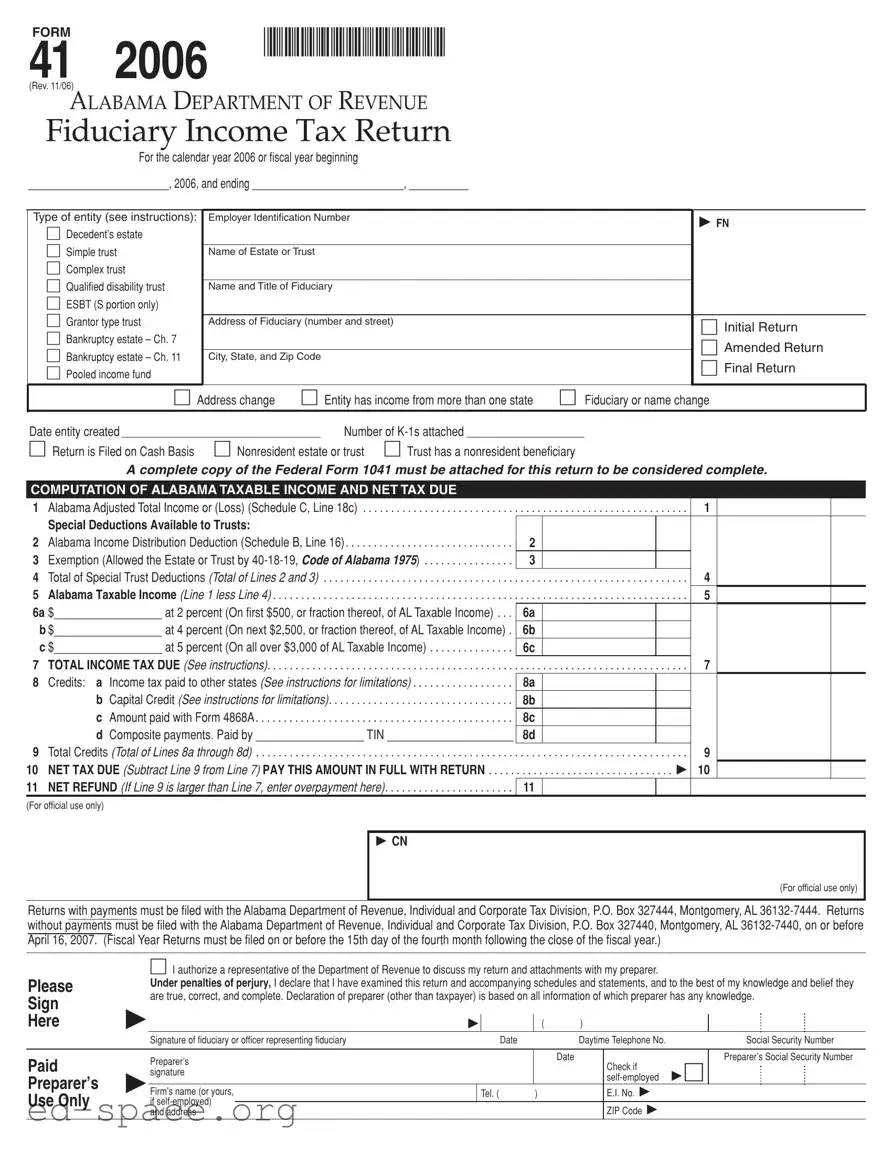

The Alabama 41 form, officially known as the Fiduciary Income Tax Return, serves as a critical tool for estates and trusts operating within the state. This form is essential for reporting income earned by a decedent's estate, simple trust, complex trust, qualified disability trust, and other fiduciary entities for the calendar year 2006 or any fiscal year that begins in 2006. It requires detailed information, including the type of entity, employer identification number, and the fiduciary's name and address. Taxpayers must indicate whether this is an initial, amended, or final return, and they must also disclose any changes in address or fiduciary status. The form includes a comprehensive computation section to determine Alabama taxable income, special deductions available to trusts, and the net tax due. Additionally, it mandates the attachment of a complete copy of the Federal Form 1041, ensuring that all income and deductions are accurately reflected. Understanding the nuances of the Alabama 41 form is vital for fiduciaries to navigate their tax obligations effectively and avoid potential pitfalls.

FORM |

|

*0612830141* |

41 |

2006 |

(Rev. 11/06)

ALABAMA DEPARTMENT OF REVENUE

Fiduciary Income Tax Return

For the calendar year 2006 or fiscal year beginning

__________________________, 2006, and ending ____________________________, ___________

Type of entity (see instructions): Decedent’s estate

Simple trust

Complex trust

Qualified disability trust

ESBT (S portion only)

Grantor type trust

Bankruptcy estate – Ch. 7

Bankruptcy estate – Ch. 11

Pooled income fund

Employer Identification Number

Name of Estate or Trust

Name and Title of Fiduciary

Address of Fiduciary (number and street)

City, State, and Zip Code

FN

Initial Return

Amended Return

Final Return

|

|

Address change |

Entity has income from more than one state |

Fiduciary or name change |

||||

|

|

|

|

|

|

|

|

|

Date entity created |

|

|

|

Number of |

|

|

|

|

Return is Filed on Cash Basis |

|

Nonresident estate or trust |

Trust has a nonresident beneficiary |

|

|

|||

A complete copy of the Federal Form 1041 must be attached for this return to be considered complete.

COMPUTATION OF ALABAMA TAXABLE INCOME AND NET TAX DUE |

|

|

1 |

Alabama Adjusted Total Income or (Loss) (Schedule C, Line 18c) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 |

|

Special Deductions Available to Trusts: |

|

2 |

Alabama Income Distribution Deduction (Schedule B, Line 16) |

2 |

3 |

Exemption (Allowed the Estate or Trust by |

3 |

4 |

Total of Special Trust Deductions (Total of Lines 2 and 3) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 |

5 |

Alabama Taxable Income (Line 1 less Line 4) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 |

6a |

$__________________ at 2 percent (On first $500, or fraction thereof, of AL Taxable Income) . . . |

6A |

b$__________________ at 4 percent (On next $2,500, or fraction thereof, of AL Taxable Income) . 6B |

||

c $__________________ at 5 percent (On all over $3,000 of AL Taxable Income) |

6C |

|

7 |

TOTAL INCOME TAX DUE (See instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 |

8 |

Credits: a Income tax paid to other states (See instructions for limitations) |

8A |

|

b Capital Credit (See instructions for limitations) |

8B |

|

c Amount paid with Form 4868A |

8C |

|

d Composite payments. Paid by __________________ TIN _____________________ |

8D |

9 |

Total Credits (Total of Lines 8a through 8d) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 |

10 |

NET TAX DUE (Subtract Line 9 from Line 7) PAY THIS AMOUNT IN FULL WITH RETURN |

. . . . . . . . . . . . . . . . . . . . . . . . . . . 10 |

11 |

NET REFUND (If Line 9 is larger than Line 7, enter overpayment here) |

11 |

(For official use only) |

|

|

|

CN |

|

(For official use only)

Returns with payments must be filed with the Alabama Department of Revenue, Individual and Corporate Tax Division, P.O. Box 327444, Montgomery, AL

Please

Sign

Here

I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

( )

