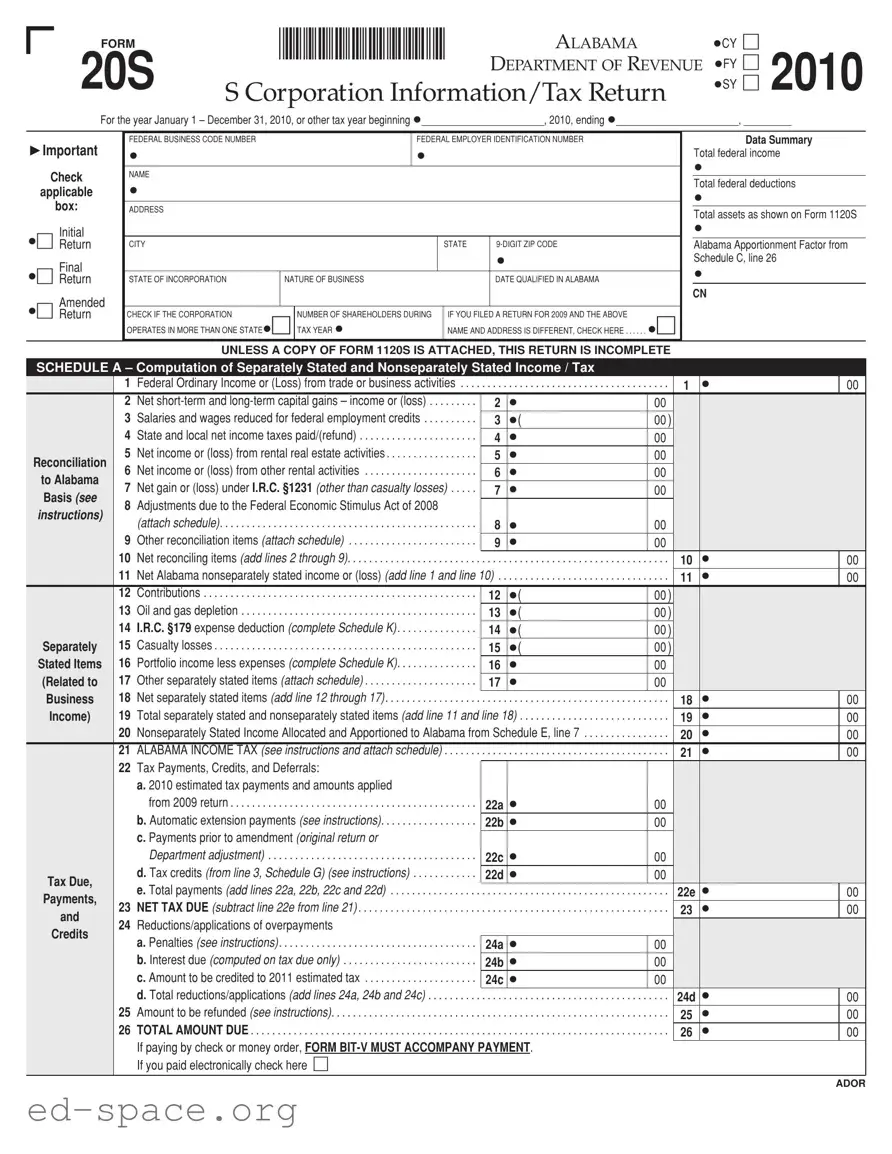

The Alabama 20S form serves as a crucial document for S corporations operating within the state, detailing their income, deductions, and tax obligations for a specific tax year. This form, officially titled "S Corporation Information/Tax Return," is designed to capture a comprehensive overview of the corporation's financial activities, including total federal income, deductions, and assets. Notably, it requires information such as the federal business code number and employer identification number, which are essential for proper identification and processing. The form is divided into several schedules, each addressing different aspects of the corporation's financials, from the computation of income and deductions to apportionment factors that determine how income is allocated to Alabama. Moreover, it includes sections for tax credits, adjustments, and any nonbusiness income or expenses, ensuring a thorough accounting of the corporation's financial performance. The 20S form not only facilitates compliance with Alabama tax laws but also provides a structured approach for S corporations to report their financial activities accurately and transparently.

FORM |

*1000012S* |

ALABAMA |

•CY |

|

|

|

20S |

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

•SY |

2010 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

•FY |

|

|

|||||||

|

|

|

|

|

S Corporation Information/Tax Return |

|

|

|

|

||||||||||||

|

For the year January 1 – December 31, 2010, or other tax year beginning •_______________________, 2010, ending •_______________________, _________ |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Important |

|

FEDERAL BUSINESS CODE NUMBER |

|

|

FEDERAL EMPLOYER IDENTIFICATION NUMBER |

|

|

|

|

|

|

Data Summary |

||||||||

|

|

• |

|

|

|

• |

|

|

|

|

|

|

|

Total federal income |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Check |

|

NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total federal deductions |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

applicable |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||||

|

box: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets as shown on Form 1120S |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Initial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

• |

Return |

|

CITY |

|

|

|

|

|

STATE |

|

|

|

|

Alabama Apportionment Factor from |

|||||||

|

Final |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

Schedule C, line 26 |

||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||

Return |

|

STATE OF INCORPORATION |

NATURE OF BUSINESS |

|

|

DATE QUALIFIED IN ALABAMA |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

CN |

|

|

|

|||||||||||

|

Amended |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return |

|

CHECK IF THE CORPORATION |

|

NUMBER OF SHAREHOLDERS DURING |

IF YOU FILED A RETURN FOR 2009 AND THE ABOVE |

|

|

|

|

|

|

|

|

||||||||

|

|

|

OPERATES IN MORE THAN ONE STATE• |

|

TAX YEAR • |

NAME AND ADDRESS IS DIFFERENT, CHECK HERE |

• |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNLESS A COPY OF FORM 1120S IS ATTACHED, THIS RETURN IS INCOMPLETE |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE A – Computation of Separately Stated and Nonseparately Stated Income / Tax |

|

|

|

|

|

|

|

|

|||||||||||||

|

|

1 |

Federal Ordinary Income or (Loss) from trade or business activities . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

1 |

|

• |

|

|

00 |

||||||||

|

|

2 |

Net |

2 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

3 |

. . . . . . . . . .Salaries and wages reduced for federal employment credits |

3 |

•( |

00 ) |

|

|

|

|

|

|

|

||||||||

|

|

4 |

. . . . . . . . . . . . . . . . . . . . . .State and local net income taxes paid/(refund) |

4 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

5 |

Net income or (loss) from rental real estate activities |

|

|

|

|

|

|

|

|

|

|

|

|||||||

Reconciliation |

5 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

6 |

Net income or (loss) from other rental activities |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

to Alabama |

6 |

• |

00 |

|

|

|

|

|

|

|

||||||||||

|

7 |

Net gain or (loss) under I.R.C. §1231 (other than casualty losses) |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

7 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

|

Basis (SEE |

|

|

|

|

|

|

|

|||||||||||||

|

8 |

Adjustments due to the Federal Economic Stimulus Act of 2008 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

INSTRUCTIONS) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

(attach schedule) |

|

|

|

|

|

|

8 |

• |

00 |

|

|

|

|

|

|

|

||

|

|

|

|

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

|

|

|

|

|

|

|

|||||

|

|

9 |

. . . . . . . . . . . . . . . . . . . . . . . .Other reconciliation items (attach schedule) |

9 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

10 |

Net reconciling items (add lines 2 through 9) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

10 |

|

• |

|

|

00 |

|||||||||

|

|

11 |

. .Net Alabama nonseparately stated income or (loss) (add line 1 and line 10) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

11 |

|

• |

|

|

00 |

||||||||||

|

|

12 |

Contributions . . . |

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

12 |

•( |

00 ) |

|

|

|

|

|

|

|

||

|

|

13 |

. . . . . . . .Oil and gas depletion |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

13 |

•( |

00 ) |

|

|

|

|

|

|

|

|||

|

|

14 |

. . . . . . . . . . . . . . .I.R.C. §179 expense deduction (complete Schedule K) |

14 |

•( |

00 ) |

|

|

|

|

|

|

|

||||||||

|

|

15 |

Casualty losses . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Separately |

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

15 |

•( |

00 ) |

|

|

|

|

|

|

|

||||

|

Stated Items |

16 |

. . . . . . . . . . . . . . .Portfolio income less expenses (complete Schedule K) |

16 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

(Related to |

17 |

Other separately stated items (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

17 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

|

|

18 |

Net separately stated items (add line 12 through 17) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Business |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

18 |

|

• |

|

|

00 |

|||||||||

|

Income) |

19 |

. . . . . . . . . . . . . . . . . . . . . . . .Total separately stated and nonseparately stated items (add line 11 and line 18) |

. . . . |

19 |

|

• |

|

|

00 |

|||||||||||

|

|

20 |

. . . . . . . . . . . .Nonseparately Stated Income Allocated and Apportioned to Alabama from Schedule E, line 7 |

. . . . |

20 |

|

• |

|

|

00 |

|||||||||||

|

|

21 |

ALABAMA INCOME TAX (see instructions and attach schedule) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

21 |

|

• |

|

|

00 |

|||||||

|

|

22 |

Tax Payments, Credits, and Deferrals: |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

a. 2010 estimated tax payments and amounts applied |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

from 2009 return |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

22a |

• |

00 |

|

|

|

|

|

|

|

||

|

|

|

|

. . . . . . . . . . . . . . . . . .b. Automatic extension payments (see instructions) |

22b |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

c. Payments prior to amendment (original return or |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Department adjustment) . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

22c |

• |

00 |

|

|

|

|

|

|

|

||

|

Tax Due, |

|

|

. . . . . . . . . . . .d. Tax credits (from line 3, Schedule G) (see instructions) |

22d |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

Payments, |

|

|

. . . . . . . . . .e. Total payments (add lines 22a, 22b, 22c and 22d) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

22e |

• |

|

|

00 |

|||||||

|

23 |

NET TAX DUE (subtract line 22e from line 21) |

|

|

|

|

|

23 |

|

• |

|

|

00 |

||||||||

|

and |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

|

|

|

||||||||||||

|

24 |

Reductions/applications of overpayments |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Credits |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

a. Penalties (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

24a |

• |

00 |

|

|

|

|

|

|

|

|||

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . .b. Interest due (computed on tax due only) |

24b |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

c. Amount to be credited to 2011 estimated tax |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

24c |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

d. Total reductions/applications (add lines 24a, 24b and 24c) |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

24d |

• |

|

|

00 |

||||||||

|

|

25 |

. . . . . . . . . . . . . . . . . . . . .Amount to be refunded (see instructions) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

25 |

|

• |

|

|

00 |

|||||||

|

|

26 |

. . . . . .TOTAL AMOUNT DUE |

. . . |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

26 |

|

• |

|

|

00 |

|||

|

|

|

|

If paying by check or money order, FORM |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

If you paid electronically check here |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADOR |

|

|

*1000022S* |

Page 2 |

|

FORM 20S – 2010 |

|

|

|

|

SCHEDULE B – Allocation of Nonbusiness Income, Loss, and Expense |

|

|

|

|

|

Identify by account name and amount all items of nonbusiness income, loss, and expense removed from apportionable income and those items which are directly allocable to Alabama. Adjustment(s) must also be made for any proration of expenses under Alabama Income Tax Rule

allowable deduction that is applicable to both business and nonbusiness income of the taxpayer shall be prorated to each class of income in determining income subject to tax as provided…” (See instructions).

|

DIRECTLY ALLOCABLE ITEMS |

|

ALLOCABLE GROSS INCOME / LOSS |

|

|

|

RELATED EXPENSE |

|

NET OF RELATED EXPENSE |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Column A |

|

Column B |

|

|

Column C |

|

Column D |

|

Column E |

|

Column F |

|||

|

|

|

Everywhere |

|

Alabama |

|

|

Everywhere |

|

Alabama |

|

Everywhere |

|

Alabama |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Col. A less Col. C) |

(Col. B less Col. D) |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonseparately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1c |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1d Total (add lines 1a, 1b, and 1c) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

• |

||

Separately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1e |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1f |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1g |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1h Total (add lines 1e, 1f, and 1g) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

• |

||

SCHEDULE C – Apportionment Factor Schedule. Do not complete if entity operates exclusively in Alabama. |

|

|

|||||||||||||||

|

TANGIBLE PROPERTY AT COST FOR |

|

|

ALABAMA |

|

|

|

|

|

EVERYWHERE |

|||||||

|

PRODUCTION OF BUSINESS INCOME |

BEGINNING OF YEAR |

|

END OF YEAR |

|

BEGINNING OF YEAR |

|

END OF YEAR |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Inventories |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Land |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Furniture and fixtures |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Machinery and equipment |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Buildings and leasehold improvements |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||

6 |

IDB/IRB property (at cost) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Government property (at FMV) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

Less Construction in progress (if included) |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||

10 |

Totals |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Average owned property (BOY + EOY ÷ 2) |

|

|

|

• |

|

|

|

|

|

|

|

• |

|

|||

12 |

Annual rental expense |

|

|

• |

x8 = |

• |

|

|

|

• |

|

x8 = |

• |

|

|||

13 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total average property (add line 11 and line 12) |

|

13a |

• |

|

|

|

. . . . . . |

. . . . |

. . . . . . . . . . . . |

13b |

• |

|

||||

14 |

Alabama property factor — 13a ÷ 13b = line 14 |

. |

. . . . . . |

. . . . . . |

. . . . . . . . . . . |

. . . . . . . |

. . . . . |

. . . . . . . |

. . . . |

. . . . . . . . . . . . |

14 |

• |

% |

||||

|

SALARIES, WAGES, COMMISSIONS AND OTHER COMPENSATION |

|

|

15a |

ALABAMA |

|

15b |

EVERYWHERE |

15c |

|

|||||||

|

RELATED TO THE PRODUCTION OF BUSINESS INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

||||

15 |

Alabama payroll factor — 15a ÷ 15b = 15c |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

% |

|||

|

|

|

SALES |

|

|

|

|

ALABAMA |

|

|

EVERYWHERE |

|

|

||||

16 |

Destination sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

17 |

. . . . . . . . . . . . . . . . . . . . . . . .Origin sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

18 |

. . . . .Total gross receipts from sales |

. . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|

19 |

. . . . . . . . . . . . . . . . . . . . . . . .Dividends |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

20 |

. . . . . . . . . . . . . . . . . . . . . . . .Interest |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

21 |

. . . . . . . . . . . . . . . . . . . . . . . .Rents |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

22 |

. . . . . . . . . . . . . . . . . . . . . . . .Royalties |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

23 |

. . . . . . .Gross proceeds from capital and ordinary gains |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

24Other •___________________________________ (Federal 1120S, line •_____ ) •

25 |

Alabama sales factor — 25a ÷ 25b = line 25c |

25a• |

25b• |

|

25c• |

% |

26 |

Sum of lines 14, 15c, and 25c ÷ 3 = ALABAMA APPORTIONMENT FACTOR (Enter here and on line 4, Schedule E, page 3) |

26 |

• |

% |

||

ADOR

| Fact Name | Detail |

|---|---|

| Form Title | Alabama CY 20S Department of Revenue S Corporation Information/Tax Return |

| Tax Year | Applicable for the year January 1 – December 31, 2010, or other specified tax year. |

| Governing Law | Alabama Code Title 40, Chapter 18, Article 2 - Alabama Income Tax Act |

| Filing Requirement | Required for S Corporations operating in Alabama or having income sourced to Alabama. |

| Federal Business Code | Mandatory entry for identifying the type of business on the form. |

| Apportionment Factor | Calculated using property, payroll, and sales factors to determine income taxable in Alabama. |

| Initial Return | Corporations must check the box if this is their initial return. |

| Amended Return | Corporations must check the box if they are filing an amended return for the previous tax year. |

| Attachments Required | A complete return must include copies of Federal Form 1120S and Alabama Schedule K-1 for each shareholder. |

Completing the Alabama 20S form is an essential task for S corporations operating within the state. This form collects various financial details, which are crucial for tax assessment. Follow the steps below to accurately fill out the form.

