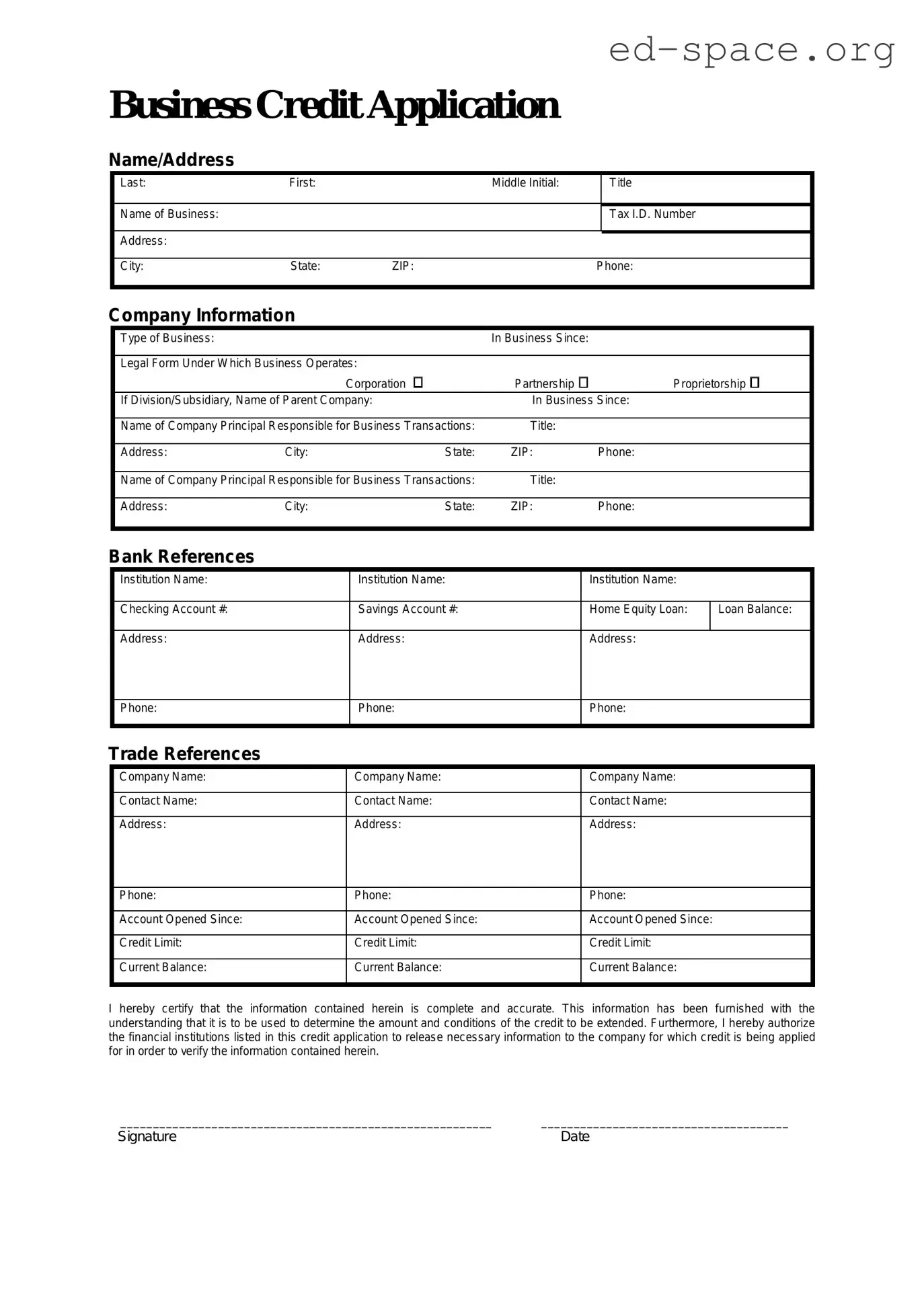

Applying for business credit involves a critical step: completing a Business Credit Application form. This document plays a pivotal role in securing financial support from lenders or suppliers, making it fundamental for the growth and sustainability of a business. Designed to assess the creditworthiness of a company, this form collects comprehensive details from the applicant, including business information, financial statements, and references. Its completion requires accuracy and thoroughness, as it provides lenders with the necessary data to make informed decisions regarding credit limits and terms. Additionally, it helps in building a formal business relationship between the borrower and the lender, establishing trust and reliability from the outset. Understanding each component of this form, from personal to financial information, is essential for businesses aiming to successfully navigate the intricate process of credit application and approval.

