In the realm of personal and business finance, the Arkansas Promissory Note form serves as a crucial tool for establishing clear agreements between lenders and borrowers. This legally binding document outlines the terms of a loan, including the principal amount, interest rate, repayment schedule, and any applicable fees. It ensures that both parties understand their rights and obligations, thereby minimizing the potential for disputes down the line. The form typically includes spaces for both the lender and borrower to provide their names and contact information, as well as a detailed description of the loan's terms. Additionally, it may incorporate clauses that address late payments, default scenarios, and the legal jurisdiction governing the agreement. By utilizing this form, individuals and businesses in Arkansas can navigate their financial transactions with greater confidence and clarity.

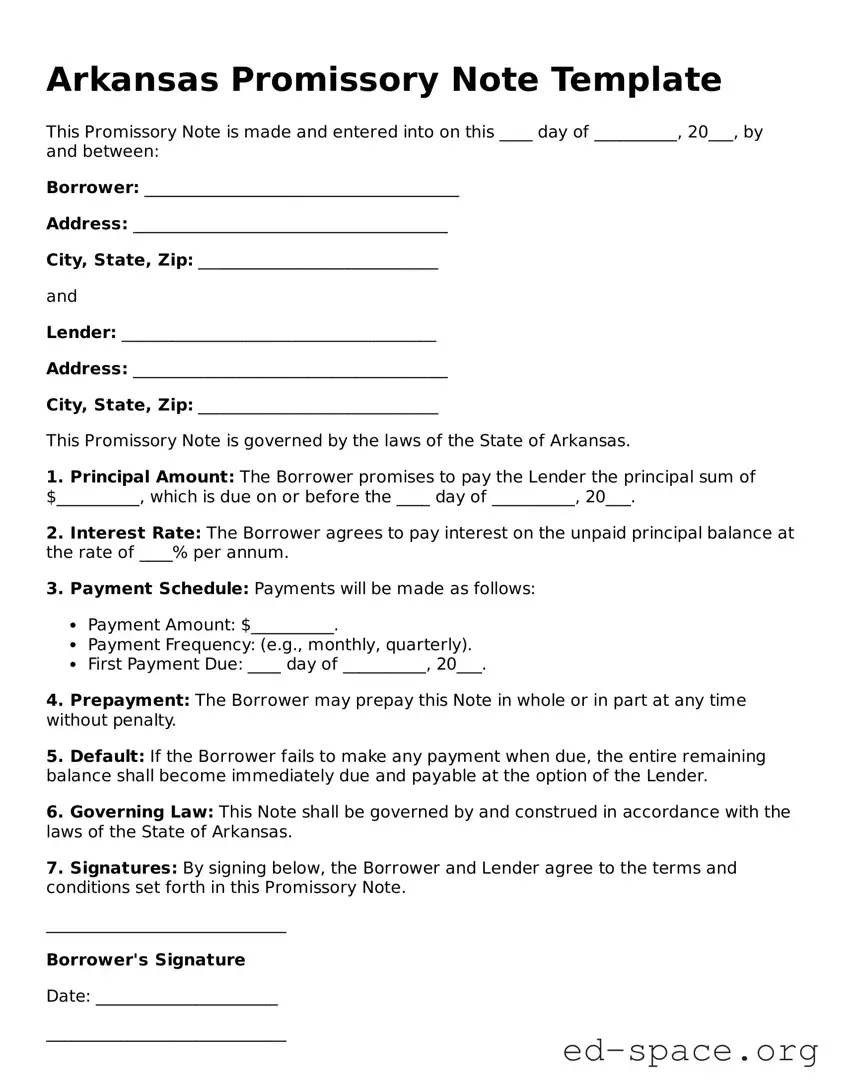

Arkansas Promissory Note Template

This Promissory Note is made and entered into on this ____ day of __________, 20___, by and between:

Borrower: ______________________________________

Address: ______________________________________

City, State, Zip: _____________________________

and

Lender: ______________________________________

Address: ______________________________________

City, State, Zip: _____________________________

This Promissory Note is governed by the laws of the State of Arkansas.

1. Principal Amount: The Borrower promises to pay the Lender the principal sum of $__________, which is due on or before the ____ day of __________, 20___.

2. Interest Rate: The Borrower agrees to pay interest on the unpaid principal balance at the rate of ____% per annum.

3. Payment Schedule: Payments will be made as follows:

4. Prepayment: The Borrower may prepay this Note in whole or in part at any time without penalty.

5. Default: If the Borrower fails to make any payment when due, the entire remaining balance shall become immediately due and payable at the option of the Lender.

6. Governing Law: This Note shall be governed by and construed in accordance with the laws of the State of Arkansas.

7. Signatures: By signing below, the Borrower and Lender agree to the terms and conditions set forth in this Promissory Note.

_____________________________

Borrower's Signature

Date: ______________________

_____________________________

Lender's Signature

Date: ______________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specific amount of money to a designated person at a specified time. |

| Governing Law | In Arkansas, promissory notes are governed by the Uniform Commercial Code (UCC), specifically under Article 3. |

| Requirements | The note must include the date, amount, payee, and signatures of the maker and, if applicable, the endorser. |

| Interest Rate | Arkansas law allows for the inclusion of an interest rate, which must be clearly stated in the note. |

| Default Terms | It is advisable to specify what constitutes a default and the consequences of defaulting on the note. |

| Transferability | Promissory notes in Arkansas can be transferred to another party, making them negotiable instruments. |

| Enforcement | If the borrower defaults, the lender can enforce the note through legal action to recover the owed amount. |

| Statute of Limitations | In Arkansas, the statute of limitations for enforcing a promissory note is typically five years from the date of default. |

After you have gathered all necessary information, you are ready to fill out the Arkansas Promissory Note form. This document will require specific details about the borrower, the lender, and the terms of the loan. Follow these steps carefully to ensure the form is completed accurately.

Once the form is filled out, make sure to keep a copy for your records. The original should be given to the lender. Review the completed document for any errors before finalizing it.

What is a Promissory Note in Arkansas?

A Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a defined time or on demand. In Arkansas, this document outlines the terms of the loan, including the principal amount, interest rate, payment schedule, and any penalties for late payments. It serves as a legal record of the agreement between the borrower and the lender.

Who can use a Promissory Note in Arkansas?

Any individual or business can use a Promissory Note in Arkansas. Whether you are lending money to a friend, family member, or a business entity, having a written agreement helps protect both parties. It is especially important in situations involving larger sums of money or formal business transactions.

What are the essential components of an Arkansas Promissory Note?

An effective Promissory Note should include several key components: the names and addresses of both the borrower and the lender, the principal amount being borrowed, the interest rate (if applicable), the repayment schedule, and any terms regarding default. Additionally, signatures from both parties and the date of the agreement are crucial for validation.

Is it necessary to have a lawyer review a Promissory Note?

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended agreement. This helps maintain clarity and protects the interests of both the borrower and the lender.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They may attempt to collect the debt through direct communication or formal demand. If necessary, legal action can be taken to recover the owed amount. The terms outlined in the Promissory Note regarding default will guide the lender's actions.

Is a Promissory Note enforceable in Arkansas?

Yes, a properly executed Promissory Note is generally enforceable in Arkansas. As long as it meets the legal requirements and both parties have signed it, the lender can seek legal recourse if the borrower fails to fulfill their obligations. Having a clear, written agreement strengthens the lender’s position in any potential disputes.

When filling out the Arkansas Promissory Note form, it's crucial to pay attention to detail. Many individuals make common mistakes that can lead to confusion or legal complications. Here are eight mistakes to avoid:

One of the most frequent errors is failing to provide all required information. Ensure that you fill in all sections, including names, addresses, and loan amounts.

Writing the wrong date can cause significant issues. Always double-check the date of the agreement and the payment due dates.

If your loan includes interest, clearly state the interest rate. Leaving this out can lead to misunderstandings.

Using vague terms can create confusion. Be clear and specific about the terms of the loan to avoid misinterpretation.

Both the borrower and lender must sign the document. Forgetting to sign can render the note invalid.

Failing to keep a copy of the signed note can be detrimental. Always retain a copy for your records.

Depending on the situation, you may need witnesses or a notary. Verify if this is necessary for your note.

Rushing through the process often leads to mistakes. Take the time to review the completed form before submission.

By being aware of these common pitfalls, you can ensure that your Arkansas Promissory Note is filled out correctly, minimizing the risk of complications down the line.

A Promissory Note in Arkansas is often accompanied by several other documents to ensure clarity and legal protection for all parties involved. Below is a list of forms and documents that are frequently used alongside the Arkansas Promissory Note.

Utilizing these additional documents can help clarify the relationship between the lender and borrower, ensuring that all parties understand their rights and responsibilities. Proper documentation is essential for a smooth lending process and can prevent misunderstandings in the future.

Loan Agreement: A loan agreement outlines the terms of a loan, including the amount borrowed, interest rate, and repayment schedule. Like a promissory note, it is a legally binding document that establishes the borrower's obligation to repay the loan.

Mortgage: A mortgage is a specific type of loan used to purchase real estate. It includes a promissory note as part of the agreement, detailing the borrower's promise to repay the loan, along with a security interest in the property.

IOU (I Owe You): An IOU is a simple acknowledgment of a debt. While less formal than a promissory note, it serves a similar purpose by indicating that one party owes money to another and outlines the basic terms of repayment.

Security Agreement: A security agreement is a contract that grants a lender a security interest in specific assets. It often accompanies a promissory note, providing additional assurance that the borrower will repay the loan.

Installment Agreement: An installment agreement details the terms under which a borrower agrees to repay a debt in regular payments over time. It shares similarities with a promissory note, as both documents require the borrower to fulfill their payment obligations.

When filling out the Arkansas Promissory Note form, it’s crucial to pay attention to detail. Here are ten things you should and shouldn't do:

Understanding the Arkansas Promissory Note form can be challenging due to several misconceptions that often circulate. Here are ten common misunderstandings, along with clarifications to help you navigate this important financial document.

By debunking these misconceptions, individuals can better understand the role of promissory notes in their financial dealings and ensure they are using them correctly.

When dealing with the Arkansas Promissory Note form, several important aspects should be kept in mind. Here are key takeaways that can help ensure a smooth process.

By keeping these points in mind, both borrowers and lenders can navigate the process of creating and utilizing an Arkansas Promissory Note more effectively.