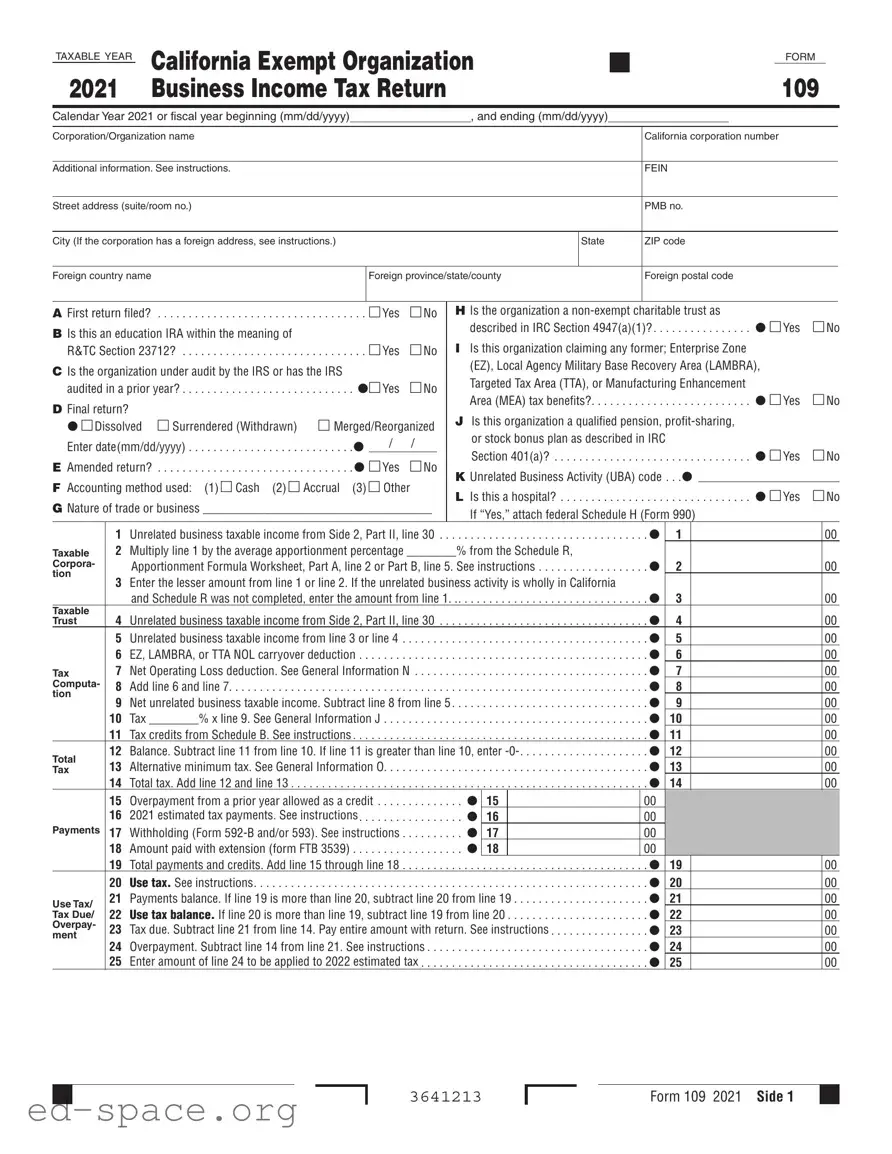

The California 109 form is an essential document for organizations operating within the state that are classified as exempt entities, such as nonprofits or certain types of trusts. This form is used to report business income and tax obligations for a specific taxable year, which can either follow the calendar year or a fiscal year chosen by the organization. Key sections of the form require organizations to provide their name, address, and federal employer identification number (FEIN), ensuring that the state has accurate information on file. Additionally, the form asks whether this is the organization's first return, if it is under IRS audit, or if it is claiming specific tax benefits related to enterprise zones or military base recovery areas. Organizations must detail their unrelated business taxable income, which is the income generated from activities not directly related to their exempt purpose. This includes various income streams such as rental income, advertising, and investment income. Moreover, the form includes sections for deductions and tax credits, allowing organizations to reduce their taxable income. Understanding the California 109 form is crucial for compliance, as it helps ensure that exempt organizations meet their reporting requirements while taking advantage of available tax benefits.

TAXABLE YEAR |

California Exempt Organization |

|

|

|

|

|

|

|

|

|

FORM |

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

109 |

|

|

|

||||||||||||||||||||

2021 |

|

Business Income Tax Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Calendar Year 2021 or fiscal year beginning (mm/dd/yyyy) |

|

|

|

|

|

|

|

, and ending (mm/dd/yyyy) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Corporation/Organization name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

California corporation number |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Additional information. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Street address (suite/room no.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PMB no. |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

City (If the corporation has a foreign address, see instructions.) |

|

|

|

|

|

|

|

|

|

|

State |

|

|

ZIP code |

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

Foreign country name |

|

|

|

Foreign province/state/county |

|

|

Foreign postal code |

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

A First return filed? |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . |

□ Yes |

□ No |

|

H Is the organization a |

|

|

|

|

||||||||||||||||||||

B Is this an education IRA within the meaning of |

|

|

|

|

|

|

|

|

described in IRC Section 4947(a)(1)? . . . . |

. . |

. . . . . . . |

. . . • □ Yes |

□ No |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

R&TC Section 23712? |

. . . . . |

. . . |

□ Yes |

□ No |

|

I Is this organization claiming any former; Enterprise Zone |

|

|

|

|

|||||||||||||||||||||

C Is the organization under audit by the IRS or has the IRS |

|

|

|

|

|

|

(EZ), Local Agency Military Base Recovery Area (LAMBRA), |

|

|

|

|

||||||||||||||||||||

•□ Yes |

|

|

|

Targeted Tax Area (TTA), or Manufacturing Enhancement |

|

|

|

|

|||||||||||||||||||||||

audited in a prior year? |

. . . . . |

|

□ No |

|

|

|

|

|

|||||||||||||||||||||||

D Final return? |

|

|

|

|

|

|

|

|

|

|

Area (MEA) tax benefits? |

. |

. . . |

. . |

. . |

. . . . . . . |

. . . • □ Yes |

□ No |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

• □ Dissolved |

□ Surrendered (Withdrawn) |

□ Merged/Reorganized |

|

J Is this organization a qualified pension, |

|

|

|

|

|||||||||||||||||||||||

Enter date(mm/dd/yyyy) |

|

. |

• |

|

/ |

/ |

|

|

|

or stock bonus plan as described in IRC |

|

|

|

• □ Yes |

|

|

|

|

|||||||||||||

. . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

□ No |

|||||||||||||

E Amended return? |

|

. |

• □ Yes |

□ No |

|

|

. . . . . . . . . . . . . .Section 401(a)? |

. |

. . . |

. . |

. . |

. . . . . . . . . . |

|||||||||||||||||||

. . . . . |

|

|

K Unrelated Business Activity (UBA) code . . |

.• |

|

|

|

|

|||||||||||||||||||||||

F Accounting method used: (1) □ Cash (2) □ Accrual |

(3) □ Other |

|

L Is this a hospital? |

|

|

|

|

|

|

. |

. . . • □ Yes |

□ No |

|||||||||||||||||||

G Nature of trade or business _____________________________________ |

|

. |

. . . |

. . |

. . |

. . . . . . |

|||||||||||||||||||||||||

|

If “Yes,” attach federal Schedule H (Form 990) |

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

1 |

Unrelated business taxable income from Side 2, Part II, line 30 |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

|

1 |

|

|

|

|

|

00 |

|

|||||||||||||

Taxable |

2 |

Multiply line 1 by the average apportionment percentage ________% from the Schedule R, |

|

|

. • |

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Corpora- |

|

Apportionment Formula Worksheet, Part A, line 2 or Part B, line 5. See instructions |

|

2 |

|

|

|

|

|

00 |

|

||||||||||||||||||||

tion |

3 |

Enter the lesser amount from line 1 or line 2. If the unrelated business activity is wholly in California |

|

|

. • |

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

and Schedule R was not completed, enter the amount from line 1 |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

|

3 |

|

|

|

|

|

00 |

|

||||||||||||||

Taxable |

4 |

Unrelated business taxable income from Side 2, Part II, line 30 |

|

|

|

|

|

|

|

|

|

. • |

|

4 |

|

|

|

|

|

00 |

|

||||||||||

Trust |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

|

|

|

|

|

|

|

||||||||||||||||||

|

5 |

Unrelated business taxable income from line 3 or line 4 |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

|

5 |

|

|

|

|

|

00 |

|

||||||||||

|

6 |

EZ, LAMBRA, or TTA NOL carryover deduction . . |

|

. . . . . . . . . . . |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

|

6 |

|

|

|

|

|

00 |

|

||||||||

Tax |

7 |

Net Operating Loss deduction. See General Information N |

. . . . |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

|

7 |

|

|

|

|

|

00 |

|

|||||||||

Computa- |

8 |

Add line 6 and line 7 |

. . . . . . |

. . . |

|

. . . . . . . . . . . |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

|

8 |

|

|

|

|

|

00 |

|

||||||

tion |

9 |

Net unrelated business taxable income. Subtract line 8 from line 5 |

|

|

|

|

|

|

|

|

|

. • |

|

9 |

|

|

|

|

|

00 |

|

||||||||||

|

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

|

|

|

|

|

|

|

|||||||||||||||||

|

10 |

Tax ________% x line 9. See General Information J |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

10 |

|

|

|

|

|

00 |

|

|||||||||||

|

11 |

Tax credits from Schedule B. See instructions |

. . . |

|

. . . . . . . . . . . |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

11 |

|

|

|

|

|

00 |

|

||||||||

Total |

12 |

Balance. Subtract line 11 from line 10. If line 11 is greater than line 10, enter |

. • |

12 |

|

|

|

|

|

00 |

|

||||||||||||||||||||

13 |

Alternative minimum tax. See General Information O |

|

|

|

|

|

|

|

|

|

|

|

|

. • |

13 |

|

|

|

|

|

00 |

|

|||||||||

Tax |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

|

|

|

|

|

|

||||||||||||||||

|

14 |

Total tax. Add line 12 and line 13 . . . . |

. . . . . . |

. . . |

|

. . . . . . . . . . . |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

14 |

|

|

|

|

|

00 |

|

|||||||

|

15 |

. . . . . . . . . .Overpayment from a prior year allowed as a credit |

. . |

. |

. • |

15 |

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

16 |

. .2021 estimated tax payments. See instructions |

|

. . . . . . . . . . . |

. . |

. |

. • |

16 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||

Payments |

17 |

Withholding (Form |

. . |

. |

. • |

17 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

18 |

Amount paid with extension (form FTB 3539) |

. . . |

|

. . . . . . . . . . . |

. . |

. |

. • |

18 |

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

||||||

|

19 |

Total payments and credits. Add line 15 through line 18 |

|

|

|

|

|

|

|

|

|

|

|

|

• |

19 |

|

|

|

|

|

00 |

|

||||||||

|

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

|

|

|

|

|

|||||||||||||||||

|

20 |

USE TAX. See instructions |

. . . . . . |

. . . |

|

. . . . . . . . . . . |

. . |

. |

. . . . |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

20 |

|

|

|

|

|

00 |

|

|||||||

Use Tax/ |

21 |

Payments balance. If line 19 is more than line 20, subtract line 20 from line 19 |

. • |

21 |

|

|

|

|

|

00 |

|

||||||||||||||||||||

22 |

USE TAX BALANCE. If line 20 is more than line 19, subtract line 19 from line 20 |

|

|

. • |

22 |

|

|

|

|

|

00 |

|

|||||||||||||||||||

Tax Due/ |

|

|

|

|

|

|

|||||||||||||||||||||||||

Overpay- |

23 |

Tax due. Subtract line 21 from line 14. Pay entire amount with return. See instructions |

|

|

. • |

23 |

|

|

|

|

|

00 |

|

||||||||||||||||||

ment |

|

|

|

|

|

|

|||||||||||||||||||||||||

24 |

Overpayment. Subtract line 14 from line 21. See instructions |

|

|

|

|

|

|

|

|

|

. • |

24 |

|

|

|

|

|

00 |

|

||||||||||||

|

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

|

|

|

|

|

|

|||||||||||||||||||

|

25 |

. . . . . . . . . .Enter amount of line 24 to be applied to 2022 estimated tax |

. . . . |

. . . . . . . . . . . . |

. . . . . |

. . . |

. . |

|

. • |

25 |

|

|

|

|

|

00 |

|

||||||||||||||

3641213

Form 109 2021 Side 1

|

|

26 |

. . . . . . . . . . . . . . . . . . . . . . .Refund. If line 25 is less than line 24, then subtract line 25 from line 24 |

•. . . |

. . • |

26 |

||||

|

|

|

. . . . . . . . .a Fill in the account information to have the refund directly deposited. Routing number |

26a |

|

|||||

|

|

|

b Type: Checking |

•□ |

Savings |

c Account Number |

• |

|

26c |

|

Refund or |

|

|

|

|

•□ |

|

|

|

||

Amount |

|

27 |

Penalties and interest. See General Information M |

. |

. . • |

27 |

||||

Due |

|

. . |

|

|||||||

|

|

28 |

• □ Check if estimate penalty computed using Exception B or C and attach form FTB 5806 |

. . . |

. . . . |

|

||||

|

|

29 |

Total amount due. Add line 22, line 23, line 25, and line 27, then subtract line 24 |

. . . |

. . • |

29 |

||||

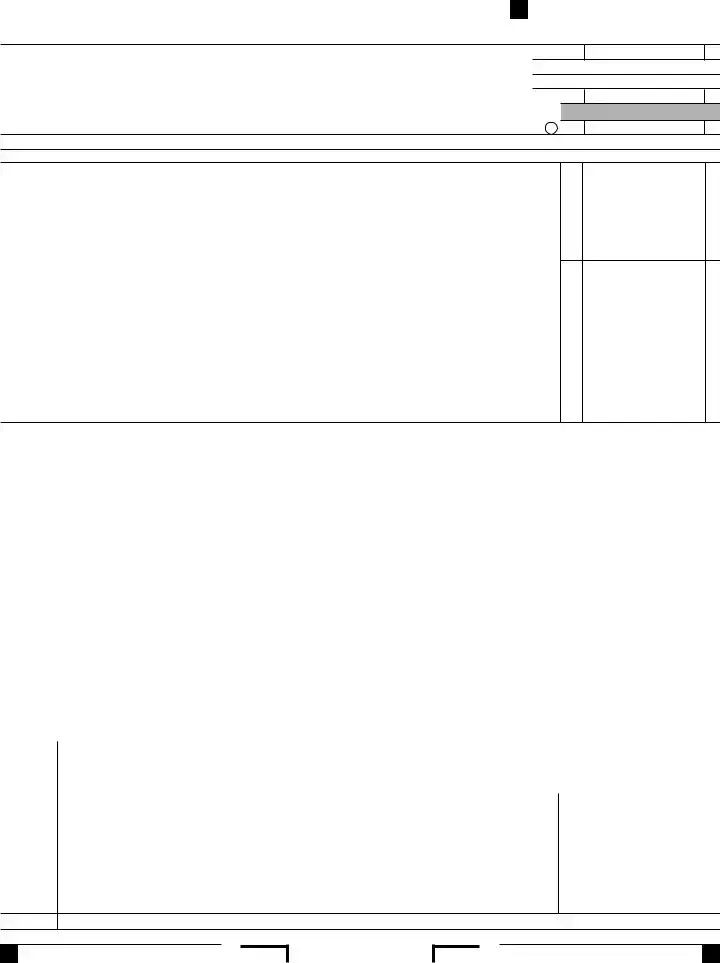

Unrelated Business Taxable Income |

|

|

|

|

|

|||||

Part I |

Unrelated Trade or Business Income |

|

|

|

|

|

||||

00

00

00

1 |

a |

Gross receipts or gross sales______________ b Less returns and allowances______________ c Balance |

• 1c |

00 |

|

2 |

Cost of goods sold and/or operations (Schedule A, line 7) |

• |

2 |

00 |

|

3 |

Gross profit. Subtract line 2 from line 1c |

• |

3 |

00 |

|

4 |

a |

Capital gain net income. See Specific Line Instructions – Trusts attach Schedule D (541) |

• 4a |

00 |

|

|

|

|

|

|

|

|

b |

Net gain (loss) from Part II, Schedule |

• 4b |

00 |

|

|

|

|

|

|

|

|

c |

Capital loss deduction for trusts |

• 4c |

00 |

|

5Income (or loss) from partnerships, limited liability companies, or S corporations. See Specific Line Instructions.

|

Attach Schedule |

• |

5 |

00 |

6 |

Rental income (Schedule C) |

• |

6 |

00 |

7 |

Unrelated |

• |

7 |

00 |

8 |

Investment income of an R&TC Section 23701g, 23701i, or 23701n organization (Schedule E) |

• |

8 |

00 |

9 |

Interest, Annuities, Royalties and Rents from controlled organizations (Schedule F) |

• |

9 |

00 |

10 |

Exploited exempt activity income (Schedule G) |

• 10 |

00 |

|

|

|

|

|

|

11 |

Advertising income (Schedule H, Part III, Column A) |

• 11 |

00 |

|

|

|

|

|

|

12 |

Other income. Attach schedule |

• 12 |

00 |

|

|

|

|

|

|

13 |

Total unrelated trade or business income. Add line 3 through line 12 |

• 13 |

00 |

|

Part II Deductions Not Taken Elsewhere (Except for contributions, deductions must be directly connected with the unrelated business income.)

14 |

Compensation of officers, directors, and trustees from Schedule I |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

14 |

|

00 |

15 |

Salaries and wages |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

15 |

|

00 |

16 |

Repairs |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

16 |

|

00 |

17 |

Bad debts |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

17 |

|

00 |

18 |

Interest. Attach schedule |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

18 |

|

00 |

19 |

Taxes. Attach schedule |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

19 |

|

00 |

20 |

Contributions. See instructions and attach schedule |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

• |

20 |

|

00 |

21 |

a Depreciation (Corporations and Associations – Schedule J) (Trusts – form FTB 3885F) |

• |

21a |

|

00 |

|

|

|

|

b Less: depreciation claimed on Schedule A. See instructions |

|

21b |

|

00 |

21 |

|

00 |

22 |

Depletion. Attach schedule |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

• |

22 |

|

00 |

23 |

a Contributions to deferred compensation plans |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

23a |

|

00 |

|

b Employee benefit programs. See instructions |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . .. |

•. . |

23b |

|

00 |

24 |

Other deductions. Attach schedule |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

24 |

|

00 |

|

25 |

Total deductions. Add line 14 through line 24 |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . .. |

•. . |

25 |

|

00 |

26 |

Unrelated business taxable income before allowable excess advertising costs. Subtract line 25 from line 13 |

26 |

|

00 |

||||

|

|

|

|

. |

• |

|

|

|

27 |

Excess advertising costs (Schedule H, Part III, Column B) |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

27 |

|

00 |

|

|

|

|

. |

• |

|

|

|

|

28 |

Unrelated business taxable income before specific deduction. Subtract line 27 from line 26 |

28 |

|

00 |

||||

|

|

|

|

. |

• |

|

|

|

29 |

Specific deduction. See instructions |

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . |

29 |

|

00 |

|

30 |

Unrelated business taxable income. Subtract line 29 from line 28. If line 28 is a loss, enter line 28 |

. . |

30 |

|

00 |

|||

Our privacy notice can be found in annual tax booklets or online. Go to ftb.ca.gov/privacy to learn about our privacy policy statement, or go to ftb.ca.gov/forms and search for 1131 to locate FTB 1131

Sign |

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and |

||||||||||

Here |

belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

||||||||||

|

|

|

|

Title |

|

Date |

|

|

• Telephone |

||

|

Signature |

▶ |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||

|

of officer |

|

|

|

|

|

|

|

|

|

|

|

Preparer’s |

|

|

|

|

Date |

|

Check if self- |

• PTIN |

||

|

|

|

|

|

|

|

|

||||

|

▶ |

|

|

|

|

|

|

▶ □ |

|

||

Paid |

signature |

|

|

|

|

|

employed |

|

|||

|

|

|

|

|

|

|

|

|

|

• Firm’s FEIN |

|

Preparer’s |

|

|

|

|

|

|

|

|

|

|

|

Firm’s name (or yours, |

|

|

|

|

|

|

|

|

|

||

Use Only |

if |

▶ |

|

|

|

|

|

||||

|

and address |

|

|

|

|

|

|

|

|

• Telephone |

|

|

|

|

|

|

|

|

|

|

|||

May the FTB discuss this return with the preparer shown above? See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . • □ Yes □ No

Side 2 Form 109 2021

3642213

| Fact Name | Description |

|---|---|

| Purpose | The California 109 form is used by exempt organizations to report unrelated business income and calculate the associated tax liability for the taxable year. |

| Filing Requirement | Organizations must file Form 109 if they have gross unrelated business income of $1,000 or more during the taxable year. |

| Governing Law | This form is governed by the California Revenue and Taxation Code, specifically Sections 23701 and 23712, which outline the tax obligations of exempt organizations. |

| Due Date | Form 109 is typically due on the 15th day of the 5th month after the end of the organization’s taxable year. |

| Amended Returns | If an organization needs to correct information reported on a previously filed Form 109, it must submit an amended return to the California Franchise Tax Board. |

Filling out the California 109 form requires attention to detail. This form is essential for reporting business income for exempt organizations. Follow the steps carefully to ensure all necessary information is included.

After completing these steps, review the form for accuracy. Ensure that all required schedules and attachments are included. Submit the form by the deadline to avoid penalties.

What is the purpose of the California 109 form?

The California 109 form is used by exempt organizations to report unrelated business taxable income (UBTI) and calculate the associated tax liability. Organizations that engage in activities not substantially related to their exempt purpose may be subject to tax on the income generated from these activities. The form ensures compliance with state tax regulations and provides necessary information for tax assessment.

Who needs to file the California 109 form?

Organizations that are recognized as tax-exempt under Internal Revenue Code (IRC) sections but generate unrelated business income must file the California 109 form. This includes charities, educational institutions, and other non-profit entities that engage in commercial activities unrelated to their primary mission. If the organization has UBTI exceeding the threshold set by the state, it is required to file this form.

What information is required on the California 109 form?

The form requires various pieces of information, including the organization's name, federal employer identification number (FEIN), and California corporation number. Additionally, it asks for details about the unrelated business income, deductions, and any applicable tax credits. Organizations must also indicate if they are filing an amended return or if this is their first return.

What is unrelated business taxable income (UBTI)?

Unrelated business taxable income refers to income generated from a trade or business that is not substantially related to the organization's exempt purpose. For example, if a charity operates a gift shop that sells items unrelated to its mission, the income from that shop would be considered UBTI. Organizations must calculate their UBTI to determine their tax liability accurately.

How is UBTI calculated on the California 109 form?

To calculate UBTI, organizations must report their gross income from unrelated business activities and subtract allowable deductions. The form provides specific lines for reporting gross receipts, costs of goods sold, and other expenses directly related to the unrelated business. The resulting figure is the UBTI, which is then subject to California tax rates.

What are the filing deadlines for the California 109 form?

The California 109 form is typically due on the 15th day of the 5th month after the end of the organization’s tax year. For organizations operating on a calendar year, this means the form is due by May 15 of the following year. If an organization needs more time, it may file for an extension, but the tax liability must still be paid by the original due date to avoid penalties.

Are there penalties for failing to file the California 109 form?

Yes, organizations that fail to file the California 109 form on time may face penalties. The state imposes fines based on the amount of tax due and the length of the delay. Additionally, failure to report UBTI accurately can lead to interest charges on unpaid taxes. It is essential for organizations to file accurately and on time to avoid these financial repercussions.

Can organizations amend their California 109 form after filing?

Yes, organizations can amend their California 109 form if they discover errors or need to update information after submission. The amended return must be filed using the same form, indicating that it is an amended return. Organizations should provide a clear explanation of the changes made and ensure that all corrections are accurately reflected to avoid issues with the state tax authorities.

Incorrect Tax Year: Ensure that you are filling out the form for the correct taxable year. Using the wrong year can lead to significant issues with your filing.

Missing Employer Identification Number (EIN): Failing to provide your EIN can delay processing. Make sure this number is accurate and included.

Improper Address Format: Ensure that your street address, city, state, and ZIP code are correctly formatted. An incorrect address can lead to miscommunication and delays.

Neglecting to Check Boxes: Many sections require you to check a box, such as whether this is your first return or if you are claiming certain tax benefits. Missing these checks can cause confusion.

Errors in Financial Calculations: Double-check all calculations, especially those involving income and deductions. Simple math errors can lead to incorrect tax liabilities.

Failing to Attach Required Schedules: Certain questions may require additional documentation or schedules. Not attaching these can result in your return being considered incomplete.

Incorrect Accounting Method: Make sure to select the correct accounting method (cash, accrual, or other). Using the wrong method can affect your reported income.

Missing Signatures: Ensure that the form is signed by an authorized person. A missing signature can result in your return being rejected.

Not Keeping Copies: Always retain a copy of your submitted form for your records. Not doing so can complicate matters if issues arise later.

Submitting Late: Be aware of deadlines for filing. Late submissions can incur penalties and interest, impacting your organization’s finances.

The California Form 109 is a crucial document for exempt organizations, particularly those engaging in unrelated business activities. When filing this form, several other forms and documents are often required to provide additional information or to fulfill specific tax obligations. Below is a list of commonly used documents that accompany the California Form 109, along with a brief description of each.

Each of these forms plays a vital role in ensuring that organizations comply with California tax regulations while accurately reporting their financial activities. Understanding the purpose and requirements of these documents can facilitate a smoother filing process and help organizations maintain their tax-exempt status.

Form 990: This document serves as the annual information return for tax-exempt organizations. Like the California 109 form, it requires organizations to report their financial activities, including income and expenses. Both forms aim to provide transparency regarding the financial health of non-profit entities.

Form 990-EZ: A simplified version of Form 990, this document is designed for smaller tax-exempt organizations. Similar to the California 109, it includes sections for reporting income, expenses, and changes in net assets, thereby ensuring that smaller organizations maintain compliance with federal regulations.

Form 1040: While primarily used by individual taxpayers, Form 1040 shares similarities with the California 109 in that both require a detailed account of income and deductions. Each form seeks to determine the tax liability or refund due, making them essential for accurate tax reporting.

Form 1065: This form is utilized by partnerships to report income, deductions, gains, and losses. Like the California 109, it requires the reporting of unrelated business taxable income, ensuring that all entities, regardless of structure, adhere to tax obligations.

Form 1120: Corporations use this form to report their income, gains, losses, and deductions. Both Form 1120 and the California 109 form necessitate a thorough accounting of business activities, reinforcing the importance of transparency in financial reporting for tax purposes.

This form is applicable to various types of organizations, including small non-profits and charitable entities. It is designed to accommodate a wide range of exempt organizations, regardless of their size.

Even if an organization does not have taxable income, it may still be required to file the California 109 form. Filing is often necessary to maintain compliance with state regulations and to report activities accurately.

Organizations outside of California that conduct business or have income sourced from California may also need to file this form. It is essential to consider the source of income, not just the location of the organization.

While both forms serve to report financial information about non-profit organizations, they are distinct documents with different requirements and purposes. Each form has its own set of instructions and guidelines.

In fact, any exempt organization that engages in unrelated business activities may need to file this form. This includes educational institutions, social clubs, and other types of non-profits.

Many organizations find the form complex due to its detailed requirements. Seeking guidance from a tax professional or accountant can help ensure accurate completion and compliance.

While it is possible to amend the form, it requires careful attention to detail. Organizations must follow specific procedures and may need to provide additional documentation to support the changes.

There are deadlines for filing the California 109 form, and missing these deadlines can result in penalties. It is crucial to be aware of the filing timeline to avoid unnecessary fees.

Organizations should maintain thorough records of their financial activities and the information reported on the California 109 form. This documentation may be necessary for future audits or inquiries from tax authorities.

Understanding the California Form 109 is essential for organizations operating within the state. Here are four key takeaways to consider: