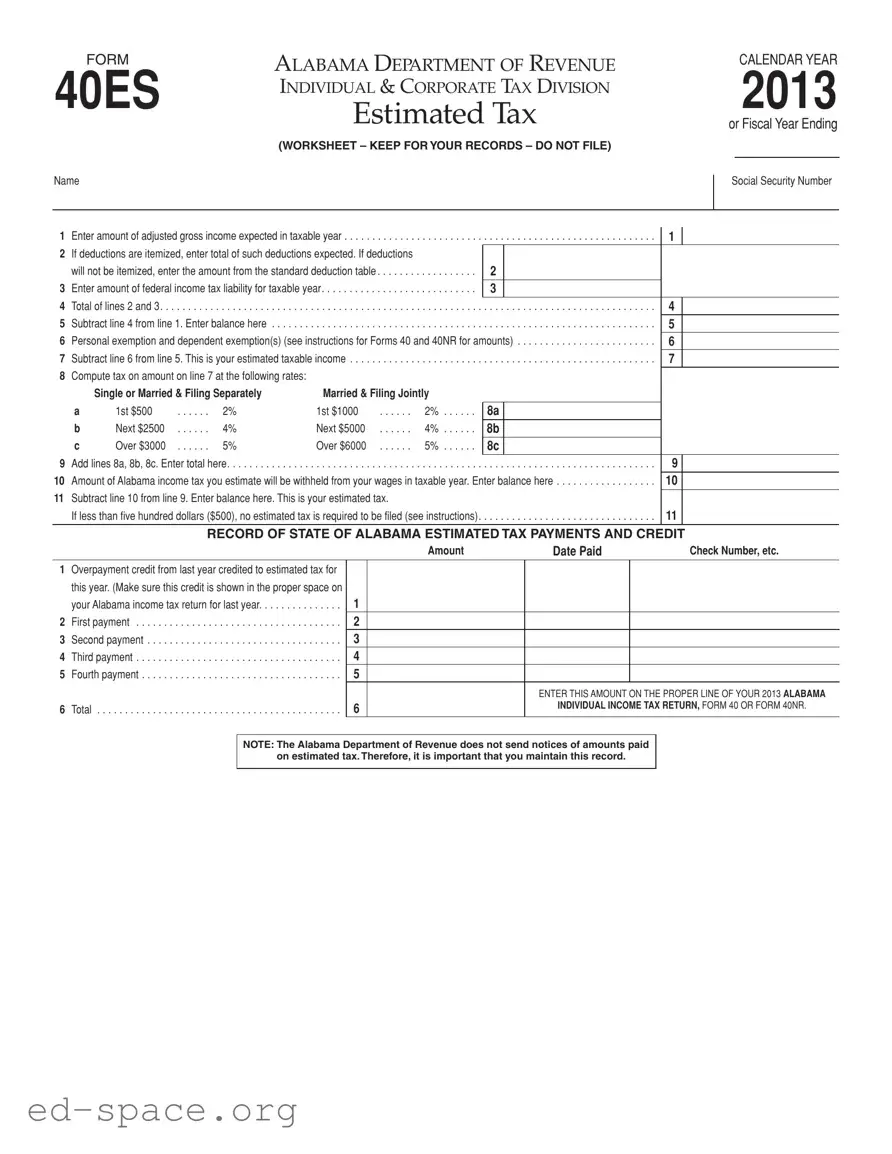

The Alabama 40ES form is an important document for individuals and corporations who need to estimate their tax obligations for the year. This form is specifically designed for those who expect to owe at least $500 in taxes after accounting for any withholding and credits. It serves as a worksheet to help taxpayers calculate their expected adjusted gross income, itemized deductions, and federal tax liability. By completing the 40ES, individuals can determine their estimated taxable income and the amount of Alabama income tax they may owe. The form also includes sections for taxpayers to record their estimated tax payments and any credits from previous overpayments. Importantly, the 40ES must be filed by specific deadlines throughout the year, with the first payment typically due by April 15. Maintaining accurate records of estimated tax payments is essential, as the Alabama Department of Revenue does not send notices of amounts paid. Understanding the requirements and procedures associated with the 40ES form can help taxpayers manage their financial responsibilities effectively.

FORM |

ALABAMA DEPARTMENT OF REVENUE |

40ES |

ESTIMATED TAX |

|

INDIVIDUAL & CORPORATE TAX DIVISION |

|

(WORKSHEET – KEEP FOR YOUR RECORDS – DO NOT FILE) |

Name |

|

CALENDAR YEAR

2013

or Fiscal Year Ending

Social Security Number

1 Enter amount of adjusted gross income expected in taxable year |

1 |

2If deductions are itemized, enter total of such deductions expected. If deductions

|

will not be itemized, enter the amount from the standard deduction table |

2 |

|

|

|

3 |

Enter amount of federal income tax liability for taxable year |

3 |

|

|

|

4 |

Total of lines 2 and 3 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

4 |

|

5 |

Subtract line 4 from line 1. Enter balance here |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

5 |

|

6 |

Personal exemption and dependent exemption(s) (see instructions for Forms 40 and 40NR for amounts) |

6 |

|

||

7 |

Subtract line 6 from line 5. This is your estimated taxable income |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

7 |

|

8Compute tax on amount on line 7 at the following rates:

|

Single or Married & Filing Separately |

Married & Filing Jointly |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

a |

1st $500 |

. 2% |

1st $1000 |

2% |

8a |

|

|

|

|

b |

Next $2500 |

. 4% |

Next $5000 |

4% |

8b |

|

|

|

|

c |

Over $3000 |

. 5% |

Over $6000 |

5% |

8c |

|

|

|

|

9 Add lines 8a, 8b, 8c. Enter total here |

. . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . |

. . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

9 |

|

||

|

|

|

|

|

|

||||

10 Amount of Alabama income tax you estimate will be withheld from your wages in taxable year. Enter balance here |

|

10 |

|

||||||

11 Subtract line 10 from line 9. Enter balance here. This is your estimated tax. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

||||

If less than five hundred dollars ($500), no estimated tax is required to be filed (see instructions). |

. . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

11 |

|

||||

|

|

|

|

|

|

|

|||

|

|

RECORD OF STATE OF ALABAMA ESTIMATED TAX PAYMENTS AND CREDIT |

|||||||

|

|

|

|

Amount |

|

Date Paid |

|

Check Number, etc. |

|

1Overpayment credit from last year credited to estimated tax for this year. (Make sure this credit is shown in the proper space on your Alabama income tax return for last year. . . . . . . . . . . . . . .

2 First payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Second payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4 Third payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Fourth payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6 Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

2

3

4

5

6

ENTER THIS AMOUNT ON THE PROPER LINE OF YOUR 2013 ALABAMA

INDIVIDUAL INCOME TAX RETURN, FORM 40 OR FORM 40NR.

NOTE: The Alabama Department of Revenue does not send notices of amounts paid on estimated tax. Therefore, it is important that you maintain this record.

Form 40ES Instructions

Who Must Pay Estimated Tax

If you owe additional tax for 2012, you may have to pay esti- mated tax for 2013.

You can use the following general rule as a guide during the year to see if you will have enough withholding, or if you should in- crease your withholding or make estimated tax payments.

General Rule. In most cases, you must pay estimated tax for 2013 if both of the following apply.

1.You expect to owe at least $500 in tax for 2013, after sub- tracting your withholding and credits.

2.You expect your withholding plus your credits to be less than the smaller of:

a.90% of the tax to be shown on your 2013 tax return, or

b.100% of the tax shown on the your 2012 tax return. Your 2012 tax return must cover all 12 months.

Special Rule for Higher Income Taxpayers

If your Alabama AGI for 2012 was more than $150,000 ($75,000 if your filing status for 2013 is Married Filing a Separate Return) substitute 110% for 100% in (2b) under General Rule, above.

When and Where to File Estimated Tax

Your estimated tax must be filed on or before April 15, 2013, or on such later dates as specified under “Farmers.” It should be mailed to the Alabama Department of Revenue, Individual Esti- mates, P.O. Box 327485, Montgomery, AL

Payment of Estimated Tax

Your estimated tax may be paid in full or in equal installments on or before April 15, 2013, June 15, 2013, September 15, 2013 and January 15, 2014. If the 15th falls on a Saturday, Sunday, or State holiday, the due date will then be considered the following

business day. Checks or money orders should be made payable to the Alabama Department of Revenue.

Changes In Tax

Even though your situation on April 15 is such that you are not required to file estimated tax at that time, your expected tax may change so that you will be required to file estimated tax later. In such case, the time for filing is as follows: June 15, if the change occurs after April 1 and before June 2; September 15, if the change occurs after June 1 and before September 2; January 15, if the change occurs after September 1. If, after you have filed a voucher, you find that your estimated tax is substantially increased or de- creased as the result of a change in your tax, you should file an amended voucher on or before the next filing date – June 15, 2013, September 15, 2013, January 15, 2014.

Farmers

If at least 2/3 of your estimated gross income for the taxable year is derived from farming, you may pay estimated tax at any time on or before January 15, 2014 instead of April 15, 2013. If you wait until January 15, 2014, you must pay the entire balance of the estimated tax. However, if farmers file their final tax return on or before March 2, 2013, and pay the total tax at that time, they need not file estimated tax.

Fiscal Year

If you file your income tax return on a fiscal year basis, you will substitute for the dates specified in the above instructions the months corresponding thereto.

Penalties for Underpayment

Penalties are provided for underpaying the Alabama income tax by at least $500.00.

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➀ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

✁

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

ADOR |

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➁ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

✁

ADOR

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➂ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

✁

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

ADOR |

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

✁ |

|

DETACH ALONG THIS LINE AND MAIL VOUCHER WITH YOUR FULL PAYMENT |

|

|

|||||||||

|

|

|

40ES 2013 |

|

|

|

Alabama Department of Revenue |

➃ |

|||||

|

|

|

|

|

|

||||||||

|

|

|

Estimated Income Tax Payment Voucher |

||||||||||

|

|

|

|||||||||||

PRIMARY TAXPAYER’S |

SPOUSE’S |

|

|

|

LAST |

|

|

||||||

FIRST NAME |

|

|

FIRST NAME |

|

|

|

NAME • |

|

|

||||

MAILING |

|

|

|

|

|

|

|

|

|

|

|

||

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

DAYTIME |

|

|

|

CITY |

|

|

|

STATE |

|

|

ZIP |

|

TELEPHONE NUMBER |

|

|

|

|

✁

CHECK IF FISCAL YEAR

Beginning Date:

Ending Date: •

Primary Taxpayer SSN: •

Spouse SSN: |

• |

Amount Paid With Voucher: $ •

MAIL TO: Alabama Department of Revenue, Individual Estimates,

P.O. Box 327485, Montgomery, AL

ADOR |

Instructions

1.Be sure you are using a form for the proper year. Do not use this form to file for any calendar year other than the year printed in bold type on the face of the form. Individuals who file on fiscal year basis (other than calendar year ending Dec. 31) should show beginning and ending dates of fiscal year in spaces provided on Form 40ES and each payment voucher.

2.Enter your social security number in space pro- vided. If joint voucher, enter spouse’s number on the line after yours.

3.Enter your first name, middle initial, and last name. If joint estimated tax, show first name and middle initial of both spouses. (Example: John T. and Mary A. Doe).

4.The amount to be shown on Amount Paid With Voucher line is determined by (a) the date you meet the requirements for filing a estimated tax,

(b) the amount of credit, if any, for overpayment from last year or income taxes withheld. Any overpayment credit may be applied to your earli- est installment or divided equally among all the installments for the year. See the following schedule:

Requirements Met |

Required |

Amt. Due With |

|

After |

& Before |

Filing Date |

Voucher |

1/4 of line 1 |

|||

|

|

|

|

1/3 of line 1 |

|||

|

|

|

|

1/2 of line 1 |

|||

|

|

|

|

All of line 1 |

|||

|

|

|

|

MAIL TO: Alabama Department of Revenue

Individual Estimates

P.O. Box 327485

Montgomery, AL

| Fact Name | Detail |

|---|---|

| Form Purpose | The Alabama 40ES form is used for estimating individual and corporate tax payments. |

| Filing Requirement | Taxpayers must file if they expect to owe at least $500 in taxes after withholding and credits. |

| Filing Deadline | The estimated tax must be filed by April 15, 2013, or on specified later dates for farmers. |

| Payment Schedule | Payments can be made in full or in four equal installments due on April 15, June 15, September 15, and January 15. |

| Overpayment Credit | Taxpayers can apply overpayment credits from the previous year to their estimated tax. |

| Exemption Details | Personal and dependent exemptions are deducted to determine estimated taxable income. |

| Tax Rates | Tax rates vary based on income brackets, with rates of 2%, 4%, and 5% applicable. |

| Record Keeping | Taxpayers should maintain records of estimated tax payments, as the Alabama Department of Revenue does not send notices. |

| Governing Law | The Alabama 40ES form is governed by Alabama state tax laws. |

| Fiscal Year Consideration | Taxpayers using a fiscal year must adjust the filing dates accordingly. |

Filling out the Alabama 40ES form is an important step for individuals who need to estimate their tax obligations for the year. This form helps you calculate your expected tax liability and determine whether you need to make estimated tax payments. Below are the steps to guide you through the process of completing the form accurately.

After completing the form, keep it for your records. If your estimated tax exceeds $500, you will need to submit the appropriate payment along with the form to the Alabama Department of Revenue by the specified deadlines. This ensures you stay compliant with Alabama tax regulations and avoid any penalties for underpayment.

What is the Alabama 40ES form used for?

The Alabama 40ES form is used for estimating your state income tax for the year. If you expect to owe at least $500 in taxes after subtracting any withholding and credits, you will need to file this form. It helps you determine how much you should pay in estimated taxes throughout the year to avoid penalties later.

Who needs to file the Alabama 40ES form?

If you owed additional tax last year or expect your withholding to be insufficient for the current year, you may need to file the 40ES form. Specifically, you must file if you expect to owe at least $500 in taxes after accounting for any withholding and credits. This applies to both individuals and corporations.

When are the estimated tax payments due?

Estimated tax payments are due in four installments. These payments should be made by April 15, June 15, September 15, and January 15 of the following year. If any of these dates fall on a weekend or holiday, the due date shifts to the next business day. You can choose to pay the entire amount at once or in equal installments.

How do I calculate my estimated tax using the 40ES form?

To calculate your estimated tax, start by entering your expected adjusted gross income. Then, subtract any deductions and your federal tax liability. This gives you your estimated taxable income. From there, apply the tax rates outlined on the form to determine your estimated tax amount. Finally, subtract any expected withholding from your wages to find your net estimated tax due.

What happens if I underpay my estimated taxes?

If you underpay your estimated taxes by $500 or more, you may face penalties. It’s important to monitor your tax situation throughout the year. If your income changes significantly, you may need to adjust your estimated payments to avoid penalties. Keep in mind that if you file your tax return and pay the total tax owed by the due date, you can avoid these penalties.

Using the wrong year form: Many individuals mistakenly use a form from a different year. It is crucial to ensure that the form corresponds to the correct tax year, as indicated in bold on the form.

Incorrectly entering social security numbers: Some people fail to enter their social security number correctly. If filing jointly, both spouses' numbers must be included. This mistake can lead to processing delays.

Miscalculating estimated income: Estimating income can be challenging. People often either overestimate or underestimate their adjusted gross income, which affects their tax calculations. It is essential to provide an accurate figure to avoid complications later.

Neglecting to include credits: Many filers forget to account for any overpayment credits from the previous year. This oversight can result in a higher estimated tax than necessary, leading to overpayment.

The Alabama 40ES form is used for estimating individual and corporate taxes in the state of Alabama. Alongside this form, several other documents are often utilized to ensure compliance with tax regulations. Each document serves a specific purpose in the tax filing process, helping taxpayers accurately report their financial situation and obligations.

Understanding these forms and their purposes is crucial for effective tax management. Each document plays a role in ensuring that individuals and businesses meet their tax obligations accurately and timely, thereby avoiding potential penalties or issues with tax authorities.

The Alabama 40ES form is an essential document for estimating tax payments, but it shares similarities with several other tax-related forms. Here are four documents that are comparable to the Alabama 40ES form:

When filling out the Alabama 40ES form, attention to detail is crucial. Here are nine important dos and don'ts to consider:

Following these guidelines will help ensure that your estimated tax filing process is smooth and compliant with Alabama tax regulations.

This form is applicable to both individuals and corporations. Anyone who expects to owe taxes may need to use it.

You only need to file the form if you expect to owe at least $500 in taxes after subtracting your withholding and credits.

For some taxpayers, making estimated tax payments is mandatory if they do not meet certain withholding thresholds.

There are specific due dates for filing the 40ES form, typically April 15, June 15, September 15, and January 15 of the following year.

Currently, the 40ES form must be mailed to the Alabama Department of Revenue. Electronic filing is not an option.

Each taxpayer's situation is unique, and deductions can vary based on individual circumstances. Always check the instructions for specific amounts.

If your financial situation changes, you can adjust your estimated tax payments by filing an amended voucher before the next due date.

Penalties can be imposed for underpaying your estimated tax by $500 or more, so it's important to keep track of your tax obligations throughout the year.

Filling out the Alabama 40ES form for estimated taxes can seem daunting, but understanding its key components can simplify the process. Here are nine essential takeaways to keep in mind when using this form:

By understanding these key points, individuals and businesses can navigate the Alabama 40ES form more effectively and ensure compliance with state tax requirements.