The Appraisal HVCC form plays a crucial role in the mortgage lending process, ensuring that property valuations are conducted fairly and without undue influence. This form is utilized by lenders to certify the accuracy of the attached appraisal for a specific property, which includes essential details such as the borrower's name, loan number, property address, and appraisal date. One of the key aspects of the HVCC form is the emphasis on maintaining a clear separation between the appraiser and the lender's loan production staff. This separation is vital to prevent any potential conflicts of interest that could arise from direct communication. The lender must ensure that the appraiser is selected based on their qualifications and proximity to the subject property, reinforcing compliance with the Home Valuation Code of Conduct (HVCC). Additionally, the form outlines prohibited influences on the appraisal, including the owner's estimate of value, target value, and any information that could sway the appraiser's opinion, ensuring that the appraisal remains objective and based solely on factual data. The lender also certifies that the appraiser's qualifications have been verified and that they do not appear on any exclusionary lists, further safeguarding the integrity of the appraisal process. By signing this form, the lender affirms that the appraisal meets all HVCC requirements, thereby fostering transparency and trust in property valuations.

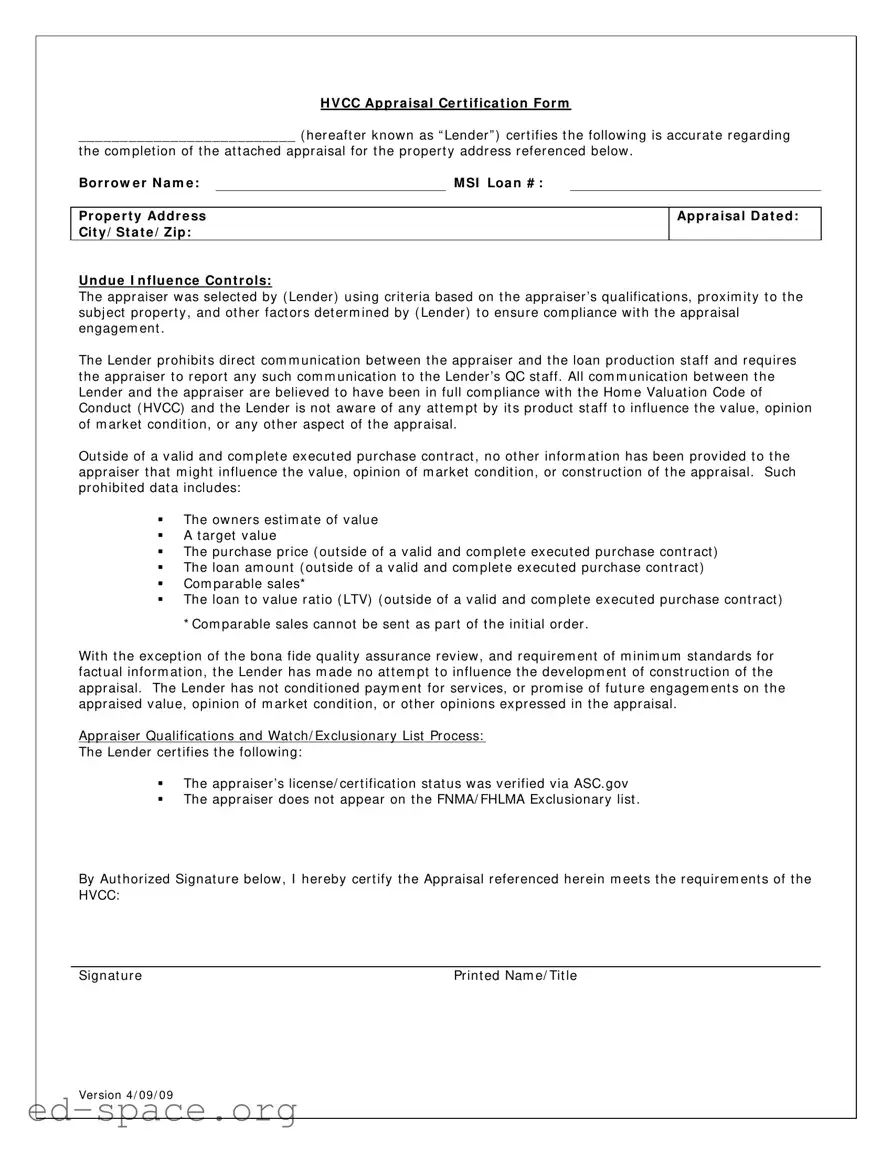

H V CC Ap p r a isa l Ce r t if ica t ion For m

__________________________ ( her eaft er k now n as “ Lender ” ) cer t ifies t he follow ing is accur at e r egar ding

t he com plet ion of t he at t ached appr aisal for t he pr oper t y addr ess r efer enced below .

Bor r ow e r N a m e : |

|

M SI Loa n # : |

Pr op e r t y Ad d r e ss Cit y / St a t e / Z ip :

Ap p r a isa l D a t e d :

U n d u e I n f lu e n ce Con t r ols:

The appr aiser w as select ed by ( Lender ) using crit er ia based on t he appr aiser ’s qualificat ions, pr ox im it y t o t he subj ect pr oper t y , and ot her fact or s det er m ined by ( Lender ) t o ensur e com pliance w it h t he appr aisal engagem ent .

The Lender pr ohibit s dir ect com m unicat ion bet w een t he appr aiser and t he loan pr oduct ion st aff and r equir es t he appr aiser t o r epor t any such com m unicat ion t o t he Lender ’s QC st aff . All com m unicat ion bet w een t he Lender and t he appr aiser ar e believ ed t o hav e been in full com pliance w it h t he Hom e Valuat ion Code of Conduct ( HVCC) and t he Lender is not aw ar e of any at t em pt by it s pr oduct st aff t o influence t he v alue, opinion of m ar k et condit ion, or any ot her aspect of t he appr aisal.

Out side of a v alid and com plet e ex ecut ed pur chase cont r act , no ot her infor m at ion has been pr ov ided t o t he appr aiser t hat m ight influence t he v alue, opinion of m ar k et condit ion, or const r uct ion of t he appr aisal. Such pr ohibit ed dat a includes:

The ow ner s est im at e of v alue

A t ar get v alue

|

The pur chase pr ice ( out side of a v alid and com plet e ex ecut ed pur chase cont r act ) |

|

The loan am ount ( out side of a v alid and com plet e ex ecut ed pur chase cont r act ) |

Com par able sales*

The loan t o v alue r at io ( LTV) ( out side of a v alid and com plet e ex ecut ed pur chase cont r act )

* Com par able sales cannot be sent as par t of t he init ial or der .

Wit h t he ex cept ion of t he bona fide qualit y assur ance r ev iew , and r equir em ent of m inim um st andar ds for fact ual infor m at ion, t he Lender has m ade no at t em pt t o influence t he dev elopm ent of const r uct ion of t he appr aisal. The Lender has not condit ioned pay m ent for ser v ices, or pr om ise of fut ur e engagem ent s on t he appr aised v alue, opinion of m ar k et condit ion, or ot her opinions ex pr essed in t he appr aisal.

Appr aiser Qualificat ions and Wat ch/ Ex clusionar y List Pr ocess:

The Lender cer t ifies t he follow ing:

The appr aiser ’s license/ cer t ificat ion st at us w as v er ified v ia ASC. gov

The appr aiser does not appear on t he FNMA/ FHLMA Ex clusionar y list .

By Aut hor ized Signat ur e below , I her eby cer t ify t he Appraisal r efer enced her ein m eet s t he r equir em ent s of t he HVCC:

Signat ur e |

Pr int ed Nam e/ Tit le |

Ver sion 4/ 09/ 0 9

| Fact Name | Description |

|---|---|

| Purpose | The Appraisal HVCC form certifies the accuracy of the appraisal for a specific property. |

| Borrower Information | It includes the borrower's name and loan number for identification purposes. |

| Property Address | The form requires the complete address of the property being appraised. |

| Appraisal Date | The date of the appraisal must be clearly stated on the form. |

| Selection Criteria | The lender selects the appraiser based on qualifications and proximity to the property. |

| Communication Restrictions | Direct communication between the appraiser and loan production staff is prohibited. |

| Compliance Assurance | The lender certifies compliance with the Home Valuation Code of Conduct (HVCC). |

| Prohibited Information | Specific information that could influence the appraisal value is not allowed. |

| Quality Assurance Review | A bona fide quality assurance review is permitted under certain conditions. |

| Verification of Appraiser | The lender verifies the appraiser’s licensing status via the ASC website. |

Filling out the Appraisal HVCC form is a straightforward process that requires careful attention to detail. Once completed, this form will serve as a certification regarding the appraisal of a property, ensuring compliance with relevant regulations. Follow these steps to fill out the form accurately.

What is the Appraisal HVCC form?

The Appraisal HVCC form is a certification document used by lenders to ensure that appraisals are conducted in compliance with the Home Valuation Code of Conduct (HVCC). It certifies the accuracy of the appraisal process and outlines the lender's commitment to maintaining independence between the appraisal and loan production staff.

Why is the HVCC important?

The HVCC was established to promote transparency and fairness in the appraisal process. It aims to prevent conflicts of interest and ensure that appraisals are unbiased and based solely on the property's market value. This helps protect consumers and maintain the integrity of the mortgage lending process.

Who selects the appraiser?

The lender is responsible for selecting the appraiser. This selection is based on the appraiser’s qualifications, proximity to the property, and other factors deemed necessary to ensure compliance with the appraisal engagement. The lender prohibits direct communication between the appraiser and loan production staff to avoid any undue influence.

What communication is allowed between the lender and the appraiser?

All communication between the lender and the appraiser must comply with the HVCC. The lender is not aware of any attempts by its staff to influence the appraisal value or any related opinions. Any communication that could affect the appraisal must be reported to the lender's quality control staff.

What information should not be provided to the appraiser?

To maintain objectivity, the appraiser should not receive certain information. This includes the owner's estimate of value, target value, purchase price (unless part of a valid purchase contract), loan amount (unless part of a valid purchase contract), comparable sales data, and loan-to-value ratio (LTV) outside of a valid purchase contract.

How does the lender ensure the appraiser's qualifications?

The lender verifies the appraiser’s license or certification status through the Appraisal Subcommittee (ASC) website. This ensures that the appraiser is properly qualified to conduct the appraisal in accordance with applicable regulations.

What is the exclusionary list, and why is it relevant?

The exclusionary list includes individuals who are barred from performing appraisals for certain reasons, such as disciplinary actions or violations of appraisal standards. The lender certifies that the appraiser does not appear on this list, ensuring that only qualified appraisers are used.

What happens if there is a violation of the HVCC?

If there is a violation of the HVCC, it could lead to serious consequences for the lender, including penalties and potential legal action. It is crucial for lenders to adhere strictly to the HVCC guidelines to avoid any issues that could undermine the appraisal process.

How is the Appraisal HVCC form signed and certified?

The form is signed by an authorized representative of the lender. By signing, the representative certifies that the appraisal meets the requirements of the HVCC, ensuring compliance and accountability in the appraisal process.

Incomplete Information: Failing to fill out all required fields, such as the borrower’s name or property address, can lead to delays or rejection of the form.

Incorrect Borrower Name: Providing the wrong name for the borrower can cause confusion and may result in legal issues later on.

Missing Appraisal Date: Not including the date of the appraisal can create discrepancies in the timeline of the loan process.

Ignoring Communication Prohibitions: Any direct communication between the appraiser and loan production staff should be avoided. Not adhering to this can violate HVCC guidelines.

Providing Prohibited Information: Sharing details such as the owner's estimate of value or target value can compromise the integrity of the appraisal process.

Not Verifying Appraiser Qualifications: Failing to confirm that the appraiser’s license and certification status are valid can lead to issues with the appraisal’s acceptance.

Signature Issues: Omitting the authorized signature or failing to print the name and title can invalidate the certification of the appraisal.

The Appraisal HVCC form is a crucial document in the appraisal process, ensuring compliance with the Home Valuation Code of Conduct. Several other forms and documents are often utilized alongside it to facilitate the appraisal process and ensure transparency and accuracy. Below is a list of these documents, each described briefly.

Each of these documents plays a vital role in the appraisal process, contributing to a comprehensive understanding of property value and compliance with regulatory standards. Timely completion and accuracy of these forms are essential to facilitate smooth transactions and uphold the integrity of the appraisal process.

The Appraisal HVCC form shares similarities with several other important documents in the real estate and lending process. Here are four such documents:

When filling out the Appraisal HVCC form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Adhering to these guidelines will help ensure that the appraisal process remains compliant with the Home Valuation Code of Conduct (HVCC) and maintains the integrity of the appraisal itself.

Misconceptions about the Appraisal HVCC form can lead to misunderstandings regarding its purpose and function. Below are ten common misconceptions clarified for better understanding.

Understanding these misconceptions can help individuals navigate the appraisal process more effectively and ensure that their rights are protected during real estate transactions.

Here are some key takeaways about filling out and using the Appraisal HVCC form: