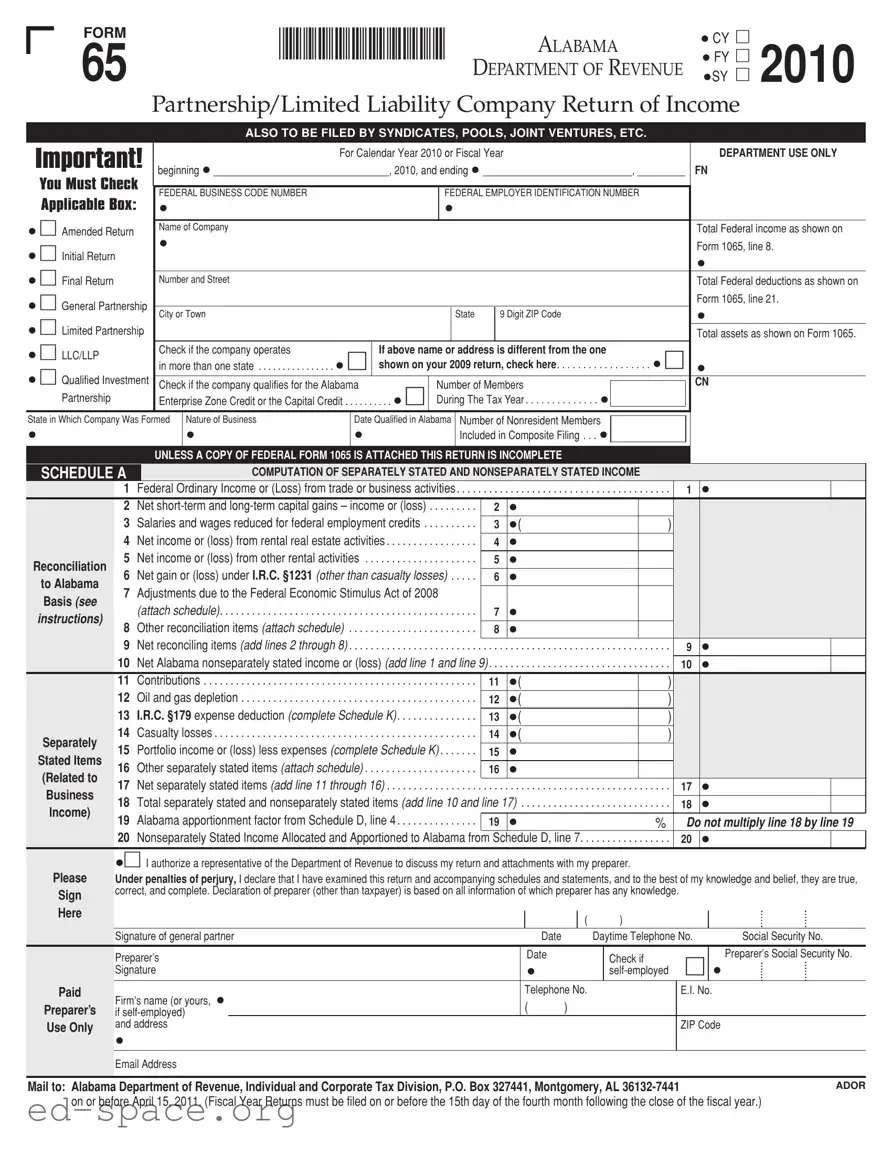

The Alabama 65 form is an essential document for partnerships and limited liability companies (LLCs) operating in Alabama. This form serves as a return of income, allowing these entities to report their financial activities to the Alabama Department of Revenue. It must be filed by various types of organizations, including syndicates, pools, and joint ventures. The form includes critical sections where companies must provide their federal business code, employer identification number, and specify whether the return is initial, amended, or final. Additionally, it requires details about the company’s total federal income, deductions, and assets as reported on the federal Form 1065. The Alabama 65 also asks for information regarding the nature of the business, the number of members, and if the company operates in more than one state. Furthermore, it contains schedules for computing separately stated and non-separately stated income, as well as apportionment factors, which are crucial for determining how much income is subject to Alabama tax. Completing this form accurately is vital, as it ensures compliance with state tax laws and can affect the overall tax liability of the entity.

FORM |

*10000165* |

ALABAMA |

|

65 |

|||

|

DEPARTMENT OF REVENUE |

• CY

• FY 2010

•SY

|

|

|

|

|

Partnership/Limited Liability Company Return of Income |

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

ALSO TO BE FILED BY SYNDICATES, POOLS, JOINT VENTURES, ETC. |

|

|

|

|

|

|

|||||||||||||||

Important! |

|

|

For Calendar Year 2010 or Fiscal Year |

|

|

|

|

|

|

|

|

|

DEPARTMENT USE ONLY |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

beginning • _________________________________, 2010, and ending • ____________________________, _________ |

FN |

|||||||||||||||||||||

|

You Must Check |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Applicable Box: |

|

|

FEDERAL BUSINESS CODE NUMBER |

|

|

|

|

FEDERAL EMPLOYER IDENTIFICATION NUMBER |

|

|

|

|

|

|

||||||||||||

|

|

|

• |

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

Amended Return |

|

|

Name of Company |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Federal income as shown on |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

• |

Initial Return |

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 1065, line 8. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

• |

Final Return |

|

|

|

Number and Street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Federal deductions as shown on |

|||

• |

General Partnership |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 1065, line 21. |

|||||

City or Town |

|

|

|

|

|

|

State |

|

9 Digit ZIP Code |

|

|

|

|

|

|

|

• |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

• |

Limited Partnership |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets as shown on Form 1065. |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

• |

LLC/LLP |

|

|

|

Check if the company operates |

|

|

If above name or address is different from the one |

|

|

|

|

|

|

|||||||||||||

|

|

|

in more than one state |

• |

|

shown on your 2009 return, check here |

|

|

. |

. . • |

|

|

|

|

|

|

|||||||||||

• |

|

|

|

|

|

. . |

. |

. . . . |

|

|

|

• |

|||||||||||||||

Qualified Investment |

Check if the company qualifies for the Alabama |

Number of Members |

|

|

|

|

|

|

|

CN |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Partnership |

|

|

|

Enterprise Zone Credit or the Capital Credit . |

. . . . . |

. . . . • |

During The Tax Year |

• |

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State in Which Company Was Formed |

Nature of Business |

|

Date Qualified in Alabama |

Number of Nonresident Members |

|

|

|

|

|

|

|

||||||||||||||||

• |

|

|

|

|

|

• |

|

• |

|

|

|

Included in Composite Filing . . . |

• |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNLESS A COPY OF FEDERAL FORM 1065 IS ATTACHED THIS RETURN IS INCOMPLETE |

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

SCHEDULE A |

|

|

|

COMPUTATION OF SEPARATELY STATED AND NONSEPARATELY STATED INCOME |

|

|

|

|

|

|

||||||||||||||||

|

|

1 |

Federal Ordinary Income or (Loss) from trade or business activities |

. . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . |

. |

1 |

|

• |

|

|||||||||||||||

|

|

2 |

Net |

. . |

. . |

. |

. . . . |

|

2 |

• |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

3 |

.Salaries and wages reduced for federal employment credits |

. . |

. . |

. |

. . . . |

|

3 |

•( |

|

|

|

|

) |

|

|

|

|

|

|||||||

|

|

4 |

. . . . . . . .Net income or (loss) from rental real estate activities |

. . |

. . |

. |

. . . . |

|

4 |

• |

|

|

|

|

|

|

|

|

|

|

|||||||

Reconciliation |

5 |

. . . . . . . . . . . .Net income or (loss) from other rental activities |

. . |

. . |

. |

. . . . |

|

5 |

• |

|

|

|

|

|

|

|

|

|

|

||||||||

6 |

Net gain or (loss) under I.R.C. §1231 (other than casualty losses) |

|

|

6 |

• |

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

to Alabama |

. . . . |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

7 |

Adjustments due to the Federal Economic Stimulus Act of 2008 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Basis (see |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

(attach schedule) |

|

|

|

|

|

|

|

|

7 |

• |

|

|

|

|

|

|

|

|

|

|

|||||

|

instructions) |

|

. . . . |

. . . . . . . . . . |

. . |

. . |

. |

. . . . |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

8 |

Other reconciliation items (attach schedule) |

|

|

|

|

|

|

|

8 |

• |

|

|

|

|

|

|

|

|

|

|

||||||

|

|

. . . . |

. . . . . . . . . . |

. . |

. . |

. |

. . . . |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

9 |

.Net reconciling items (add lines 2 through 8) |

. . . . |

. . . . . . . . . . |

. . |

. . |

. |

. . . . . |

. |

. . |

. . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . |

. |

9 |

|

• |

|

|||||||

|

|

10 |

Net Alabama nonseparately stated income or (loss) (add line 1 and line 9) |

. . |

. . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . |

. |

10 |

|

• |

|

||||||||||||||

|

|

11 |

Contributions |

. . . . |

. . . . . . . . . . |

. . |

. . |

. |

. . . . |

|

11 |

•( |

|

|

|

|

) |

|

|

|

|

|

|||||

|

|

12 |

. . . . . . . . . . . . . . . . . . . . .Oil and gas depletion |

. . . . |

. . . . . . . . . . |

. . |

. . |

. |

. . . . |

|

12 |

•( |

|

|

|

|

) |

|

|

|

|

|

|||||

|

|

13 |

. . . . . .I.R.C. §179 expense deduction (complete Schedule K) |

. . |

. . |

. |

. . . . |

|

13 |

•( |

|

|

|

|

) |

|

|

|

|

|

|||||||

|

Separately |

14 |

. . . . . . . . . . . . . . . . . . . . . . . . . .Casualty losses |

. . . . |

. . . . . . . . . . |

. . |

. . |

. |

. . . . |

|

14 |

•( |

|

|

|

|

) |

|

|

|

|

|

|||||

|

15 |

Portfolio income or (loss) less expenses (complete Schedule K) |

|

|

15 |

• |

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Stated Items |

. . . . |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

16 |

Other separately stated items (attach schedule) |

|

|

|

|

|

16 |

• |

|

|

|

|

|

|

|

|

|

|

||||||||

|

(Related to |

. . |

. . |

. |

. . . . |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Business |

17 |

. . . . . . . .Net separately stated items (add line 11 through 16) |

. . |

. . |

. |

. . . . . |

. |

. . |

. . |

. . . . . . . . . . . . . . . . . . . |

. . . . . |

. . . . . |

. |

17 |

|

• |

|

|||||||||

|

18 |

Total separately stated and nonseparately stated items (add line 10 and line 17) |

|

|

|

|

|

18 |

|

• |

|

||||||||||||||||

|

Income) |

. . . . . |

. . . . . |

. |

|

|

|||||||||||||||||||||

|

19 |

Alabama apportionment factor from Schedule D, line 4 |

|

|

|

|

|

19 |

• |

% |

|

|

Do not multiply line 18 by line 19 |

||||||||||||||

|

|

. . |

. . |

. |

. . . . |

|

|

|

|||||||||||||||||||

|

|

20 |

Nonseparately Stated Income Allocated and Apportioned to Alabama from Schedule D, line 7 |

. . . . . |

. . . . . |

. |

20 |

|

• |

|

|||||||||||||||||

•I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Please

Sign

Here

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

|

|

( |

) |

|

Signature of general partner |

Date |

Daytime Telephone No. |

Social Security No. |

|

|

Preparer’s |

|

|

Signature |

|

Paid |

Firm’s name (or yours, • |

|

Preparer’s |

||

if |

||

Use Only |

and address |

|

|

||

|

• |

Date |

Check if |

|

Preparer’s Social Security No. |

|

|

|

|

• |

|

• |

|

Telephone No. |

|

E.I. No. |

|

()

ZIP Code

Email Address

Mail to: Alabama Department of Revenue, Individual and Corporate Tax Division, P.O. Box 327441, Montgomery, AL |

ADOR |

on or before April 15, 2011. (Fiscal Year Returns must be filed on or before the 15th day of the fourth month following the close of the fiscal year.) |

|

|

|

|

*10000265* |

|

Form 65 — 2010 |

Page 2 |

|

|

|

|

|

SCHEDULE B |

|

ALLOCATION OF NONBUSINESS INCOME, LOSS, AND EXPENSE |

|

Identify by account name and amount all items of nonbusiness income, loss, and expense removed from apportionable income and those items which are directly allocable to Alabama. Adjustment(s) must also be made for any proration of expens- es under Alabama Income Tax Rule

deduction that is applicable to both business and nonbusiness income of the tax- payer shall be prorated to each class of income in determining income subject to tax as provided…” (See instructions).

|

DIRECTLY ALLOCABLE ITEMS |

|

ALLOCABLE GROSS INCOME / LOSS |

|

|

|

RELATED EXPENSE |

|

NET OF RELATED EXPENSE |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Column A |

|

Column B |

|

|

Column C |

|

Column D |

|

Column E |

|

Column F |

|||

|

|

|

|

Everywhere |

|

Alabama |

|

|

Everywhere |

|

Alabama |

|

Everywhere |

|

Alabama |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Col. A less Col. C) |

(Col. B less Col. D) |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Nonseparately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1c |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1d Total (add lines 1a, 1b, and 1c) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|||

Separately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1e |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1f |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1g |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1h Total (add lines 1e, 1f, and 1g) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE C |

|

|

APPORTIONMENT FACTOR SCHEDULE – Do not complete if the entity operates exclusively in Alabama. |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

TANGIBLE PROPERTY AT COST FOR |

|

|

ALABAMA |

|

|

|

|

|

EVERYWHERE |

||||||||

|

PRODUCTION OF BUSINESS INCOME |

BEGINNING OF YEAR |

|

END OF YEAR |

|

BEGINNING OF YEAR |

|

END OF YEAR |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1 |

Inventories |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

2 |

Land |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

3 |

Furniture and fixtures |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

4 |

Machinery and equipment |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

5 |

Buildings and leasehold improvements |

• |

|

|

|

|

|

|

|

|

|

|

|

|

||||

6 |

IDB/IRB property (at cost) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

7 |

Government property (at FMV) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

8 |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

9 |

Less Construction in progress (if included) |

• |

|

|

|

|

|

|

|

|

|

|

|

|

||||

10 |

Totals |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||

11 |

Average owned property (BOY + EOY ÷ 2) |

|

|

|

• |

|

|

|

|

|

|

|

• |

|

||||

12 |

Annual rental expense |

|

|

• |

x8 = |

|

|

|

|

|

|

x8 = |

|

|

||||

13 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total average property (add line 11 and line 12) |

|

13a |

• |

|

|

|

. . . . . . |

. . . . |

. . . . . . . . . . . . |

13b |

• |

|

|||||

14 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Alabama property factor — 13a ÷ 13b = line 14 |

. |

. . . . . . |

. . . . . . |

. . . . . . . . . . . |

. . . . . . . |

. . . . . |

. . . . . . . |

. . . . |

. . . . . . . . . . . . |

14 |

• |

% |

|||||

|

SALARIES, WAGES, COMMISSIONS AND OTHER COMPENSATION |

|

|

15a |

ALABAMA |

|

15b |

EVERYWHERE |

15c |

|

||||||||

|

RELATED TO THE PRODUCTION OF BUSINESS INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

15 |

Alabama payroll factor — 15a ÷ 15b = 15c |

. |

. . . . . |

• |

|

|

|

|

|

|

|

|

% |

|||||

|

|

|

|

SALES |

|

|

|

|

ALABAMA |

|

|

EVERYWHERE |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 |

Destination sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

17 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Origin sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

18 |

. .Total gross receipts from sales |

. . . . . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

19 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Dividends |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

20 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Interest |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

21 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Rents |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

22 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Royalties |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

23 |

. . . . . . .Gross proceeds from capital and ordinary gains |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||||

24Other •____________________________________ (Federal 1065, line •_____ ) •

25 |

Alabama sales factor — 25a ÷ 25b = line 25c |

25a • |

25b |

|

25c |

% |

26 |

Sum of lines 14, 15c, and 25c ÷ 3 = ALABAMA APPORTIONMENT FACTOR (Enter here and on line 4, Schedule D, page 3) |

26 |

• |

% |

||

ADOR

| Fact Name | Description |

|---|---|

| Purpose of Form | The Alabama 65 form is used by partnerships and limited liability companies to report income, deductions, and credits for the tax year. It is also applicable for syndicates, pools, and joint ventures. |

| Filing Requirements | This form must be filed for the calendar year 2010 or the fiscal year that begins in 2010. It is essential to file on or before April 15, 2011, or the 15th day of the fourth month following the close of the fiscal year. |

| Attachments Needed | To ensure completeness, a copy of the Federal Form 1065 must be attached. Without it, the return is considered incomplete. |

| Governing Laws | The Alabama 65 form is governed by the Alabama Code, specifically under Title 40, Chapter 18, which outlines the state's income tax regulations for partnerships and LLCs. |

Filling out the Alabama 65 form is a crucial step for partnerships and limited liability companies to report their income accurately. After completing the form, it must be submitted to the Alabama Department of Revenue by the specified deadline to avoid penalties. Make sure to have all necessary documents on hand, such as federal Form 1065, to ensure a smooth filing process.

What is the Alabama 65 form?

