The Alabama 96 form serves as a crucial document for reporting annual information returns to the Alabama Department of Revenue. This form must be completed by any resident individual, corporation, association, or agent who makes payments of $1,500 or more in gains, profits, or income to taxpayers subject to Alabama income tax within a calendar year. If Alabama income tax has been withheld from these payments, it is essential to file Form 99 or an approved substitute, regardless of the payment amount. However, employers who file Form A-2 for salaries and wages paid to employees do not need to report those same payments on Form 99. Instead, they can opt to submit copies of federal Form 1099 to meet their reporting obligations. It is important to note that all information returns must cover payments made during the calendar year and should be filed with the Alabama Department of Revenue by March 15 of the following year. For those who have withheld Alabama income tax, Form A-3, the Annual Reconciliation of Alabama Income Tax Withheld, should be used instead of the Alabama 96 form. This ensures compliance and helps maintain accurate records for tax purposes.

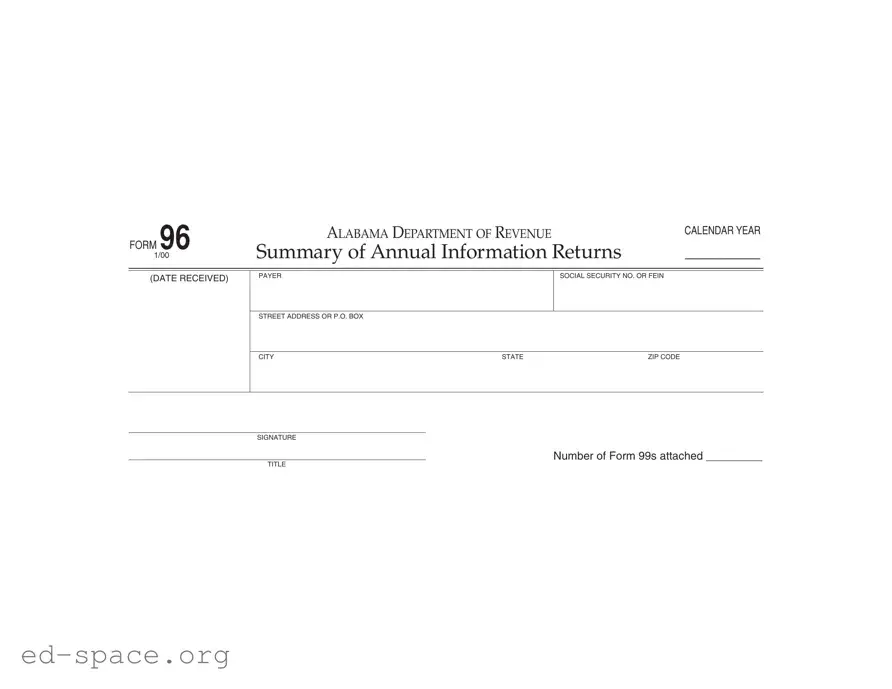

FORM 96 |

ALABAMA DEPARTMENT OF REVENUE |

CALENDAR YEAR |

|

|

|

1/00 |

Summary of Annual Information Returns |

_______________ |

(DATE RECEIVED)

PAYER

SOCIAL SECURITY NO. OR FEIN

STREET ADDRESS OR P.O. BOX

CITY |

STATE |

ZIP CODE |

SIGNATURE

NUMBER OF FORM 99S ATTACHED _________

TITLE

Instructions

Information returns on Form 99 must be filed by every resident individual, corporation, association or agent making payment of gains, profits or income (other than interest coupons payable to bearer) of $1,500.00 or more in any calendar year to any taxpayer subject to Alabama income tax. If you have voluntarily withheld Alabama income tax from such payments, you must file Form 99 or approved substitute regardless of the amount of the payment. Employers filing Form

Returns must be filed with the Alabama Department of Revenue for each calendar year on or before March 15 of the following year.

Mail to: Alabama Department of Revenue |

NOTE: IF ALABAMA INCOME TAX HAS BEEN WITHHELD ON FORM 99 |

Individual & Corporate Tax Division |

DO NOT USE THIS FORM; USE FORM |

P.O. Box 327489 |

OF ALABAMA INCOME TAX WITHHELD. |

Montgomery, AL |

|

| Fact Name | Details |

|---|---|

| Form Title | Form 96 - Summary of Annual Information Returns |

| Governing Law | Alabama Code § 40-18-70 et seq. |

| Filing Requirement | Required for payments of $1,500 or more made to taxpayers subject to Alabama income tax. |

| Filing Deadline | Forms must be submitted by March 15 of the following year. |

| Recipient Types | Includes individuals, corporations, associations, or agents making qualifying payments. |

| Withholding Tax | If Alabama income tax is withheld, Form 99 must be filed regardless of payment amount. |

| Employer Exemption | Employers filing Form A-2 for salaries and wages do not need to report those on Form 99. |

| Alternative Filing | Copies of federal Form 1099 may be submitted instead of Form 99. |

| Mailing Address | Alabama Department of Revenue, Individual & Corporate Tax Division, P.O. Box 327489, Montgomery, AL 36132-7489. |

Filling out the Alabama 96 form is an important step for those required to report certain payments made to taxpayers subject to Alabama income tax. Once you have gathered all necessary information, you can proceed with the form to ensure compliance with state requirements.

What is the Alabama 96 form?

The Alabama 96 form is a summary of annual information returns that must be filed with the Alabama Department of Revenue. It is used to report payments made to taxpayers subject to Alabama income tax, specifically when those payments are $1,500 or more in a calendar year. This form helps ensure compliance with state tax laws and provides a record of income paid to individuals or entities.

Who needs to file the Alabama 96 form?

Every resident individual, corporation, association, or agent making payments of $1,500 or more to any taxpayer subject to Alabama income tax must file this form. This includes payments for gains, profits, or income, excluding interest coupons payable to bearer. If you have withheld Alabama income tax from such payments, you are required to file Form 99 or an approved substitute, regardless of the payment amount.

When is the Alabama 96 form due?

The Alabama 96 form must be filed with the Alabama Department of Revenue on or before March 15 of the year following the calendar year in which the payments were made. Timely submission is crucial to avoid penalties and ensure compliance with state tax regulations.

What should I do if I have withheld Alabama income tax?

If Alabama income tax has been withheld on the payments reported on Form 99, do not use the Alabama 96 form. Instead, you should file Form A-3, which is the annual reconciliation of Alabama income tax withheld. This ensures that the withholding is properly accounted for and reported to the state.

Can I use federal Form 1099 instead of the Alabama 96 form?

Yes, in lieu of filing Form 99, you may submit copies of federal Form 1099 to the Alabama Department of Revenue. This option simplifies the reporting process, especially if you already file federal forms for the same payments. Ensure that the federal forms are complete and accurate to avoid any issues with state compliance.

Where do I send the Alabama 96 form?

The completed Alabama 96 form should be mailed to the Alabama Department of Revenue at the following address: Individual & Corporate Tax Division, P.O. Box 327489, Montgomery, AL 36132-7489. Make sure to check that all information is correct before sending to avoid delays or complications in processing.

Incorrect Social Security Number or FEIN: Providing an incorrect Social Security Number or Federal Employer Identification Number (FEIN) can lead to processing delays or rejections. Always double-check this information for accuracy.

Missing Signature: Failing to sign the form is a common mistake. Without a signature, the form is considered incomplete and cannot be processed.

Incorrect Address Information: Ensure that the street address, city, state, and ZIP code are all filled out correctly. An incorrect address can result in important correspondence being sent to the wrong location.

Not Reporting All Required Payments: Some individuals may overlook payments that need to be reported. Remember, any payment of $1,500 or more must be included on the form.

Missing Form 99 Attachments: If applicable, ensure that the number of Form 99s attached is filled out accurately. Not indicating the correct number can lead to confusion during processing.

Filing After the Deadline: The form must be submitted by March 15 of the following year. Late submissions can incur penalties or complications.

Using the Wrong Form: If Alabama income tax has been withheld, individuals should use Form A-3 instead of Form 96. Using the incorrect form can lead to issues with tax compliance.

Ignoring Instructions: Not reading the instructions carefully can result in mistakes. Each section of the form has specific requirements, and overlooking them can cause errors.

The Alabama 96 form is an important document used for summarizing annual information returns related to income payments in Alabama. When completing this form, you may also need to reference several other forms and documents that are commonly used in conjunction with it. Below is a list of these forms, each accompanied by a brief description to help clarify their purposes.

Understanding these forms and their purposes can simplify the process of filing taxes and ensure compliance with Alabama tax laws. Always consider consulting with a tax professional if you have questions about which forms to use or how to complete them accurately.

The Alabama 96 form is primarily used for summarizing annual information returns, specifically related to payments subject to Alabama income tax. Several other documents serve similar purposes in the realm of tax reporting and information sharing. Below are four documents that share similarities with the Alabama 96 form:

When filling out the Alabama 96 form, it’s essential to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Misconceptions about the Alabama 96 form can lead to confusion and potential errors in tax reporting. Here are eight common misconceptions clarified:

Understanding these misconceptions can help ensure compliance with Alabama tax regulations and avoid unnecessary penalties.

Filling out the Alabama 96 form is an important process for reporting annual information returns. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the process of filling out and using the Alabama 96 form with confidence.