Business Credit Application

Name/Address

Last: |

First: |

|

Middle Initial: |

|

Title |

|

|

|

|

|

|

Name of Business: |

|

|

|

|

Tax I.D. Number |

|

|

|

|

|

|

Address: |

|

|

|

|

|

|

|

|

|

|

|

City: |

State: |

ZIP: |

|

Phone: |

|

|

|

|

|

|

|

Company Information

|

Type of Business: |

|

|

|

In Business Since: |

|

|

|

|

|

|

|

|

|

|

||

|

Legal Form Under Which Business Operates: |

|

|

|

|

|||

|

|

|

Corporation |

Partnership |

Proprietorship |

|

||

|

If Division/Subsidiary, Name of Parent Company: |

In Business Since: |

|

|||||

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

|

|

Bank References |

|

|

|

|

|

|

|

|

|

Institution Name: |

|

|

Institution Name: |

|

Institution Name: |

||

|

|

|

|

|

|

|

|

|

|

Checking Account #: |

|

|

Savings Account #: |

|

Home Equity Loan: |

ILoan Balance: |

|

|

Address: |

|

|

Address: |

|

Address: |

|

|

Phone:

Phone:

Phone:

Trade References

Company Name: |

Company Name: |

Company Name: |

|

|

|

Contact Name: |

Contact Name: |

Contact Name: |

|

|

|

Address: |

Address: |

Address: |

|

|

|

Phone: |

Phone: |

Phone: |

|

|

|

Account Opened Since: |

Account Opened Since: |

Account Opened Since: |

|

|

|

Credit Limit: |

Credit Limit: |

Credit Limit: |

|

|

|

Current Balance: |

Current Balance: |

Current Balance: |

|

|

|

I hereby certify that the information contained herein is complete and accurate. This information has been furnished with the understanding that it is to be used to determine the amount and conditions of the credit to be extended. Furthermore, I hereby authorize the financial institutions listed in this credit application to release necessary information to the company for which credit is being applied for in order to verify the information contained herein.

_________________________________________________________ ______________________________________

Signature |

Date |

| Fact Name | Description |

|---|---|

| Purpose | The Business Credit Application form is designed to gather necessary information from a business seeking credit terms with a lender or supplier. |

| Content | This form typically requests details about the business applying for credit, including business name, contact information, type of business, financial statements, credit references, and bank account information. |

| Benefits | Completing a Business Credit Application is the first step in establishing a credit line or terms, enabling businesses to procure goods or services in advance of payment. |

| State-Specific Forms | Some states may have specific requirements or additional provisions that need to be included in the form, influenced by local commercial codes or regulations. |

| Governing Law(s) | The form is governed by the Uniform Commercial Code (UCC) in most states, which regulates commercial transactions. However, specific laws and regulations can vary by state. |

| Importance of Accuracy | Providing accurate and complete information is crucial as it affects the assessment of creditworthiness and the terms of credit offered by the lender or supplier. |

Applying for business credit is a vital step for many companies aiming to expand their operations or manage their finances more effectively. This process involves completing a Business Credit Application form, which serves as a formal request for credit from a financial institution or supplier. It's crucial to fill out this form accurately and completely to increase your chances of approval. The instructions below will guide you through this process, ensuring you provide all the necessary information to make a compelling case for your business.

Once your Business Credit Application form is filled out and submitted, the lender will review your request. This process can vary in length, but you will typically be notified of the decision within a few weeks. If approved, the lender will provide further instructions on how to proceed. Remember, receiving credit is a responsibility as much as it is a benefit, so ensure your business is prepared to manage it effectively.

What is a Business Credit Application form?

A Business Credit Application form is a document used by companies to apply for credit from vendors or lenders. This form collects information about the business and its principals, financial health, and creditworthiness. It serves as the basis for the credit provider to make an informed decision regarding the credit application.

Who needs to fill out a Business Credit Application form?

Any business entity that seeks to obtain credit from a supplier, bank, or financial institution should complete a Business Credit Application form. This applies to all types of businesses, including sole proprietorships, partnerships, limited liability companies, and corporations that are looking to establish a line of credit or credit terms with a creditor.

What information is required on a Business Credit Application form?

The form typically asks for the business name, address, tax identification number, nature of the business, and credit amount requested. It also requires detailed information about the owners or principals, including their names, addresses, and social security numbers. Additionally, financial details such as bank accounts, trade references, and authorization for the credit provider to perform a credit check may be necessary.

How does the Business Credit Application process work?

Once a business submits a completed credit application form, the credit provider reviews the provided information, conducts a credit check, and evaluates the business's financial stability and credit history. The credit provider may also contact the trade references listed on the application. Based on this review, the provider will decide whether to approve the credit application, set a credit limit, and determine the terms of credit.

Can a Business Credit Application be denied, and what are the reasons?

Yes, a Business Credit Application can be denied. Common reasons for denial include insufficient credit history, low credit scores, poor financial health of the business, and previous defaults on loans or credit agreements. The creditor must provide a notice explaining the reason for the denial, in accordance with the Fair Credit Reporting Act (FCRA).

Are there any best practices for completing a Business Credit Application form?

Ensure that all information provided on the form is accurate and complete. Double-check financial information, and include up-to-date contact information for trade references. It's also advisable to include a cover letter explaining the business's background, the purpose of the credit request, and how the credit will be used to help the business grow. Providing comprehensive and transparent information can increase the likelihood of approval.

Filling out a Business Credit Application form is a common step for businesses seeking to establish a credit line with suppliers and financial institutions. This document essentially helps entities evaluate the creditworthiness of a business. However, the simplicity of the task belies the complexity and potential pitfalls involved. Here are eight common mistakes businesses make during this process:

Not reading the instructions carefully. Every form comes with its set of instructions, and overlooking these can lead to errors in the application that could have been easily avoided.

Leaving sections incomplete. It might seem innocuous to skip a question if you’re unsure of the answer, but every section of the application plays a role in the evaluation process.

Inaccurate financial information. Providing financial details that are inaccurate, whether unintentionally or not, can severely impact the outcome of the application.

Failing to provide the necessary documentation. Most applications will require supplemental documents. Neglecting to attach these can delay or even void the process.

Ignoring personal credit history. In many cases, especially for small businesses, personal credit history plays a critical role in the decision-making process.

Overlooking terms and conditions. The eagerness to get credit can lead some to gloss over the terms and conditions, missing out on crucial information regarding rates, fees, and repayment terms.

Not using the correct business name or legal structure. This might lead to issues in the credit agreement or problems with legal liability.

Forgetting to sign and date the application. It’s a simple step, but an unsigned or undated application is incomplete and will likely be rejected.

When businesses endeavor to fill out a Business Credit Application form, attention to detail can make all the difference. Avoiding these common mistakes not only simplifies the approval process but also paves the way for establishing a sound credit relationship. Careful completion of the form, supported by accurate and thorough documentation, is essential. The goal is not only to secure credit but to establish a foundation for future financial interactions and opportunities. With thoughtful preparation, businesses can navigate this process smoothly, avoiding pitfalls and setting themselves up for success.

When a business applies for credit, the Business Credit Application form is just the beginning. To fully evaluate the creditworthiness of a business, lenders often request additional documents. These materials provide a more comprehensive view of the business's financial health, past credit management, and the ability to meet its financial commitments. Here's a breakdown of other forms and documents commonly required alongside the Business Credit Application form.

Collectively, these documents paint a comprehensive picture of a business's fiscal responsibility and potential for growth. By thoroughly preparing and organizing these materials, a business can streamline the credit application process and position itself as a favorable candidate for credit approval.

Personal Credit Application: Similar to a Business Credit Application, this document is used by individuals seeking credit. Both forms gather financial information to assess creditworthiness, but the Personal Credit Application focuses on individual financial history rather than that of a business.

Loan Application Form: This form is used by individuals or businesses seeking a loan. Like the Business Credit Application, it collects detailed financial information and is used to evaluate the applicant's ability to repay the borrowed funds. Both require disclosures of financial status and credit history.

Vendor Credit Application: Businesses use this document to apply for credit terms with suppliers. It is similar to a Business Credit Application as it assesses a company's financial stability and creditworthiness to determine payment terms.

Mortgage Application: Used by individuals and businesses to apply for a mortgage loan. Both this and the Business Credit Application collect extensive financial details to evaluate creditworthiness and the ability to meet payment obligations.

Business Account Application: Companies fill out this form to open an account with a financial institution. It is similar to a Business Credit Application in that it requires company information, including financial data, to establish the account.

Credit Card Application: Whether for personal or business use, this form assesses the applicant's credit history and financial health, similar to the Business Credit Application. Both determine the applicant's credit limit based on their creditworthiness.

Lease Application: Used by businesses to lease property or equipment, it collects financial information to ensure the lessee can meet the lease payments, akin to how a Business Credit Application evaluates a business's ability to fulfill credit obligations.

Supplier Credit Application: Similar to the Vendor Credit Application, this document is filled out by businesses seeking credit terms from their suppliers. It evaluates the financial health of the business to establish payment terms.

Franchise Application: This form is used by individuals or entities looking to open a franchise. It includes a thorough assessment of financial information similar to a Business Credit Application to determine if the applicant can financially support the franchise.

Investment Account Application: Similar to a Business Account Application, this document is used by businesses wanting to open an investment account. It requires detailed financial information to evaluate the business's investing capabilities.

Filling out a Business Credit Application form is a crucial step for businesses looking to establish or extend their credit. The information you provide will be analyzed by lenders to determine your business's creditworthiness. To help you navigate this process, here are 10 essential dos and don'ts:

Just as there are important steps to take, there are also pitfalls you should avoid:

When dealing with the Business Credit Application form, many misconceptions can lead to confusion and mistakes. Clearing up these errors is crucial for businesses to manage their financial relations properly. Here are four common misconceptions:

Only Large Businesses Need to Fill It Out: Many assume that business credit applications are strictly for large corporations. However, businesses of all sizes seeking credit from lenders, suppliers, or vendors must complete this form. It's a standard procedure that facilitates the assessment of creditworthiness, regardless of the company's size.

It's Just About Checking Credit Scores: While assessing credit scores is a significant component, the process goes beyond that. The application provides a comprehensive view of the business, including its financial health, payment history, and other details. This information helps creditors make informed decisions and tailor credit terms to the applicant's specific situation.

Personal Information Is Irrelevant: Contrary to this belief, personal information about the owners or proprietors is often required, especially in small businesses. This is because the personal financial behavior of the owners can be indicative of the business's credit management. Creditors use this data to gauge the risk involved in extending credit.

Once Approved, Terms Are Fixed: Another misconception is that terms of credit are static once the application is approved. In reality, credit terms can be negotiated and may change over time based on the business relationship, payment history, and market conditions. It's important for businesses to communicate with their creditors and discuss terms periodically.

Businesses should approach the Business Credit Application process with a clear understanding to foster healthy financial relationships and secure the most advantageous terms possible.

Filling out a Business Credit Application form is a critical step for businesses aiming to establish or extend credit terms with vendors or suppliers. This process requires attention to detail and a clear understanding of what information needs to be provided. Below are key takeaways that businesses should keep in mind when completing and using the form:

By keeping these key points in mind, businesses can streamline the credit application process and establish beneficial credit terms, allowing for more flexibility in managing finances and fostering growth opportunities.

What Is a Medevac Flight - The form helps ensure that patients receive the best possible care while being evacuated.

Blue Cross Mailing Address for Claims - Completing this form helps to ensure that all necessary steps are taken before a dismissal occurs.

Gun Card - A $75 processing fee must accompany the application submission.