After completing the form, review all entries for accuracy. Ensure that all required schedules and documents are attached before submitting the form to the Alabama Department of Revenue. This will help avoid delays or issues with your filing.

What is the Alabama 20S form used for?

The Alabama 20S form is specifically designed for S corporations operating in Alabama. It serves as the S Corporation Information and Tax Return, allowing these entities to report their income, deductions, and credits for state tax purposes. By filing this form, S corporations ensure compliance with Alabama tax laws and accurately calculate their tax obligations based on their financial activities for the year.

Who needs to file the Alabama 20S form?

Any S corporation that is incorporated in Alabama or qualifies to do business in the state must file the Alabama 20S form. This includes corporations that have elected S corporation status at the federal level and operate within Alabama. If an S corporation has shareholders who reside in Alabama, it is also required to file this form, regardless of where the corporation itself is incorporated.

What information is required on the Alabama 20S form?

The Alabama 20S form requires various pieces of information, including the corporation's name, address, and federal employer identification number (EIN). It also asks for financial details such as total federal income, deductions, and assets. Additionally, the form includes schedules for reporting separately stated income, apportionment factors, and any applicable tax credits. Completing the form accurately is essential for ensuring that the corporation meets its tax obligations.

What happens if an S corporation fails to file the Alabama 20S form?

If an S corporation fails to file the Alabama 20S form, it may face penalties and interest on any taxes owed. The Alabama Department of Revenue may also take enforcement actions, which could include audits or assessments of additional taxes. Moreover, not filing can lead to complications for shareholders, as they may not receive the necessary documentation to report their income accurately on their personal tax returns. It is crucial for S corporations to file on time to avoid these potential issues.

Failing to provide the correct federal employer identification number. This number is crucial for identifying the business and ensuring proper tax processing.

Not checking the box for the type of return being filed, such as initial or amended. This oversight can lead to confusion and processing delays.

Omitting to attach Form 1120S when required. If this form is not included, the return will be considered incomplete.

Incorrectly calculating the Alabama apportionment factor. This figure is essential for determining how much income is taxable in Alabama.

Providing inaccurate or incomplete information about shareholders. This can affect the distribution of income and the overall tax calculation.

Neglecting to sign and date the return. An unsigned return is not valid and can lead to penalties or delays in processing.

The Alabama 20S form is essential for S corporations operating in Alabama, as it serves as the state's tax return for these entities. Alongside this form, several other documents are commonly required to ensure compliance with state tax regulations. Each of these forms serves a specific purpose in the overall tax filing process.

Understanding these accompanying documents is crucial for S corporations in Alabama to fulfill their tax obligations effectively. Each form plays a vital role in ensuring compliance with both state and federal tax laws.

The Alabama 20S form serves as a tax return for S Corporations in Alabama, detailing income, deductions, and other financial information. Several other documents share similarities with the Alabama 20S form, each serving specific purposes in tax reporting and compliance. Below is a list of ten documents that are similar to the Alabama 20S form, along with explanations of how they relate.

When filling out the Alabama 20S form, keep these tips in mind:

Avoid these common mistakes:

This is incorrect. While the form is primarily for S corporations operating in Alabama, it can also apply to those conducting business in multiple states. The form requires specific information about income and apportionment regardless of the number of states involved.

This is a misunderstanding. Filing the Alabama 20S form is mandatory for S corporations that are subject to Alabama income tax. Failure to file can result in penalties and interest on unpaid taxes.

This is misleading. The form requires detailed information about both federal and Alabama-specific income, deductions, and apportionment factors. Accurate reporting is essential for compliance with state tax laws.

Amending the form can be complex. Corporations must follow specific procedures and may need to provide additional documentation to support the changes. It is important to carefully review the instructions for amendments to ensure compliance.

When filling out and using the Alabama 20S form, there are several key points to keep in mind. Understanding these takeaways can help ensure accuracy and compliance.

By keeping these takeaways in mind, you can navigate the process of completing the Alabama 20S form more effectively. Proper preparation and attention to detail will help in achieving a smoother filing experience.