Signature of fiduciary or officer representing fiduciary |

Date |

Daytime Telephone No. |

Social Security Number |

Paid

Preparer’s

Use Only

Preparer’s signature

Firm’s name (or yours, if

|

|

Date |

|

Preparer’s Social Security Number |

|

|

|

Check if |

|

|

|

|

|

|

|

Tel. ( |

) |

E.I. No. |

|

|

|

|

|

|

|

|

|

ZIP Code |

|

|

|

|

|

|

FORM |

*0612830241* |

|

41 2006 |

Alabama Fiduciary Income Tax Return |

PAGE 2

Name of estate or trust

Employer identification number

Name and title of fiduciary

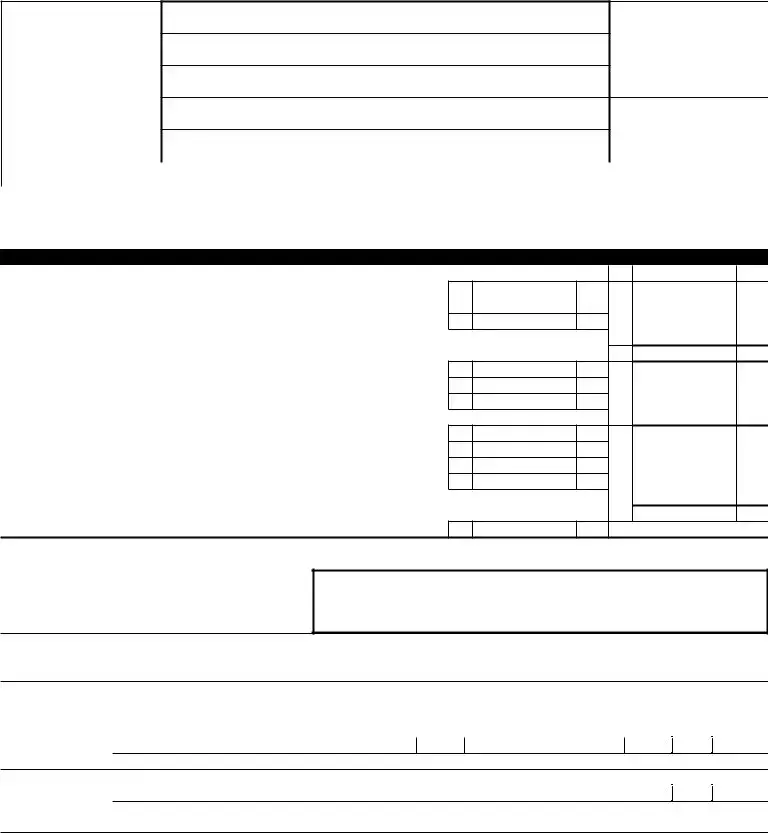

SCHEDULE A – ALABAMA CHARITABLE DEDUCTION. Do not complete for a simple trust or a pooled income fund. |

||

|

|

1 |

1 |

Amounts paid or permanently set aside for charitable purposes from gross income |

|

|

|

2 |

2 |

Alabama |

|

|

|

3 |

3 |

Subtract line 2 from line1 |

|

|

|

4 |

4 |

Capital gains for the tax year allocated to corpus and paid or permanently set aside for charitable purposes |

|

|

|

5 |

5 |

Alabama Charitable Deduction.Add Line 3 and Line 4. Enter total here and on Page 3, Schedule C, Line 13, Column C |

|

SCHEDULE B – COMPUTATION OF ALABAMA INCOME DISTRIBUTION DEDUCTION |

|

|

|

|

1 |

1 |

Alabama Adjusted Total Income (Page 1, Lne 1) |

|

2The amount of gain from the sale of capital assets, but only if the gain was allocated to corpus and not paid, credited,

|

2 |

or required to be distributed to any beneficiary during the taxable year or not included in Line 4, Schedule A (see instructions) |

|

|

3 |

3 Subtract the amount entered on Line 2 from the amount entered on Line 1, and enter in Line 3 |

|

4The amount of loss from the sale of capital assets – entered as a positive number, only if the loss was not considered

|

in the determination of the amount to be paid, credited, or required to be distributed to any beneficiary during taxable year |

4 |

5 |

Amount of tax exempt interest income excluded in computing Alabama taxable income |

5 |

6 |

Other adjustments – see instructions |

6 |

7 |

Alabama Distributable Net Income (Sum of Lines 3 through 6) |

7 |

8If a complex trust, enter accounting income for the tax year as determined under the

|

governing instrument and applicable local law |

8 |

|

|

|

|

|

|

|

|

|

9 Income required to be distributed currently |

9 |

||

|

|

|

|

10 |

Other amounts paid, credited, or otherwise required to be distributed |

10 |

|

|

|

|

|

11 |

Total distributions. add Lines 9 and 10 |

11 |

|

|

|

|

|

12 |

Enter the amount of |

12 |

|

|

|

|

|

13 |

Tentative income distribution deduction. Subtract Line 12 from Line 11 |

13 |

|

|

|

|

|

14 |

Tentative income distribution deduction. Subtract Line 5 from Line 7. If zero or less, enter |

14 |

|

|

|

|

|

15 |

Special Alabama Income Distribution Deduction (see instructions for applicability of the special limitation) |

15 |

|

16Alabama Income Distribution Deduction. Enter the smallest of Line 13, Line 14, or, if applicable, Line 15,

on this line and on Page 1, Line 2. (Do not enter less than zero.) |

16 |

CHANGE IN ALABAMA TAX LAW

CONCERNING ESTATES AND TRUSTS

The Alabama Legislature passed the Subchapter J and Business Trust Conformity Act (Act Number

At the time the 2006 Form 41 was being developed, the promulgation process had begun for the regulations to implement the Act.

FORM |

*0612830341* |

|

41 2006 |

Alabama Fiduciary Income Tax Return |

PAGE 3

Name of estate or trust

Employer identification number

Name and title of fiduciary

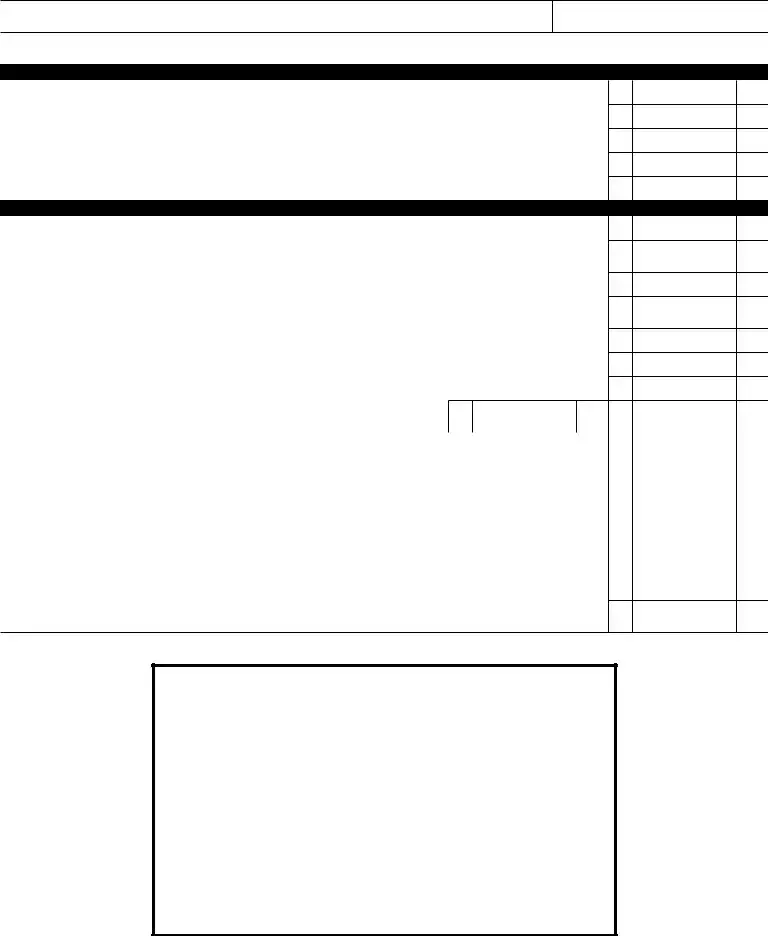

SCHEDULE C – COMPUTATION OF ALABAMA ADJUSTED TOTAL INCOME

|

|

|

Column A |

|

|

Column B |

|

Column C |

|||

|

|

|

AS REPORTED ON |

|

|

ALABAMA |

|

ALABAMA AMOUNT |

|||

|

|

|

FEDERAL FORM 1041 |

|

|

ADJUSTMENTS |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Interest income |

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Ordinary dividends |

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Business income or (loss) |

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Capital gain or loss (see instructions) |

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Rents, royalties, partnerships, and other estates and trusts |

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

6 |

Farm income or (loss) |

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Ordinary gain or (loss) from Form 4797 |

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

8 |

Other income |

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

9 |

Total Income (Sum of Lines 1 through 8) |

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Ordinary Deductions: |

|

|

|

|

|

|

|

|

|

|

10 |

Interest |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Taxes (include federal estate and income taxes) |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

12 |

Fiduciary fees |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

13 |

Charitable deduction |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

14 |

Attorney, accountant, and return preparer fees |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

15 |

Other deductions not subject to the 2% floor |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

16 |

Allowable miscellaneous itemized deductions subject to the 2% floor . . |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

17 |

Total Ordinary Deductions (Sum of Lines 10 through 16) |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

18a |

Federal Adjusted Total Income (Line 9 less Line 17 – the amount |

|

|

|

|

|

|

|

|

|

|

|

entered on this line in Column A must equal the amount entered on |

|

|

|

|

|

|

|

|

|

|

|

Page 1, Line 17, Form 1041) |

18A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18b |

Net Alabama Adjustments (Column B, Line 9 less Line 17) |

|

|

|

18B |

|

|

|

|

|

|

. . . . . |

. . . . . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

|

||

18c |

Alabama Adjusted Total Income (Column C, Line 9 less Line 17). Enter here and on Page 1, Line 1 |

|

|

|

|

18C |

|

|

|||

. . . . |

. |

. . . . . . . . . . . . . . . . . . . . |

|

|

|

|

|||||

19 Alabama Tax Exempt Income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

19

Attach a complete explanation, showing all computations, for each item of income or deduction included in Column B (Alabama Adjustments), include also a complete explanation and computation for the items of exempt income. See instructions.

FORM |

*0612830441* |

|

41 2006 |

Alabama Fiduciary Income Tax Return |

PAGE 4

Name of estate or trust

Employer identification number

Name and title of fiduciary

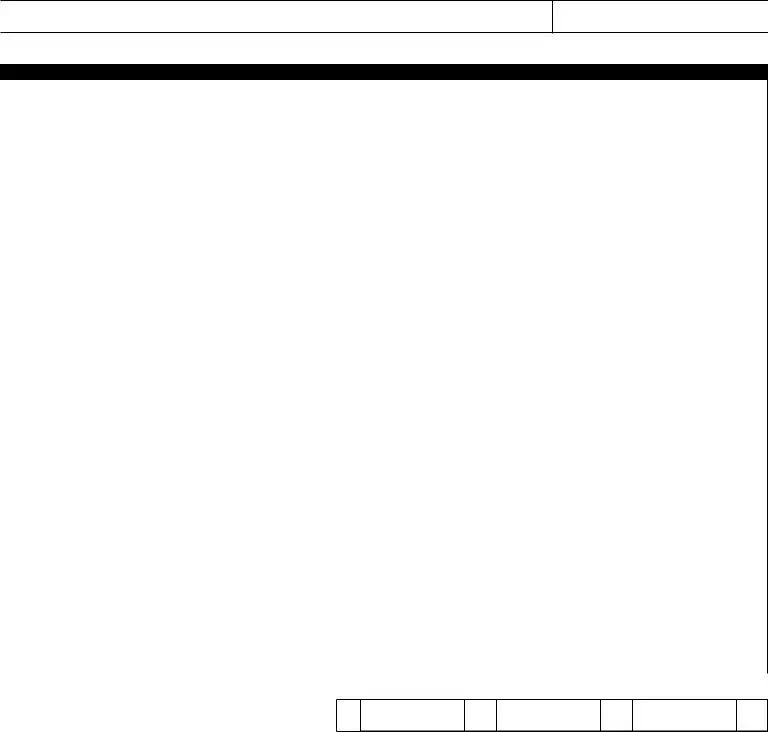

SCHEDULE K – SUMMARY OF

TOTAL ALABAMA AMOUNT

1 Interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2 Total dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2

3 Business income or (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

4 Net Alabama capital gain or loss (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

5 Rents, royalties, partnerships, and other estates and trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5

6 Farm income or (loss) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6

7 Ordinary gain or (loss) from Form 4797 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7

8 Other income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8

9 Alabama Tax Exempt Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9

10a Grantor Trust Income (Resident Beneficiaries Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10A

10b Grantor trust Deductions (Resident Beneficiaries Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10B

10c Net Grantor Trust Income (Resident Beneficiaries Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10C

11 Nonresident Beneficiary – Alabama Source Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11

12 Nonresident Beneficiary –

12

Directly apportioned deductions:

13a Depreciation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13A

13b Depletion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13B

13c Amortization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13C

Schedule K is a summary of the information reported on the

CHARACTER OF INCOME – In accordance with

ALLOCATION OF THE ALABAMA INCOME DISTRIBUTION DEDUCTION – The amount entered in Page 1, Line 2 (Alabama Income Distribution Deduction) must be allocated to resident beneficiaries and owners, so that the income reported by the beneficiaries or owners will retain its character . Generally the allocation is completed in accordance with Internal Revenue Code §§652 and 662. No amount may be included in the Alabama Income Distribution Deduction which is not included in the gross income of the estate or trust. See the instructions for more guidance concerning the allocation of income to the beneficiaries and owners.

| Fact Name | Description |

|---|---|

| Form Title | The form is officially titled the Alabama Fiduciary Income Tax Return. |

| Governing Law | The form is governed by the Code of Alabama 1975, specifically §40-18-19 and §40-18-25(b). |

| Form Revision Date | This version of the form was revised in November 2006. |

| Filing Deadline | Returns must be filed by April 16, 2007, for calendar year filers. |

| Required Attachments | A complete copy of the Federal Form 1041 must be attached for the return to be considered complete. |

| Entity Types | Entities that can use this form include decedent's estates, simple trusts, complex trusts, and more. |

| Tax Calculation | The form includes a section for computing Alabama taxable income and net tax due. |

| Income Distribution Deduction | The form allows for an Alabama Income Distribution Deduction, which is calculated based on specific criteria. |

| Charitable Deductions | There is a section for reporting Alabama charitable deductions, applicable to certain trusts. |

| Changes in Law | The form reflects changes from the Subchapter J and Business Trust Conformity Act, effective retroactively from 2004. |

Completing the Alabama 41 form requires attention to detail and accurate reporting of financial information related to the fiduciary income tax return. After gathering all necessary documents, including a complete copy of the Federal Form 1041, follow these steps to ensure the form is filled out correctly.

After completing the form, review it for any errors or omissions. Ensure that all required attachments, including the Federal Form 1041, are included. Then, submit the return to the appropriate address based on whether a payment is included or not. Timely filing is essential to avoid penalties.

What is the Alabama 41 form?

The Alabama 41 form is the Fiduciary Income Tax Return used for reporting income for estates and trusts in Alabama. It is required for entities such as decedent’s estates, simple trusts, complex trusts, and others. The form must be filed for the calendar year or a fiscal year as indicated on the return.

Who needs to file the Alabama 41 form?

What information is required to complete the form?

To complete the Alabama 41 form, you will need the Employer Identification Number (EIN), the name and title of the fiduciary, and the address of the fiduciary. Additionally, you must provide details about the type of entity, the income earned, any deductions, and whether the return is an initial, amended, or final submission. A complete copy of the Federal Form 1041 must also be attached.

What are the deadlines for filing the Alabama 41 form?

The Alabama 41 form must be filed by April 16 of the year following the tax year for calendar year filers. For fiscal year filers, the return is due on or before the 15th day of the fourth month following the close of the fiscal year. Returns with payments must be sent to a specific address, while those without payments go to a different address.

What deductions are available on the Alabama 41 form?

Several deductions may be available on the Alabama 41 form, including the Alabama Income Distribution Deduction and exemptions allowed under Alabama law. Special deductions for charitable contributions may also apply, but they are not applicable for simple trusts or pooled income funds. It is important to review the instructions to determine eligibility for each deduction.

How is the Alabama taxable income calculated?

To calculate Alabama taxable income, begin with the Alabama Adjusted Total Income. From this amount, subtract any special deductions available to the trust or estate. The resulting figure represents the Alabama taxable income. The tax due is then calculated based on the taxable income brackets established by Alabama law.

What should I do if I need to amend my Alabama 41 form?

If an amendment is necessary, you must indicate this by checking the appropriate box on the form. An amended return should include all corrected information and any additional documentation required. It is essential to ensure that the amended return is filed by the deadline to avoid penalties.

Where can I find additional resources or assistance regarding the Alabama 41 form?

For more information, individuals can visit the Alabama Department of Revenue's website. The site provides up-to-date information, instructions, and resources related to the Alabama 41 form and fiduciary income tax matters. Additionally, consulting with a tax professional may provide further guidance.

Incorrect Entity Type Selection: Selecting the wrong type of entity can lead to significant issues. Ensure you choose between decedent's estate, simple trust, complex trust, or other options correctly.

Missing Employer Identification Number (EIN): Failing to provide a valid EIN is a common mistake. This number is crucial for processing your return.

Omitting Required Attachments: Not attaching a complete copy of the Federal Form 1041 can result in your return being deemed incomplete. Always double-check that all necessary documents are included.

Errors in Income Calculation: Miscalculating Alabama Adjusted Total Income or failing to accurately report income from various sources can lead to incorrect tax amounts. Review your calculations thoroughly.

Ignoring Special Deductions: Many filers overlook special deductions available to trusts. Familiarize yourself with these deductions to minimize your taxable income.

Neglecting to Sign the Return: Not signing the return is a frequent oversight. Ensure that the fiduciary or officer representing the fiduciary has signed and dated the form.

Incorrect Filing Address: Sending the return to the wrong address can cause delays. Confirm that you are mailing it to the correct location based on whether payment is included.

When dealing with the Alabama 41 form, which is the Fiduciary Income Tax Return, there are several other documents and forms that may be necessary to complete the tax filing process effectively. Each of these forms serves a specific purpose and helps ensure that the fiduciary or estate complies with Alabama tax regulations. Below is a list of commonly used forms alongside the Alabama 41 form.

Understanding these additional forms can help streamline the tax filing process for estates and trusts in Alabama. Proper documentation ensures compliance and can prevent potential issues with the Alabama Department of Revenue. Always consider consulting with a tax professional to navigate these requirements effectively.

The Alabama 41 form, officially known as the Fiduciary Income Tax Return, shares similarities with several other tax documents that serve specific purposes for various entities. Here are eight documents that are comparable to the Alabama 41 form, along with explanations of how they are alike:

When filling out the Alabama 41 form, it's important to follow specific guidelines to ensure accuracy and compliance. Here are seven things to do and avoid:

Misconception 1: The Alabama 41 form is only for simple trusts.

This is incorrect. The form is designed for various types of entities, including decedent’s estates, complex trusts, and qualified disability trusts, among others. Each entity type has specific requirements and deductions.

Misconception 2: You do not need to attach the Federal Form 1041.

In fact, a complete copy of the Federal Form 1041 must be attached for the Alabama 41 form to be considered complete. This requirement is crucial for accurate processing and compliance.

Misconception 3: The Alabama 41 form can be filed anytime without penalties.

This is misleading. The form must be filed by April 16, 2007, for the 2006 tax year. Late filings may incur penalties, so timely submission is essential.

Misconception 4: Only estates with Alabama residents need to file the Alabama 41 form.

This is false. Nonresident estates or trusts with Alabama source income must also file the form. The residency status of beneficiaries does not exempt an estate or trust from filing obligations.

When filling out and using the Alabama 41 form, here are some key takeaways to keep in mind:

By following these guidelines, you can navigate the Alabama 41 form more effectively and ensure compliance with state tax regulations.