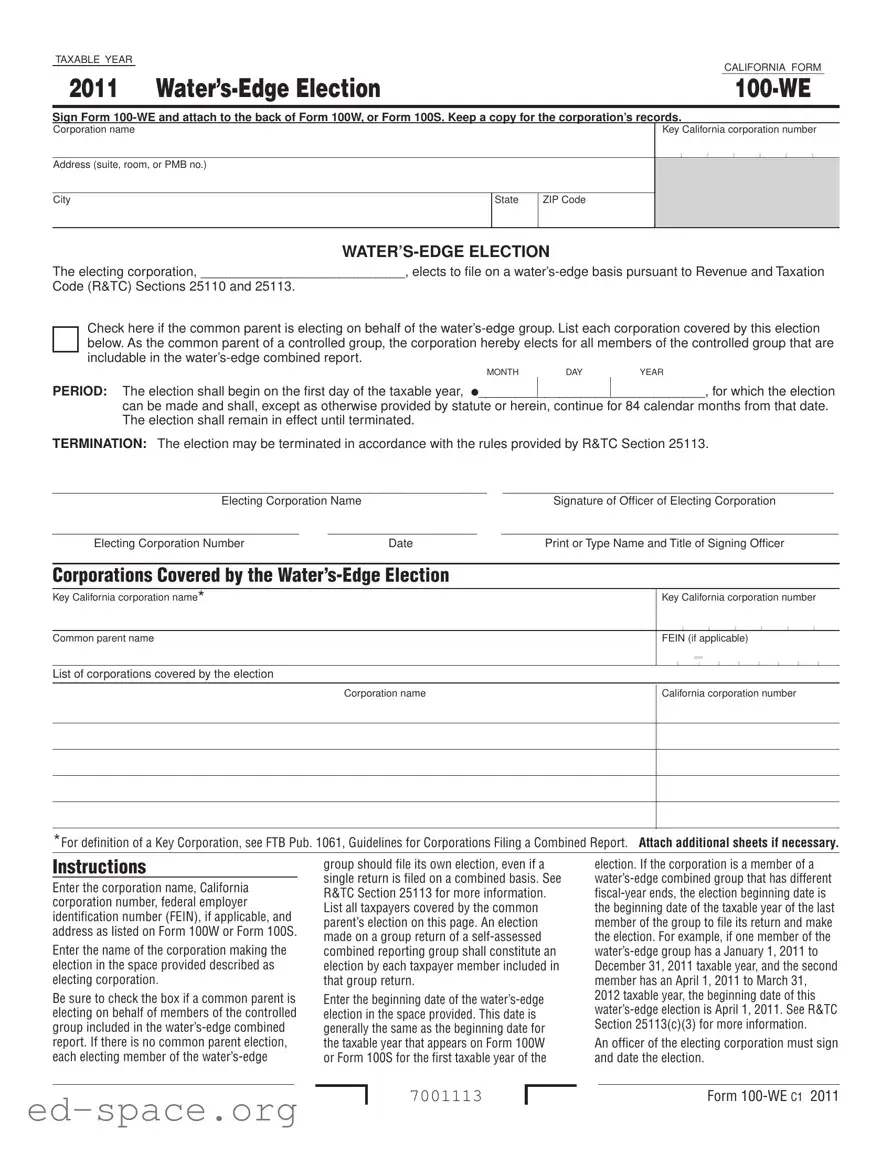

The California 100 We form, officially known as Form 100-WE, plays a crucial role for corporations electing to file on a water's-edge basis. This election allows corporations to determine their taxable income by considering only income derived from within the United States, which can significantly impact their overall tax liability. The form must be attached to either Form 100W or Form 100S, and it is essential for the electing corporation to maintain a copy for its records. When filling out the form, the corporation must provide its name, California corporation number, and address, ensuring that all details are accurate and up to date. A key aspect of this form is the option for a common parent corporation to elect on behalf of a controlled group, allowing all members to be included in the water's-edge combined report. The election period begins on the first day of the taxable year and lasts for 84 calendar months, unless terminated earlier as per the relevant tax code provisions. Proper completion of the form requires the signature of an officer from the electing corporation, confirming the validity of the election. Additionally, it is necessary to list all corporations covered by this election, which ensures clarity and compliance with the state's tax regulations. Understanding the intricacies of the California 100 We form is vital for corporations aiming to navigate their tax obligations effectively while benefiting from the potential advantages of this election.

TAXABLE YEAR

|

|

CALIFORNIA FORM |

|

|

|

2011 |

||

|

|

|

Sign Form

Corporation name

Key California corporation number

Address (suite, room, or PMB no.)

City

State

ZIP Code

The electing corporation, ____________________________, elects to file on a

Code (R&TC) Sections 25110 and 25113.

Check here if the common parent is electing on behalf of the

MONTHDAYYEAR

PERIOD: The election shall begin on the first day of the taxable year, I_______________________________, for which the election

can be made and shall, except as otherwise provided by statute or herein, continue for 84 calendar months from that date. The election shall remain in effect until terminated.

TERMINATION: The election may be terminated in accordance with the rules provided by R&TC Section 25113.

___________________________________________________________________ |

___________________________________________________ |

|

Electing Corporation Name |

Signature of Officer of Electing Corporation |

|

______________________________________ |

_______________________ |

____________________________________________________ |

Electing Corporation Number |

Date |

Print or Type Name and Title of Signing Officer |

Corporations Covered by the

Key California corporation name*

Key California corporation number

Common parent name

FEIN (if applicable)

List of corporations covered by the election

Corporation name

California corporation number

*For definition of a Key Corporation, see FTB Pub. 1061, Guidelines for Corporations Filing a Combined Report. Attach additional sheets if necessary.

Instructions

Enter the corporation name, California corporation number, federal employer identification number (FEIN), if applicable, and address as listed on Form 100W or Form 100S.

Enter the name of the corporation making the election in the space provided described as electing corporation.

Be sure to check the box if a common parent is electing on behalf of members of the controlled group included in the

group should file its own election, even if a single return is filed on a combined basis. See R&TC Section 25113 for more information. List all taxpayers covered by the common parent’s election on this page. An election made on a group return of a

Enter the beginning date of the

election. If the corporation is a member of a

2012 taxable year, the beginning date of this

An officer of the electing corporation must sign and date the election.

7001113

Form

| Fact Name | Details |

|---|---|

| Form Purpose | The California Form 100-WE is used for the Water's-Edge Election, allowing corporations to file on a water's-edge basis. |

| Governing Law | This form is governed by the California Revenue and Taxation Code, specifically Sections 25110 and 25113. |

| Taxable Year | The election begins on the first day of the taxable year for which it is made, as indicated on Form 100W or Form 100S. |

| Duration of Election | The election lasts for 84 calendar months, unless terminated earlier according to the relevant statutes. |

| Termination Rules | Corporations can terminate the election following the rules outlined in R&TC Section 25113. |

| Common Parent Election | If a common parent elects on behalf of the water’s-edge group, this must be indicated on the form. |

| Corporations Covered | All corporations included in the common parent’s election must be listed on the form, with their respective California corporation numbers. |

| Signature Requirement | An officer of the electing corporation must sign and date the form for it to be valid. |

| Additional Information | For definitions and guidelines, refer to FTB Publication 1061 regarding corporations filing a combined report. |

Filling out the California 100 We form requires careful attention to detail. This form is essential for corporations electing to file on a water’s-edge basis. Follow these steps to complete the form accurately.

Once the form is completed, it should be attached to the back of Form 100W or Form 100S. Ensure all necessary information is accurate to avoid any issues with processing.

What is the purpose of the California 100 We form?

The California 100 We form is used by corporations to elect to file on a water’s-edge basis. This election allows a corporation to include only certain income and deductions from foreign affiliates in its California tax return. It is particularly beneficial for corporations with international operations, as it can help streamline tax reporting and potentially reduce tax liability. By making this election, the corporation agrees to follow specific rules outlined in the California Revenue and Taxation Code.

How long does the water’s-edge election last?

The election begins on the first day of the taxable year specified on the form and continues for 84 calendar months, unless terminated earlier according to the rules provided by the Revenue and Taxation Code. It is important to note that once the election is made, it remains in effect until the corporation decides to terminate it. Corporations should keep detailed records of their election and any related documentation for future reference.

Who can make the water’s-edge election?

The electing corporation, typically the common parent of a controlled group, can make the water’s-edge election on behalf of all members of that group. If there is no common parent, each corporation that wishes to elect must file its own election, even if a combined return is being submitted. It is crucial to list all corporations covered by the election on the form to ensure compliance and proper reporting.

What information is required to complete the form?

To complete the California 100 We form, you will need to provide several key pieces of information. This includes the corporation name, California corporation number, and federal employer identification number (FEIN), if applicable. You must also enter the beginning date of the water’s-edge election, which typically aligns with the taxable year start date. Additionally, an officer of the corporation must sign and date the form to validate the election. Be sure to keep a copy for your records.

Failing to include the correct corporation name and California corporation number. This information must match what is on Form 100W or Form 100S.

Not checking the box if a common parent is electing on behalf of the water’s-edge group. This oversight can lead to confusion regarding the election's validity.

Neglecting to list all corporations covered by the election. Each member of the controlled group must be accounted for to ensure compliance with tax regulations.

Entering an incorrect beginning date for the water’s-edge election. This date should align with the taxable year start date on Form 100W or Form 100S.

Forgetting to have an officer's signature on the form. The election is not valid without the proper authorization from an officer of the electing corporation.

Not keeping a copy of the form for the corporation’s records. Retaining a copy is crucial for future reference and compliance verification.

Overlooking the need to attach the form to the back of Form 100W or Form 100S. This is necessary for the election to be recognized and processed correctly.

The California 100 We form is a critical document for corporations electing to file on a water’s-edge basis. However, it is often accompanied by other important forms and documents that facilitate compliance with state tax regulations. Understanding these documents can streamline the filing process and ensure that all necessary information is accurately submitted.

Incorporating these forms and documents into the filing process is essential for any corporation electing the water’s-edge option in California. Each document plays a significant role in ensuring compliance and facilitating accurate reporting. It is advisable to review these forms carefully and seek assistance if needed to avoid potential pitfalls.

The California Form 100-WE is a specific document used by corporations to elect to file on a water’s-edge basis. Several other documents share similarities with this form in terms of purpose, structure, and the information required. Below is a list of seven such documents.

When filling out the California 100 We form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are seven things to do and avoid:

Following these guidelines can help streamline the process and ensure compliance with California tax regulations.

Here are four common misconceptions about the California 100 We form:

Understanding the California 100 We form is essential for corporations electing to file on a water's-edge basis. Here are key takeaways to keep in mind: