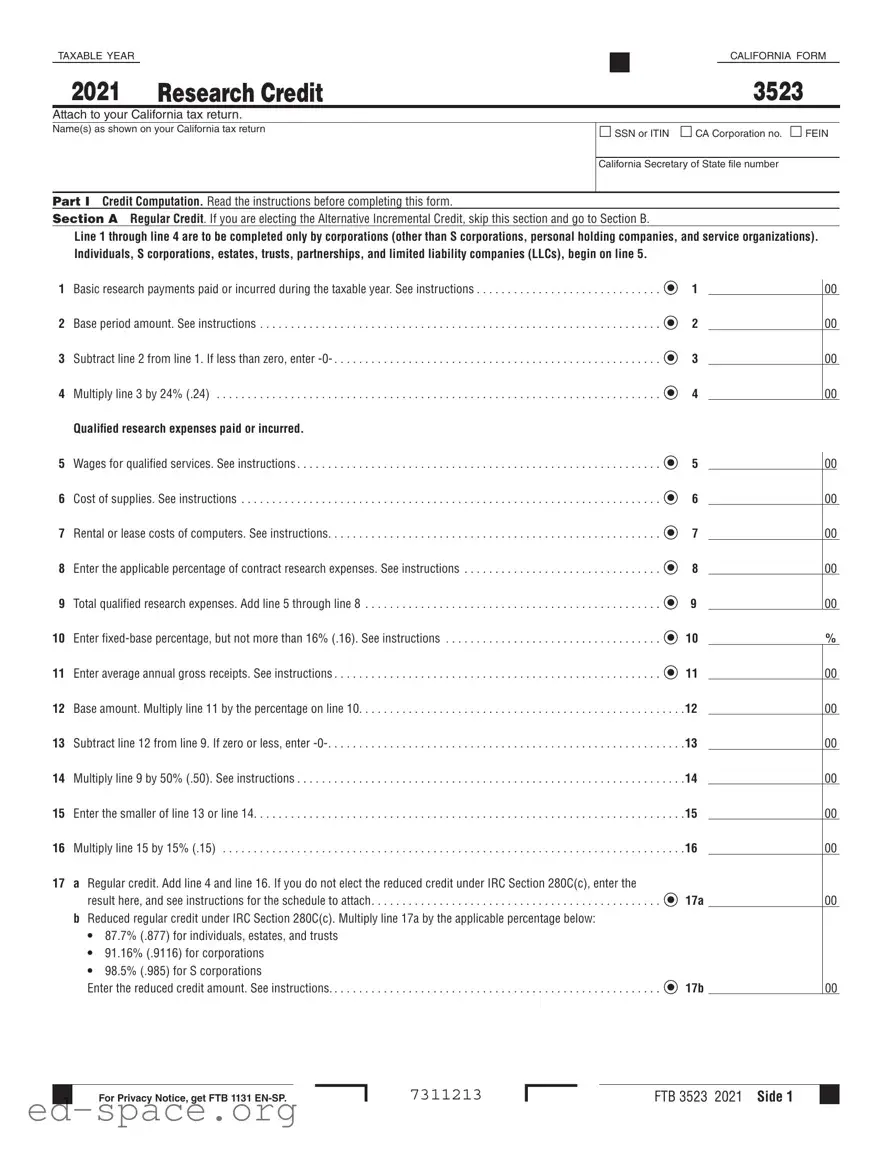

The California Form 3523 serves as a crucial tool for taxpayers seeking to claim the Research Credit on their California tax returns. This form is specifically designed to facilitate the calculation and reporting of both the Regular Credit and the Alternative Incremental Credit for qualified research expenses. Taxpayers must complete different sections based on their business structure, distinguishing between corporations and individuals, S corporations, estates, trusts, partnerships, and limited liability companies (LLCs). The form requires detailed information about basic research payments, qualified research expenses, and the applicable percentages for various calculations. It also addresses the implications of the IRC Section 280C(c) election, which affects the amount of credit that can be claimed. Additionally, taxpayers must account for any carryover credits from previous years, ensuring accurate reporting of their available research credits. By carefully navigating the instructions and sections of Form 3523, taxpayers can maximize their potential benefits under California’s research credit program.

TAXABLE YEAR |

|

|

CALIFORNIA FORM |

|

|

|

|

2021 RESEARCH CREDIT |

3523 |

||

|

|

|

|

Attach to your California tax return.

Name(s) as shown on your California tax return

◻ SSN or ITIN ◻ CA Corporation no. ◻ FEIN

California Secretary of State file number

PART I Credit Computation. Read the instructions before completing this form.

SECTION A Regular Credit. If you are electing the Alternative Incremental Credit, skip this section and go to Section B.

Line 1 through line 4 are to be completed only by corporations (other than S corporations, personal holding companies, and service organizations). Individuals, S corporations, estates, trusts, partnerships, and limited liability companies (LLCs), begin on line 5.

1 |

Basic research payments paid or incurred during the taxable year. See instructions |

1 |

2 |

Base period amount. See instructions |

2 |

3 |

Subtract line 2 from line 1. If less than zero, enter |

3 |

4 |

Multiply line 3 by 24% (.24) |

4 |

|

Qualified research expenses paid or incurred. |

|

5 |

Wages for qualified services. See instructions |

5 |

6 |

Cost of supplies. See instructions |

6 |

7 |

Rental or lease costs of computers. See instructions |

7 |

8 |

Enter the applicable percentage of contract research expenses. See instructions |

8 |

9 |

Total qualified research expenses. Add line 5 through line 8 |

9 |

10 |

Enter |

10 |

11 |

Enter average annual gross receipts. See instructions |

11 |

12 |

Base amount. Multiply line 11 by the percentage on line 10 |

12 |

13 |

Subtract line 12 from line 9. If zero or less, enter |

13 |

14 |

Multiply line 9 by 50% (.50). See instructions |

14 |

15 |

Enter the smaller of line 13 or line 14 |

15 |

16 |

Multiply line 15 by 15% (.15) |

16 |

17a Regular credit. Add line 4 and line 16. If you do not elect the reduced credit under IRC Section 280C(c), enter the

result here, and see instructions for the schedule to attach. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17a

bReduced regular credit under IRC Section 280C(c). Multiply line 17a by the applicable percentage below: 87.7% (.877) for individuals, estates, and trusts

91.16% (.9116) for corporations

98.5% (.985) for S corporations

Enter the reduced credit amount. See instructions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17b

00

00

00

00

00

00

00

00

00

%

00

00

00

00

00

00

00

00

|

For Privacy Notice, get FTB 1131 |

7311213 |

FTB 3523 2021 Side 1 |

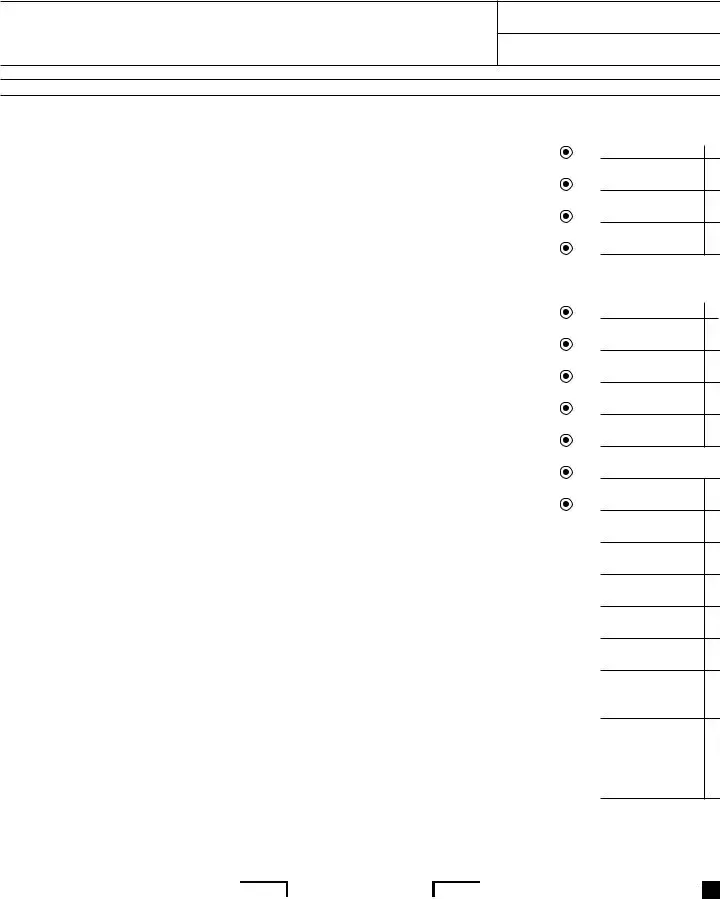

SECTION B Alternative Incremental Credit. Skip this section if you completed Section A, Regular Credit.

Line 18 through line 21 are to be completed only by corporations (other than S corporations, personal holding companies, and service organizations). Individuals, S corporations, estates, trusts, partnerships, and LLCs, begin on line 22.

18 |

Basic research payments paid or incurred during the taxable year. See instructions |

18 |

19 |

Base period amount. See instructions |

19 |

20 |

Subtract line 19 from line 18. If less than zero, enter |

20 |

21 |

Multiply line 20 by 24% (.24) |

21 |

|

Qualified research expenses paid or incurred. |

|

22 Wages for qualified services. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

23 Cost of supplies. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

24 Rental or lease costs of computers. See instructions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

25 Enter the applicable percentage of contract research expenses. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

26 Total qualified research expenses. Add line 22 through line 25 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

27 Enter average annual gross receipts. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 28 Multiply line 27 by 1% (.01). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28 29 Subtract line 28 from line 26. If zero or less, enter

39a Alternative incremental credit. Add line 21, line 36, line 37, and line 38. If you do not elect the reduced credit

under IRC Section 280C(c), enter the result here, and see instructions for the schedule that must be attached . . . . . . . 39a

bReduced alternative incremental credit under IRC Section 280C(c). Multiply line 39a by the applicable percentage below: 87.7% (.877) for individuals, estates, and trusts

91.16% (.9116) for corporations

98.5% (.985) for S corporations

Enter the reduced credit amount. See instructions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39b

SECTION C Available Research Credit

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

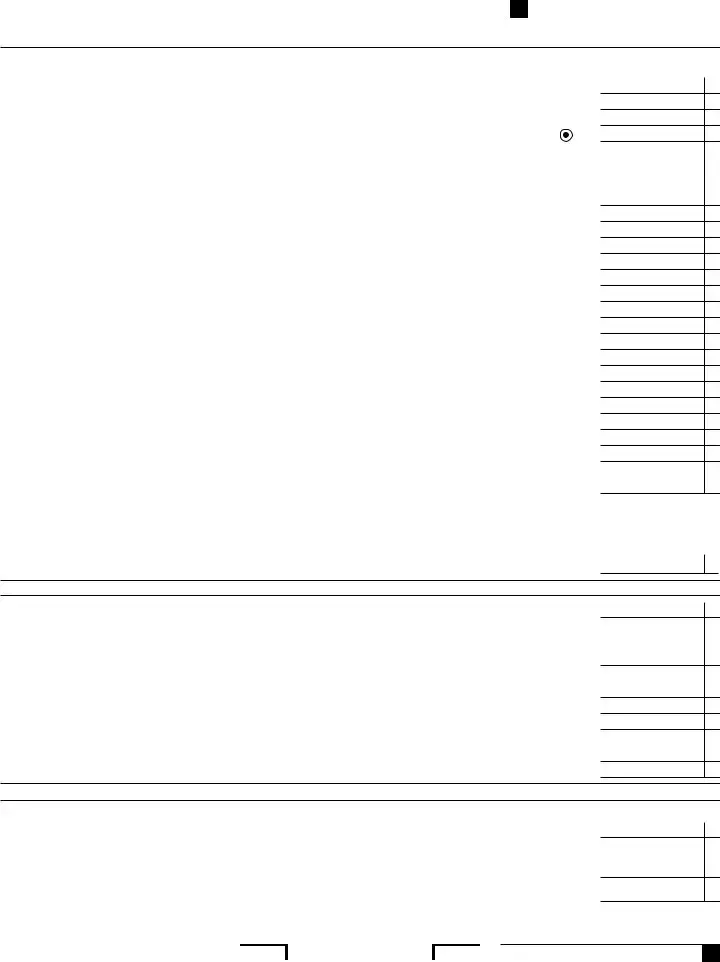

40

41Current year research credit. If you did not elect the reduced credit under IRC Section 280C(c), add line 17a or

line 39a to line 40 and enter the result here. If you elected the reduced credit under IRC Section 280C(c),

add line 17b or line 39b to line 40 and enter the result here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

42Enter the amount of credit on line 41 that is from passive activities. If none of the amount on line 41 is from

passive activities, enter

43 Subtract line 42 from line 41 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43 44 Enter the allowable credit from passive activities. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44

45

See instructions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

46 Total. Add line 43 through line 45. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

PART II Carryover Computation. Combined Report Filers see instructions for Part III before completing this part.

47Credit claimed. Enter the amount of the credit claimed on the current year tax return. See instructions.

(Do not include any assigned credit claimed on form FTB 3544, Part B.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

48Total credit assigned. Enter the total amount from form FTB 3544, Part A, column (g). If you are not a corporation,

enter

49 Credit carryover available for use or assignment for future years. Subtract lines 47 and 48 from line 46 . . . . . . . . . . . . . . 49

00

00

00

00

00

00

00

00

00

00

|

Side 2 FTB 3523 2021 |

7312213 |

PART III Credit Allocation and Carryover Per Entity – Only Combined Report Filers

To make an election for assigning credits, you must also complete form FTB 3544, Part A. Otherwise, the assignment indicated here will be invalid.

Credit Generated and Assigned Per Entity

|

(a) |

(b) |

(c) |

(d) |

(e) |

|

Corporation |

Corporation no., FEIN, or |

Amount of credit generated |

Amount of generated credit |

Total of generated credit |

|

|

SOS no. |

in current year |

carryover from prior years |

and credit carryover from |

|

|

|

|

|

prior years |

|

|

|

|

|

col. (c) + col. (d) |

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

6 |

|

|

|

|

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

(f)* |

(g) |

(h) |

|

Amount of credit from col. (e) claimed |

Amount of research credit |

Generated credit carryover |

|

in current year return. (Do not include |

assigned and to be reported |

for future years |

|

any assigned credit claimed on |

on form FTB 3544, Part A |

col. (e) – [col. (f) + col. (g)] |

|

form FTB 3544, Part B.) |

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

6 |

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

*There is a $5,000,000 business credit limitation on the application of tax credits. See instructions.

|

|

7313213 |

FTB 3523 2021 Side 3 |

| Fact Name | Fact Details |

|---|---|

| Purpose | The California Form 3523 is used to claim the Research Credit for qualified research expenses incurred during the taxable year. |

| Eligibility | Corporations, individuals, S corporations, estates, trusts, partnerships, and LLCs can all file this form, but different sections apply based on the type of entity. |

| Governing Law | The form is governed by California Revenue and Taxation Code Sections 23609 and 23609.5, which outline the requirements for claiming the research credit. |

| Submission | Form 3523 must be attached to your California tax return for the taxable year in which the research expenses were incurred. |

Completing the California 3523 form requires attention to detail and accuracy. Follow these steps carefully to ensure that all necessary information is provided correctly. Once the form is filled out, it should be attached to your California tax return for processing.

What is the purpose of California Form 3523?

California Form 3523 is used to claim the Research Credit for taxable years. This credit is designed to incentivize businesses to engage in qualified research activities within the state. The form allows eligible taxpayers to compute the amount of credit they can claim based on their research expenditures, which may include wages, supplies, and contract research costs. It is essential to attach this form to the California tax return to ensure proper credit is applied.

Who is eligible to file California Form 3523?

Eligibility to file California Form 3523 primarily depends on the type of entity and the nature of the research activities. Corporations, individuals, S corporations, estates, trusts, partnerships, and limited liability companies (LLCs) may qualify, provided they have incurred qualified research expenses during the taxable year. However, certain organizations, such as personal holding companies and service organizations, are excluded from claiming this credit. Each entity type has specific lines on the form that must be completed, depending on their classification.

How is the credit amount calculated on Form 3523?

The credit amount is calculated through two main sections: Regular Credit and Alternative Incremental Credit. For the Regular Credit, taxpayers must determine their basic research payments and subtract the base period amount to arrive at the creditable amount. This amount is then multiplied by 24% to compute the credit. Alternatively, the Alternative Incremental Credit section involves a more complex calculation based on various expense categories and gross receipts. Taxpayers must follow the specific instructions outlined in the form to ensure accurate calculations.

What are the consequences of not filing Form 3523 correctly?

Failure to file Form 3523 correctly can result in the denial of the claimed credit, which may lead to an increased tax liability. Inaccurate information or incomplete forms may trigger audits or requests for additional documentation from the California Franchise Tax Board. It is crucial for taxpayers to carefully review the instructions and ensure that all required information is accurately reported to avoid these potential issues.

Can the Research Credit be carried over to future years?

Yes, the Research Credit can be carried over to future tax years if it is not fully utilized in the year it is claimed. Taxpayers can report any unused credit on subsequent tax returns. The form includes a section for calculating the credit carryover available for future use, which allows businesses to maximize their benefits from research expenditures over time. However, it is important to adhere to the guidelines provided in the form to ensure compliance with tax regulations.

Incomplete Personal Information: Failing to provide all required personal information, such as the full name, Social Security Number (SSN), or Individual Taxpayer Identification Number (ITIN), can lead to delays or rejections. Ensure that all fields are accurately filled out.

Incorrect Section Selection: Many individuals mistakenly fill out the wrong section of the form. For example, corporations should complete Section A, while individuals and certain entities must start at line 5. Carefully read the instructions to determine the correct section for your situation.

Miscalculating Research Expenses: It is crucial to accurately calculate qualified research expenses. Errors in adding wages, costs of supplies, or rental expenses can lead to incorrect credit amounts. Double-check your calculations to ensure accuracy.

Overlooking Instructions: Ignoring the specific instructions provided for each line can result in mistakes. Each line has unique requirements that must be followed closely. Always refer to the instructions to avoid common pitfalls.

Failing to Attach Required Schedules: If you do not elect the reduced credit under IRC Section 280C(c), you must attach the appropriate schedule. Neglecting to do this can result in your claim being incomplete and possibly denied.

Not Keeping Records: Many individuals fail to maintain proper documentation of their research activities and expenses. Keeping detailed records is essential for substantiating your claims. This documentation can be invaluable if your return is audited.

The California Form 3523 is used for claiming the Research Credit on your tax return. Alongside this form, several other documents may be required to ensure accurate reporting and compliance. Here are four commonly used forms that often accompany the California 3523 form:

Each of these forms plays a crucial role in the tax filing process, helping to ensure that all credits and deductions are accurately reported. It is important to carefully complete and attach the necessary documents to avoid any issues with your tax return.

The California Form 3523 is related to various tax credits and financial documentation. Below is a list of seven forms that share similarities with the California 3523 form, along with a brief explanation of how they are alike.

When filling out the California 3523 form, attention to detail is crucial. Here are some important dos and don'ts to keep in mind:

Understanding the California Form 3523 can be challenging, and several misconceptions can lead to confusion. Here are four common misunderstandings:

Filling out the California 3523 form can seem daunting, but understanding its key aspects can simplify the process. Here are five important takeaways to keep in mind:

By following these key points, you can navigate the California 3523 form with greater confidence and accuracy.