The Alabama 65 form is a tax return specifically designed for partnerships, limited liability companies (LLCs), and similar entities operating in Alabama. It is used to report income, deductions, and other relevant financial information for the calendar year or fiscal year. This form must be filed by various business structures, including syndicates, pools, and joint ventures. It is essential for compliance with Alabama tax regulations.

Who needs to file the Alabama 65 form?

Any partnership or limited liability company that operates in Alabama must file the Alabama 65 form. This includes general partnerships, limited partnerships, LLCs, and LLPs. If the entity operates in multiple states, it is still required to file this form. Additionally, if the entity is part of a composite filing that includes nonresident members, it must also complete the Alabama 65 form.

What information is required on the Alabama 65 form?

The Alabama 65 form requires several pieces of information, including the name of the company, its address, and its federal employer identification number (EIN). It also asks for total federal income, deductions, and assets as reported on federal Form 1065. Furthermore, details about the nature of the business, the number of members, and any credits the company qualifies for must be provided. A copy of federal Form 1065 must be attached for the return to be considered complete.

What are the deadlines for filing the Alabama 65 form?

The deadline for filing the Alabama 65 form is typically April 15 of the following year for calendar year filers. For entities on a fiscal year, the form must be filed on or before the 15th day of the fourth month after the close of the fiscal year. It is important to adhere to these deadlines to avoid penalties and interest on unpaid taxes.

What happens if the Alabama 65 form is filed late?

If the Alabama 65 form is filed late, the entity may incur penalties and interest on any unpaid taxes. The penalties can vary based on how late the form is submitted. It is advisable to file the return as soon as possible to minimize potential penalties. If there are extenuating circumstances, the entity may consider reaching out to the Alabama Department of Revenue for guidance on possible relief options.

Can the Alabama 65 form be amended?

Yes, the Alabama 65 form can be amended if there are errors or omissions in the original filing. To amend the form, the entity must check the box indicating that it is an amended return and provide the corrected information. It is important to file the amended return as soon as the errors are discovered to ensure compliance and avoid further penalties.

Incomplete Information: One common mistake is failing to provide complete information. Each section of the Alabama 65 form must be filled out thoroughly. Missing details can lead to delays or rejections.

Incorrect Federal Identification Numbers: People often enter incorrect federal employer identification numbers (FEINs). This error can cause significant issues, as the form is linked to federal records.

Failure to Check Applicable Boxes: It’s essential to check the appropriate boxes, such as whether the return is an amended, initial, or final return. Neglecting this step can lead to confusion about the filing status.

Not Including Required Attachments: The form explicitly states that a copy of the federal Form 1065 must be attached. Omitting this document renders the return incomplete.

Misreporting Income or Deductions: Errors in reporting federal income and deductions can lead to incorrect calculations. It’s crucial to ensure that these figures match those on the federal return.

Ignoring Multi-State Operations: If the business operates in multiple states, this must be indicated on the form. Failing to do so can result in inaccurate apportionment of income.

Signing and Dating the Form: Lastly, individuals often forget to sign and date the return. This step is necessary to validate the submission and confirm its accuracy.

The Alabama 65 form is an important document for partnerships and limited liability companies in Alabama. It is used to report income, deductions, and credits for state tax purposes. Along with the Alabama 65 form, several other documents are often required to ensure compliance with state tax regulations. Below is a list of these forms and a brief description of each.

Each of these forms plays a crucial role in ensuring that partnerships and limited liability companies comply with Alabama tax laws. Properly completing and submitting these documents can help avoid penalties and ensure accurate tax reporting.

The Alabama 65 form is primarily used for the reporting of income by partnerships and limited liability companies. There are several other documents that serve similar purposes in various contexts. Here’s a list of seven such documents, along with explanations of their similarities to the Alabama 65 form:

When filling out the Alabama 65 form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are seven things to do and not to do:

By adhering to these guidelines, you can help ensure a smoother filing process for your Alabama 65 form. Attention to detail is crucial, and taking the time to follow these steps can prevent future complications.

Misconceptions about the Alabama 65 form can lead to confusion and potential errors in filing. Here are nine common misconceptions, along with clarifications for each.

Understanding these misconceptions can help ensure accurate and timely filing of the Alabama 65 form, reducing the risk of complications with the Alabama Department of Revenue.

When dealing with the Alabama 65 form, there are several important considerations to keep in mind. Here are some key takeaways:

These takeaways highlight the importance of careful preparation and attention to detail when filling out the Alabama 65 form. Ensuring compliance with these guidelines can help facilitate a smoother filing process.