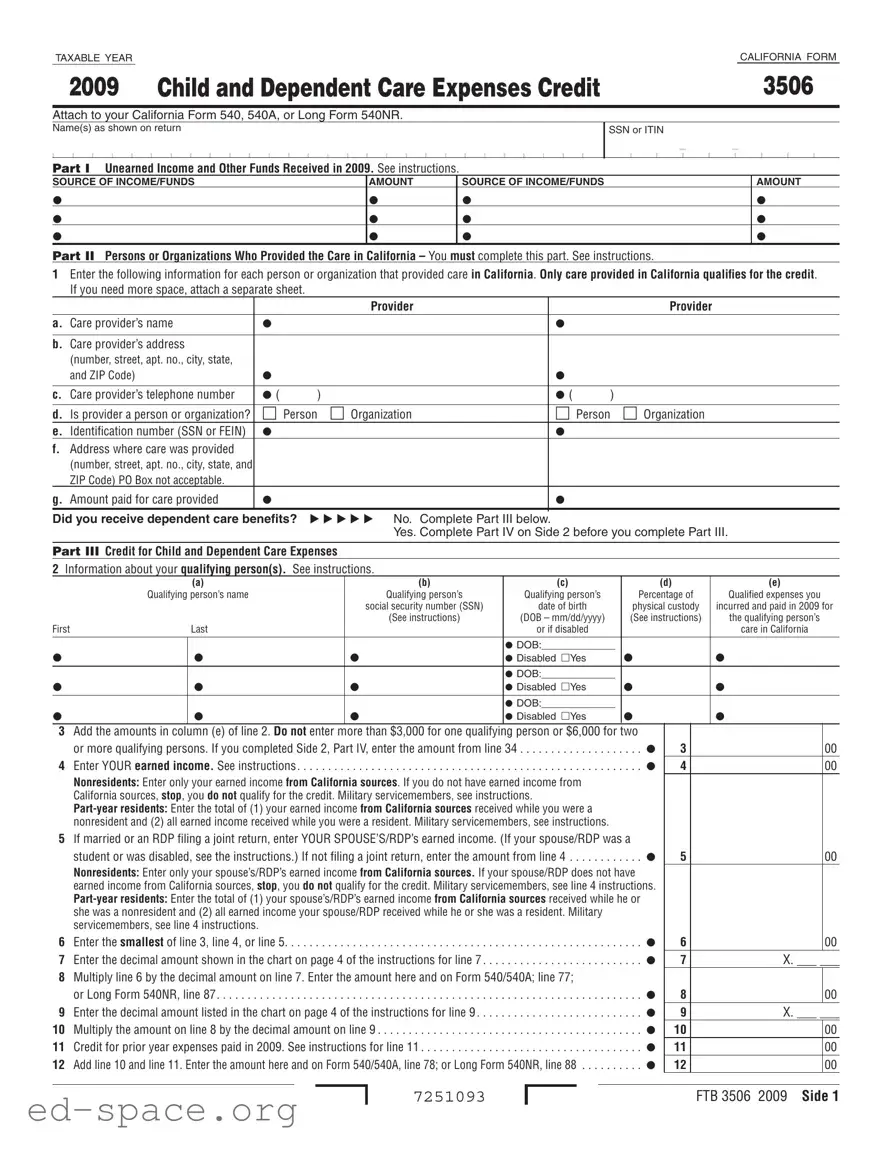

The California 3506 form, also known as the Child and Dependent Care Expenses Credit form, is an important document for taxpayers seeking to claim credits related to child and dependent care expenses. This form is specifically designed for individuals filing their California income tax returns, including Forms 540, 540A, or Long Form 540NR. Key sections of the form require detailed information about unearned income and funds received during the taxable year, as well as the identification of care providers who offered services in California. Taxpayers must provide their care providers' names, addresses, and identification numbers, ensuring that only care provided within the state qualifies for the credit. Additionally, the form includes a section for reporting qualifying individuals and the expenses incurred for their care, with specific limits set on the amounts that can be claimed. For those who received dependent care benefits, the form provides guidance on how to report these amounts, which can affect the overall credit calculation. Understanding the nuances of the California 3506 form is essential for maximizing potential tax benefits while ensuring compliance with state tax regulations.

TAXABLE YEAR |

|

CALIFORNIA FORM |

2009 |

Child and Dependent Care Expenses Credit |

3506 |

Attach to your California Form 540, 540A, or Long Form 540NR.

Name(s) as shown on return

SSN or ITIN

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

- |

|

|

|

|

|

|

|

Part I Unearned Income and Other Funds Received in 2009. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||

SOURCE OF INCOME/FUNDS |

AMOUNT |

|

SOURCE OF INCOME/FUNDS |

|

|

AMOUNT |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Part II Persons or Organizations Who Provided the Care in California – You must complete this part. See instructions.

1Enter the following information for each person or organization that provided care in California. Only care provided in California qualifies for the credit. If you need more space, attach a separate sheet.

|

|

|

Provider |

|

|

Provider |

a. Care provider’s name |

|

|

|

|

|

|

b. Care provider’s address |

|

|

|

|

|

|

|

(number, street, apt. no., city, state, |

|

|

|

|

|

|

and ZIP Code) |

|

|

|

||

c. |

Care provider’s telephone number |

( |

) |

( |

) |

|

d. |

Is provider a person or organization? |

Person Organization |

Person |

Organization |

||

e. |

Identification number (SSN or FEIN) |

|

|

|

|

|

f.Address where care was provided (number, street, apt. no., city, state, and ZIP Code) PO Box not acceptable.

g. Amount paid for care provided |

|

|

Did you receive dependent care benefits? |

No. Complete Part III below. |

|

|

|

Yes. Complete Part IV on Side 2 before you complete Part III. |

Part III Credit for Child and Dependent Care Expenses

2Information about your qualifying person(s). See instructions.

|

|

(a) |

(b) |

(c) |

(d) |

(e) |

|

Qualifying person’s name |

Qualifying person’s |

Qualifying person’s |

Percentage of |

Qualified expenses you |

|

|

|

|

social security number (SSN) |

date of birth |

physical custody |

incurred and paid in 2009 for |

|

|

|

(See instructions) |

(DOB – mm/dd/yyyy) |

(See instructions) |

the qualifying person’s |

First |

|

Last |

|

or if disabled |

|

care in California |

|

|

|

|

|

|

|

|

|

|

|

DOB:_____________ |

|

|

|

Disabled Yes |

|||||

|

|

|

|

DOB:_____________ |

|

|

|

Disabled Yes |

|||||

|

|

|

|

DOB:_____________ |

|

|

|

Disabled Yes |

|||||

3Add the amounts in column (e) of line 2. Do not enter more than $3,000 for one qualifying person or $6,000 for two

or more qualifying persons. If you completed Side 2, Part IV, enter the amount from line 34 . . . . . . . . . . . . . . . . . . . .

4 Enter YOUR earned income. See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Nonresidents: Enter only your earned income from California sources. If you do not have earned income from California sources, stop, you do not qualify for the credit. Military servicemembers, see instructions.

5If married or an RDP filing a joint return, enter YOUR SPOUSE’S/RDP’s earned income. (If your spouse/RDP was a

student or was disabled, see the instructions.) If not filing a joint return, enter the amount from line 4 . . . . . . . . . . . .

Nonresidents: Enter only your spouse’s/RDP’s earned income from California sources. If your spouse/RDP does not have earned income from California sources, stop, you do not qualify for the credit. Military servicemembers, see line 4 instructions.

6 Enter the smallest of line 3, line 4, or line 5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Enter the decimal amount shown in the chart on page 4 of the instructions for line 7 . . . . . . . . . . . . . . . . . . . . . . . . . .

8Multiply line 6 by the decimal amount on line 7. Enter the amount here and on Form 540/540A; line 77;

|

or Long Form 540NR, line 87 |

|

9 |

Enter the decimal amount listed in the chart on page 4 of the instructions for line 9 |

|

10 |

Multiply the amount on line 8 by the decimal amount on line 9 |

|

11 |

Credit for prior year expenses paid in 2009. See instructions for line 11 |

|

12 |

Add line 10 and line 11. Enter the amount here and on Form 540/540A, line 78; or Long Form 540NR, line 88 |

|

3 |

00 |

|

4 |

00 |

|

5 |

00 |

|

6 |

00 |

|

7 |

X. ___ ___ |

|

8 |

|

00 |

9 |

X. ___ ___ |

|

10 |

|

00 |

11 |

|

00 |

12 |

|

00 |

7251093

FTB 3506 2009 Side 1

Part IV Dependent Care Benefits

13Enter the total amount of dependent care benefits you received for 2009. This amount should be shown in box 10 of your Form(s)

|

sole proprietorship or partnership |

13 |

|

00 |

|

14 |

Enter the amount, if any, you carried over from 2008 and used in 2009 during the grace period |

|

14 |

|

00 |

15 |

Enter the amount, if any, you forfeited or carried forward to 2010 |

|

15 |

( |

) 00 |

16 |

Combine line 13 through line 15 |

16 |

|

00 |

|

17Enter the total amount of qualified expenses incurred in 2009 for the

|

care of the qualifying person(s). See instructions |

17 |

00 |

18 |

Enter the smaller of line 16 or line 17 |

18 |

00 |

19 |

Enter YOUR earned income |

19 |

00 |

20If married or an RDP filing a joint return, enter YOUR SPOUSE’S/RDP’s earned income (if your spouse/RDP was a student or was disabled, see the instructions for line 5); if married or an RDP filing a separate return, see the instructions for the

amount to enter; all others, enter the amount from line 19 |

20 |

00 |

21 Enter the smallest of line 18, line 19, or line 20 |

21 |

00 |

22Enter $5,000 ($2,500 if married or an RDP filing separately and you were required

to enter your spouse’s/RDP’s earned income on line 20) |

22 |

00 |

23Enter the amount from line 13 that you received from your sole proprietorship or partnership. If you did not receive

|

|

any amounts, enter |

. . . . . . . . . . . . . . . . . . . . . |

23. |

00 |

||||

24 |

|

Subtract line 23 from line 16 |

24 |

|

00 |

|

|

|

|

25 |

|

Enter the smaller of line 21 or line 22 |

25 |

|

00 |

|

|

|

|

26 |

Deductible benefits. Enter the smallest of line 21, line 22, or line 23 |

. . . . . . . . . . . . . . . . . . . . . |

. |

26 |

|

00 |

|||

27 |

Excluded benefits. Subtract line 26 from line 25. If zero or less, enter |

. . . . . . . . . . . . . . . . . . . . . |

. |

27 |

|

00 |

|||

28 |

Taxable benefits. Subtract line 27 from line 24. If zero or less, enter |

. . . . . . . . . . . . . . . . . . . . . |

. |

28 |

|

00 |

|||

29 |

Enter $3,000 ($6,000 if two or more qualifying persons) |

. . . . . . . . . . . . . . . . . . . . . |

. |

29 |

|

00 |

|||

30 |

Add line 26 and line 27 |

. . . . . . . . . . . . . . . . . . . . . |

30. |

|

00 |

||||

31 |

Subtract the amount on line 30 from the amount on line 29. If zero or less, stop. You do not qualify for the credit. |

|

|

|

|

|

|||

|

|

Exception – If you paid 2008 expenses in 2009, see instructions for line 11 |

. . . . . . . . . . . . . . . . . . . . . |

. |

31 |

|

00 |

||

32 |

Complete Side 1, Part III, line 2. Add the amounts in column (e) and enter the total here |

. |

32 |

|

00 |

||||

33 |

Enter the amount from your federal Form 2441, Part III, line 34 |

. . . . . . . . . . . . . . . . . . . . . |

33. |

|

00 |

||||

34 |

Enter the smaller of line 31, line 32, or line 33. Also, enter this amount on Side 1, Part III, line 3 and |

|

|

|

|

|

|||

|

|

complete line 4 through line 12 |

. . . . . . . . . . . . . . . . . . . . . |

34. |

|

00 |

|||

Worksheet – Credit for 2008 Expenses Paid in 2009 |

|

|

|

|

|

|

|

||

1. |

Enter your 2008 qualified expenses paid in 2008. If you did not claim the credit for these expenses on your 2008 |

|

|

|

|

|

|||

|

|

return, get and complete a 2008 form FTB 3506 for these expenses. You may need to amend your 2008 return |

. . . |

|

. . . . |

. 1.____________________ |

|||

2. |

Enter your 2008 qualified expenses paid in 2009 |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 2.____________________ |

|||

3. |

Add the amounts on line 1 and line 2 |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 3.____________________ |

|||

4. |

Enter $3,000 if care was for one qualifying person ($6,000 for two or more) |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 4.____________________ |

|||

5. |

Enter any dependent care benefits received for 2008 and excluded from your income |

|

|

|

|

|

|

|

|

|

|

(from your 2008 form FTB 3506, Part IV, line 28) |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 5.____________________ |

||

6. |

Subtract amount on line 5 from amount on line 4 and enter the result |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 6.____________________ |

|||

7. |

Compare your and your spouse’s/RDP’s earned income for 2008 and enter the smaller amount |

. . . |

|

. . . . |

. 7.____________________ |

||||

8. |

Compare the amounts on line 3, line 6, and line 7 and enter the smallest amount |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 8.____________________ |

|||

9. |

Enter the amount from your 2008 form FTB 3506, Side 1, Part III, line 6 |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 9.____________________ |

|||

10. |

Subtract amount on line 9 from amount on line 8 and enter the result. If zero or less, stop here. You cannot increase |

|

|

|

|

|

|||

|

|

your credit by any previous year’s expenses |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 10.____________________ |

||

11. |

Enter your 2008 federal adjusted gross income (AGI) (from your 2008 Form 540/540A, line13; |

|

|

|

|

|

|||

|

|

or Long Form 540NR, line 13) |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 11.____________________ |

||

12. |

2008 federal AGI decimal amount (from 2008 form FTB 3506, instructions for line 7) |

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 12.______ . ______ ______ |

||

13. |

Multiply line 10 by line 12 |

. . . . . . . . . . . . . . . . . . . . . |

. . . |

|

. . . . |

. 13.____________________ |

|||

14. |

2008 California AGI decimal amount (from 2008 form FTB 3506, instructions for line 9) |

. . . |

|

. . . . |

. 14.______ . ______ ______ |

||||

15. |

Multiply line 13 by line 14. Enter the result here and on your 2009 form FTB 3506, Side 1, Part III, line 11 |

. . . |

|

. . . . |

. 15.____________________ |

||||

Side 2 FTB 3506 2009

7252093

| Fact Name | Fact Description |

|---|---|

| Purpose | The California Form 3506 is used to claim the Child and Dependent Care Expenses Credit for the taxable year. |

| Eligibility | To qualify for the credit, taxpayers must have incurred eligible expenses for the care of qualifying persons while they worked or looked for work. |

| Attachment Requirement | This form must be attached to California Form 540, 540A, or Long Form 540NR when filing. |

| Income Reporting | Taxpayers must report all unearned income and other funds received during the taxable year on the form. |

| Care Provider Information | Taxpayers must provide detailed information about each care provider, including name, address, and identification number. |

| Maximum Credit | The maximum credit is $3,000 for one qualifying person or $6,000 for two or more qualifying persons. |

| Governing Law | The use of Form 3506 is governed by California Revenue and Taxation Code Section 17052.5. |

Filling out the California 3506 form is an important step in claiming your Child and Dependent Care Expenses Credit. It’s essential to ensure that all sections are completed accurately to avoid any delays in processing your tax return. Follow the steps below to fill out the form correctly.

What is the purpose of the California 3506 form?

The California 3506 form is used to claim the Child and Dependent Care Expenses Credit. This credit helps families offset the costs of care for children or dependents while they work or look for work. By completing this form, taxpayers can potentially reduce their state tax liability, making it easier to manage the financial demands of caregiving. It is essential to attach this form to your California tax return, specifically Form 540, 540A, or Long Form 540NR.

Who qualifies as a care provider for the purposes of this form?

To qualify as a care provider, the individual or organization must provide care in California. The form requires detailed information about each care provider, including their name, address, and whether they are an individual or an organization. Importantly, only care provided in California qualifies for the credit. This means that if you paid for care received outside the state, those expenses cannot be included in your claim.

How do I determine the amount of credit I can claim?

What if I received dependent care benefits?

If you received dependent care benefits, you must report this on the California 3506 form. The form includes a specific section (Part IV) for detailing these benefits. The total amount of benefits received will influence your credit calculation. You will need to consider both the benefits and the qualified expenses incurred in the year to accurately determine your credit. If the benefits exceed your expenses, this could limit the credit you are eligible to claim.

Incorrect Personal Information: One common mistake is failing to accurately enter names or Social Security Numbers (SSNs). Ensure that the names match exactly with the tax return and that SSNs are correct.

Missing Care Provider Information: Many individuals neglect to provide complete details about the care provider. This includes their name, address, and phone number. All care must be provided in California to qualify.

Improper Identification Numbers: Users often forget to include the care provider's identification number, such as their SSN or Federal Employer Identification Number (FEIN). This is essential for verification.

Incorrect Amounts Paid: It's crucial to accurately report the amount paid for care. Some people mistakenly enter the wrong figures, which can affect the credit calculation.

Overlooking Earned Income Requirements: Applicants sometimes fail to report their earned income correctly. If you do not have earned income from California sources, you do not qualify for the credit.

Ignoring Dependent Care Benefits: Some filers forget to include any dependent care benefits received. This amount should be reported from your W-2 forms, and neglecting it can lead to inaccuracies.

Not Following Instructions: The form comes with specific instructions that must be followed. Many users skip reading these instructions, leading to common errors in completing the form.

Failing to Sign and Date the Form: Finally, some individuals forget to sign and date the form before submission. This is a simple yet critical step that can delay processing.

The California Form 3506 is essential for claiming the Child and Dependent Care Expenses Credit. However, it is often accompanied by other forms and documents that help clarify and support your tax situation. Here are five commonly used documents that may be necessary when filing your taxes alongside the California 3506 form.

Understanding these accompanying forms and documents can streamline your tax filing process. Each one plays a vital role in ensuring that you accurately claim the credits you are entitled to, ultimately aiding in a smoother and more efficient tax experience.

When filling out the California Form 3506, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are ten important dos and don’ts:

Understanding the California 3506 form can be challenging. Here are seven common misconceptions about this form, along with clarifications to help you navigate it more easily.

This is not entirely true. While it is primarily designed for residents, part-year residents and nonresidents can also use it if they have earned income from California sources.

Only expenses for care provided in California qualify for the credit. It's essential to ensure that the care provider is located in California.

On the contrary, you must provide details about each care provider, including their name, address, and identification number. This information is crucial for the form's processing.

Your earned income is a determining factor for eligibility. If you do not have earned income from California sources, you cannot qualify for the credit.

The credit is limited to a maximum of $3,000 for one qualifying person and $6,000 for two or more qualifying persons. This means you cannot simply claim all expenses incurred.

While it is most commonly associated with parents, anyone who pays for qualifying dependent care can benefit from this credit, including guardians and caregivers.

This is misleading. If you received dependent care benefits, you must still complete the relevant sections of the form. Your benefits may affect the amount of credit you can claim, but they do not disqualify you from applying.

When filling out the California Form 3506 for Child and Dependent Care Expenses Credit, keep these key takeaways in mind: