Long or Short Form 540NR.

Parents of children 18 and under or a student under age 24 at the end of 2011, may elect to include the child’s investment income on the parent’s tax return. To make this election, the child must have had income only from interest and dividends. The election is not available if estimated tax payments were made in the child’s name. Get form FTB 3803, Parents’ Election to Report Child’s Interest and Dividends, for more information. If parents make this election, the child will not have to file a California tax return or form FTB 3800.

If you elect to report your child’s income on your federal income tax return, but not on your California income tax return, be sure to make an adjustment on your Schedule CA (540 or 540NR), line 21f.

Specific Line Instructions

Parent’s Name and Social Security Number (SSN) or Individual Taxpayer Identiication Number (ITIN)

If federal Form 8615, Tax for Certain Children Who Have Investment Income of More Than $1,900, was filed with the child’s federal tax return, enter the name and SSN or ITIN of the same parent who was identified at the top of federal Form 8615.

If the child’s parents were married to each other or in an RDP and filed a joint 2011 California tax return, enter the name and SSN or ITIN of the parent who is listed first on the joint return.

If the parents were married or in an RDP but filed separate California tax returns, enter the name and SSN or ITIN of the parent with the higher taxable income.

If the parents were unmarried, treated as unmarried for tax purposes, or separated either by a divorce or separate maintenance decree, enter the name and SSN or ITIN of the parent who had custody of the child for most of 2011.

Exception. If the custodial parent remarried or entered into an RDP and filed a joint return with the new spouse/RDP, enter the name and SSN or ITIN of the person listed first on the joint return, even if that person is not the child’s parent. If the custodial parent and the new spouse/RDP filed separate California tax returns, enter the name and SSN or ITIN of the person with the higher taxable income, even if that person is not the child’s parent.

If the child’s parents were unmarried but lived together during the year with the child, enter the name and SSN or ITIN of the parent who had the higher taxable income.

Part I Child’s Net Investment Income

Line 1 – Enter the child’s investment income. Include income such as taxable interest, dividends, capital gains, rents, annuities, and income received as a beneficiary. In most cases, this will be the same as the amount entered on federal Form 8615, include only income taxable by California. Also, include investment income that was not taxed on the child’s federal tax return but is taxable under California law. For more information, get the instructions for Schedule CA (540 or 540NR), line 8 and line 9.

If the child had earned income (defined below), use the following worksheet to figure the amount to enter on form FTB 3800, line 1.

1.Enter the amount of the child’s adjusted gross income from Form 540, line 17 or

Long Form 540NR, line 17, whichever applies . . . . . . 1 __________

2.Enter the child’s earned income . . . . . . . . . . . . . . . . . . 2 __________

(wages, tips, and other payments received for personal services performed)

3.Subtract line 2 from line 1. Enter the result

here and on form FTB 3800, line 1 . . . . . . . . . . . . . . . 3 __________

Line 2 – If the child itemized deductions, enter the greater of:

$950 plus the portion of the amount on Form 540 or Long Form 540NR, line 18, that is directly connected with the production of the investment income shown on form FTB 3800, line 1 or $1,900.

Part II Tentative Tax Based on Parent’s Tax Rate

If the parent used Form 540 2EZ, refigure your tax by referring to the tax table for Forms 540/540A in order to complete this part. Using Form 540 2EZ will not produce the correct result.

Line 6 – Enter the taxable income from Forms 540/540A, line 19; or total taxable income from Long or Short Form 540NR, line 19 of the parent whose name is shown at the top of form FTB 3800. If the parent’s taxable income is less than zero, enter

Line 7 – If the individual identified as the parent on this form FTB 3800 is also identified as the parent on any other form FTB 3800, add the amounts, if any, from line 5 on each of the other forms FTB 3800 and enter the total on line 7.

Line 9 – Use the California tax table or tax rate schedules in the 2011 instructions for Forms 540/540A to find the tax for the amount on line 8, based on the parent’s filing status.

FTB 3800 2011 Page 1

Long or Short Form 540NR Filers: To figure a revised California adjusted gross income and a tentative tax based on the parent’s tax rate, complete the following worksheet.

AEnter the child’s portion of the net investment income that must be included in the child’s

|

CA adjusted gross income |

____________ |

B |

Enter parent’s CA adjusted gross income from |

|

|

Long or Short Form 540NR, Line 32 |

____________ |

C |

Add line A and line B |

____________ |

D |

Enter the child’s investment income |

|

|

(form FTB 3800, line 5) |

____________ |

E |

Enter parent’s adjusted gross income from all |

|

|

sources from Long or Short Form 540NR, line 17. . . |

____________ |

|

If the parents have other children for whom form |

|

|

FTB 3800 was completed, add the other children’s |

|

|

net investment income to the parent’s CA adjusted |

|

|

gross income on line B and to the parent’s adjusted |

|

|

gross income from all sources on line E. |

|

F |

Add line D and line E |

____________ |

G |

Divide line C by line F (not to exceed 1.0) |

____________ |

HEnter the parent’s total itemized deductions or standard deduction from Long or Short

|

Form 540NR, line 18 |

____________ |

I |

Multiply line H by line G |

____________ |

J |

Subtract line I from line C |

____________ |

K |

Subtract line H from line F |

____________ |

LFind the tax on the amount on line K for the parent’s filing status (Use the tax table or tax rate schedules in the 2011 instructions for

|

Long or Short Form 540NR) |

____________ |

M |

Divide line L by line K |

____________ |

N |

Multiply line J by line M. Enter the result on form |

|

|

FTB 3800, line 9 |

____________ |

Line 10 – Enter the tax shown on the tax return of the parent identified at the top of form FTB 3800 from Forms 540/540A, line 31.

If the parent filed a joint tax return, enter on line 10 the tax shown on that tax return even if the parent’s spouse/RDP is not the child’s parent.

Long Form 540NR Filers: If the parent’s tax amount on Long

Form 540NR, line 37 does not include an amount from form FTB 3803, then enter the parent’s tax amount from Long Form 540NR, line 37.

If the parent’s tax amount on Long Form 540NR, line 37 includes an amount from form FTB 3803, revise the parent’s tax by completing the following worksheet.

A |

Enter the tax from the parent’s |

|

|

Long Form 540NR, line 31 |

____________ |

B |

Enter the tax from form FTB 3803 |

____________ |

C |

Subtract line B from line A |

____________ |

D |

Enter the amount from the parent’s |

|

|

Long Form 540NR, line 19 |

____________ |

E |

Divide line C by line D |

____________ |

F |

Enter the amount from the parent’s |

|

|

Long Form 540NR, line 35 |

____________ |

G |

Multiply line F by line E. Enter the result |

|

|

on form FTB 3800, line 10 |

____________ |

Part III Child’s Tax

Line 15 – Use the California tax table or tax rate schedules in the 2011 instructions for Form 540 to find the tax for the amount on line 14 based on the child’s filing status.

Long Form 540NR Filers: To figure a revised California adjusted gross income for the child and the child’s tax, complete the following worksheet.

A Enter the child’s CA adjusted gross income |

|

from Long Form 540NR, line 32 |

____________ |

BEnter the portion of the child’s net investment income that must be included in the child’s

|

CA adjusted gross income |

____________ |

C |

Subtract line B from line A |

____________ |

D |

Enter the child’s adjusted gross income from all |

|

|

sources from Long Form 540NR, line 17 |

____________ |

E |

Enter the child’s investment income |

|

|

(form FTB 3800, line 5) |

____________ |

F |

Subtract line E from line D |

____________ |

G |

Divide line C by line F (not to exceed 1.0) |

____________ |

HEnter the child’s total itemized deductions or standard deduction from Long or Short

|

Form 540NR, line 18 |

____________ |

I |

Multiply line H by line G |

____________ |

J |

Subtract line I from line C |

____________ |

K |

Subtract line H from line F |

____________ |

LFind the tax on the amount on line K for the child’s filing status (Use the tax table or tax rate schedules in the 2011 instructions for

|

Long Form 540NR) |

____________ |

M |

Divide line L by line K |

____________ |

N |

Multiply line J by line M. Enter the result on |

|

|

form FTB 3800, line 15 |

____________ |

Line 17 – Use the California tax table or tax rate schedules found in the 2011 instructions for Form 540 to find the tax for the amount on line 4, based on the child’s filing status.

Long Form 540NR Filers: |

|

A Enter the amount from form FTB 3800, line 4 |

____________ |

BFind the tax for the amount on line A, by using the tax table or tax rate schedules in the 2011 instructions for Long Form 540NR based on

|

the child’s filing status |

____________ |

C |

Divide line B by line A |

____________ |

D |

Enter the amount from the child’s |

|

|

Long Form 540NR, line 35 |

____________ |

E |

Multiply line D by line C. Enter the result on |

|

|

form FTB 3800, line 17 |

____________ |

Line 18 – Compare the amounts on line 16 and line 17 and enter the larger of the two amounts on line 18. Be sure to fill in the circle labeled “FTB 3800” on Form 540, line 31 of the child’s tax return.

Long Form 540NR Filers: Divide the child’s Long Form 540NR, line 35 by the child’s Long Form 540NR, line 19 to determine the child’s percentage. Divide the larger of line 16 or line 17, by the percentage. Enter the amount on line 18 and on the child’s Long Form 540NR, line 31. Be sure to the fill in the circle labeled “FTB 3800” on the child’s Long Form 540NR.

Note: The amount entered on 540NR, line 31 reflects your tax on total taxable income before applying the California tax rate to your California source income. Follow the instructions for Long Form 540NR to determine your final California tax.

Page 2 FTB 3800 2011

| Fact Name | Details |

|---|---|

| Purpose | The California Form 3800 is used to calculate the tax for children with investment income exceeding $1,900, which is taxed at the parent's rate if higher. |

| Eligibility Criteria | To use Form 3800, the child must be 18 or younger, or a student under 24, and have investment income over $1,900. |

| Filing Requirement | This form must be attached to the child’s Form 540 or Long Form 540NR when filing taxes. |

| Investment Income Definition | Investment income includes taxable interest, dividends, and capital gains. Only income taxable by California is reported. |

| Governing Laws | The form operates under the California Revenue and Taxation Code (R&TC) and conforms to the Internal Revenue Code (IRC) as of January 1, 2009. |

| Tax Calculation | The tax is calculated based on the parent’s taxable income and the child’s net investment income, utilizing tax tables provided in the instructions. |

Completing the California Form 3800 is an essential step for parents of children with investment income exceeding $1,900. This form helps determine the tax liability for the child based on the parent's tax rate. After filling out the form, it should be attached to the child's Form 540 or Long Form 540NR when filing. Below are the steps to guide you through the process of filling out the California 3800 form.

Next, proceed to Part I, where you will calculate the child’s net investment income. Follow the instructions carefully to ensure accuracy.

Now, you will move on to Part II, which focuses on calculating the tentative tax based on the parent’s tax rate.

Finally, in Part III, you will determine the child’s tax.

What is the purpose of the California 3800 form?

The California 3800 form is used to calculate the tax for certain children who have investment income exceeding $1,900. If a child meets specific criteria, their investment income may be taxed at the parent's rate, which could be higher than the child's tax rate.

Who needs to file the California 3800 form?

Children aged 18 and under, or students under 24, who have investment income over $1,900 must file this form. Additionally, at least one parent must be alive at the end of the tax year for the form to be applicable.

What types of income should be reported on the form?

Report all taxable investment income, including interest, dividends, capital gains, and other relevant income. Make sure to include only the income that is taxable by California, even if it was not taxed on the federal return.

What should I do if my child's investment income is $1,900 or less?

If the child's investment income is $1,900 or less, you do not need to file the California 3800 form. Simply stop there and do not submit the form with the child’s tax return.

How do I determine the parent’s taxable income for the form?

To find the parent’s taxable income, refer to the parent’s California tax return, specifically Forms 540/540A or Long/Short Form 540NR, and enter the amount from line 19. If the parent's income is zero or less, enter -0- on the form.

What if the child has earned income?

If the child has earned income, you will need to calculate the net investment income by subtracting the earned income from the child’s adjusted gross income. This amount should be reported on line 1 of the California 3800 form.

What happens if the child itemized deductions?

If the child itemized deductions on their tax return, you will need to enter a specific calculation on line 2 of the form. This amount is either $950 plus the portion of the deductions related to the investment income or $1,900, whichever is greater.

How is the tentative tax calculated?

The tentative tax is based on the parent's tax rate. You will enter the parent’s taxable income and any net investment income from other children on the form. The total will help determine the tax amount using the tax tables provided in the instructions.

What do I do with the completed California 3800 form?

Attach the completed California 3800 form to the child’s Form 540 or Long Form 540NR when filing. Ensure that you fill in the circle labeled “FTB 3800” on the child’s tax return to indicate that this form has been used.

Incorrect Parent Information: Many people fail to enter the correct name and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) of the parent. This can lead to delays or rejections.

Missing Child’s Investment Income: Some individuals overlook the requirement to accurately report the child’s investment income. This includes taxable interest, dividends, and capital gains. If the amount is $1,900 or less, the form should not be filed at all.

Errors in Taxable Income: Entering the wrong taxable income from the parent’s tax return is a common mistake. Ensure that the income is taken from the correct line on Forms 540 or 540NR.

Incorrect Filing Status: Selecting the wrong filing status for the parent can lead to incorrect calculations. Be sure to check the appropriate box for single, married, head of household, or qualifying widow(er).

Omitting Other Children’s Income: When multiple children are involved, parents sometimes forget to add the net investment income from other children on the form. This can affect the overall tax calculation.

Not Following Instructions: Ignoring the specific line instructions can lead to errors. Each line has detailed guidance, and it’s important to read these before completing the form.

The California 3800 form is essential for calculating the tax owed for certain children with investment income. However, it is often accompanied by other forms and documents that help clarify and support the tax filing process. Below is a list of these documents, along with a brief description of each.

Each of these documents plays a vital role in ensuring accurate tax reporting and compliance with California tax laws. Properly gathering and submitting these forms alongside the California 3800 can help streamline the tax filing process for families with children who have investment income.

The California Form 3800 is used to calculate the tax for certain children with investment income. It has similarities to several other tax-related documents. Below is a list of ten forms that share similarities with the California Form 3800:

When filling out the California 3800 form, follow these guidelines:

Things to avoid when completing the form:

Misconceptions about the California 3800 Form

This is not entirely true. The form applies to children who are 18 or younger or students under 24. Therefore, some 18-year-olds can still qualify.

If the child's investment income is $1,900 or less, you do not need to file this form. In such cases, simply stop here.

This form can apply to families of various income levels. It specifically addresses how to handle a child's investment income, regardless of the family's overall financial situation.

Parents can choose to report only the child's investment income on their return. If the child has earned income, it is not included in this calculation.

The 3800 form is an attachment to the child's Form 540 or Long Form 540NR. It helps calculate the tax but does not replace the child's tax return.

Adjustments can be made, especially if the child has other sources of income or deductions. It's essential to follow the specific instructions provided for accurate reporting.

The California 3800 form is necessary for children under 19 or students under 24 with investment income exceeding $1,900. If the child qualifies, this form must be attached to their Form 540 or Long Form 540NR.

Parents should carefully enter their information, including their name and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). The correct parent must be identified based on custody and filing status.

Investment income must be reported accurately. This includes taxable interest, dividends, and capital gains. If the child’s investment income is $1,900 or less, the form does not need to be filed.

To determine the child’s tax, compare the calculated amounts on lines 16 and 17 of the form. The larger amount should be reported on the child’s Form 540, along with marking the “FTB 3800” circle.