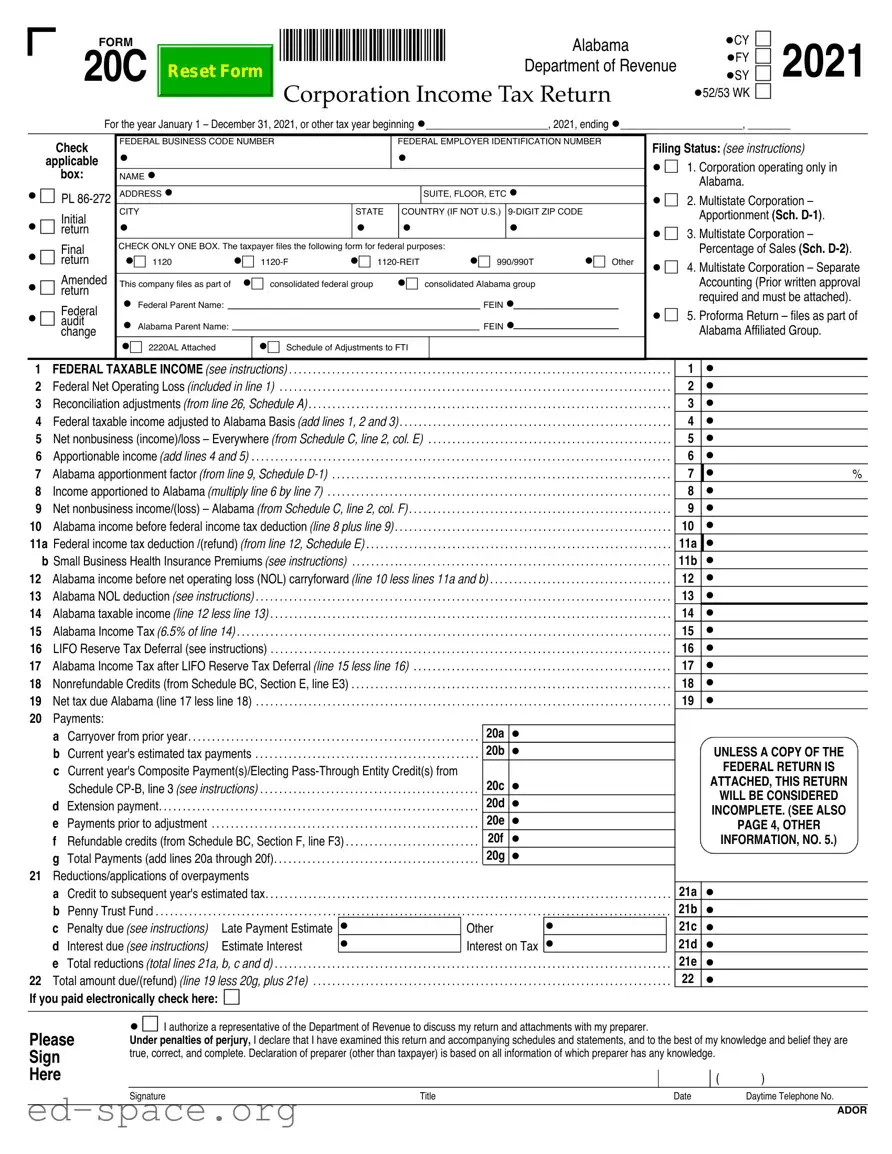

The Alabama 20C form is a crucial document for corporations operating within the state, serving as the official Corporation Income Tax Return. Designed to capture essential financial information for the tax year, this form includes fields for the corporation's name, address, and federal identification numbers. Corporations must indicate their filing status, whether they are operating solely in Alabama or are part of a multistate operation. The form requires detailed reporting of federal taxable income, adjustments for Alabama-specific tax regulations, and calculations for apportionable income based on the corporation's activities within the state. Additionally, corporations must account for net operating losses and tax credits available under Alabama law. The 20C form also includes sections for reconciliation adjustments, allowing corporations to align their federal taxable income with Alabama taxable income. Accurate completion of this form is essential for compliance with state tax obligations and can significantly impact a corporation's tax liability.

FORM

20C

Reset Form

*2100012C* Alabama

Department of Revenue

Corporation Income Tax Return

•CY

•FY

•SY

•52/53 WK

6

6 2021

6

6

For the year January 1 – December 31, 2021, or other tax year beginning •_______________________, 2021, ending •_______________________, ________

Check

applicable

box:

•6 PL

•6 returnInitial

•6 returnFinal

•6 returnAmended

•6 auditFederal change

FEDERAL BUSINESS CODE NUMBER |

|

FEDERAL EMPLOYER IDENTIFICATION NUMBER |

|

Filing Status: (see instructions) |

|||

• |

|

|

• |

|

|

|

|

|

|

|

|

|

• 6 1. Corporation operating only in |

||

NAME • |

|

|

|

|

|

|

|

|

|

|

|

|

|

Alabama. |

|

ADDRESS • |

|

|

|

SUITE, FLOOR, ETC • |

|

|

|

|

|

|

|

|

• 6 2. Multistate Corporation – |

||

CITY |

|

STATE |

COUNTRY (IF NOT U.S.) |

|

|

||

|

|

|

Apportionment (Sch. |

||||

• |

|

• |

• |

• |

|

|

• 6 3. Multistate Corporation – |

CHECK ONLY ONE BOX. The taxpayer files the following form for federal purposes: |

•6 |

|

Percentage of Sales (Sch. |

||||

•6 1120 |

•6 |

•6 |

•6 990/990T |

Other |

• 6 4. Multistate Corporation – Separate |

||

|

|

|

|

|

|

|

|

This company files as part of |

•6 consolidated federal group |

•6 consolidated Alabama group |

|

|

Accounting (Prior written approval |

||

• Federal Parent Name: |

|

|

|

FEIN • |

|

|

required and must be attached). |

|

|

|

|

|

• 6 5. Proforma Return – files as part of |

||

• Alabama Parent Name: |

|

|

|

FEIN • |

|

|

|

|

|

|

|

|

Alabama Affiliated Group. |

||

|

|

|

|

|

|

|

|

•6 2220AL Attached |

•6 Schedule of Adjustments to FTI |

|

|

|

|

||

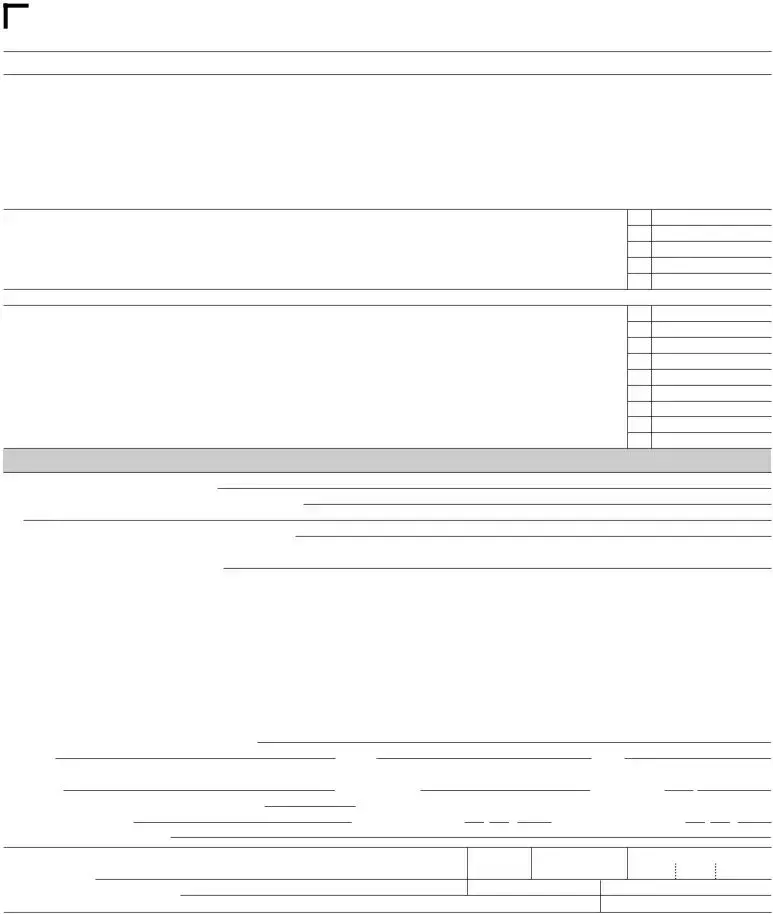

1 |

FEDERAL TAXABLE INCOME (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

2 |

Federal Net Operating Loss (included in line 1) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

3 |

Reconciliation adjustments (from line 26, Schedule A) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

4 |

Federal taxable income adjusted to Alabama Basis (add lines 1, 2 and 3) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

5 |

Net nonbusiness (income)/loss – Everywhere (from Schedule C, line 2, col. E) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

6 Apportionable income (add lines 4 and 5) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

7 |

Alabama apportionment factor (from line 9, Schedule |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

8 |

Income apportioned to Alabama (multiply line 6 by line 7) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

9 |

Net nonbusiness income/(loss) – Alabama (from Schedule C, line 2, col. F) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

10 |

Alabama income before federal income tax deduction (line 8 plus line 9) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

11a Federal income tax deduction /(refund) (from line 12, Schedule E) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

|

b Small Business Health Insurance Premiums (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

12 |

Alabama income before net operating loss (NOL) carryforward (line 10 less lines 11a and b) . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

13 |

Alabama NOL deduction (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

14 |

Alabama taxable income (line 12 less line 13) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

15 |

Alabama Income Tax (6.5% of line 14) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

16 LIFO Reserve Tax Deferral (see instructions) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||

17 |

Alabama Income Tax after LIFO Reserve Tax Deferral (line 15 less line 16) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

18 |

Nonrefundable Credits (from Schedule BC, Section E, line E3) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

19 |

Net tax due Alabama (line 17 less line 18) |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

20 |

Payments: |

20a |

|

|

|

a |

Carryover from prior year |

• |

|

|

20b |

|||

|

b |

Current year's estimated tax payments |

• |

|

|

|

|||

cCurrent year's Composite Payment(s)/Electing

|

Schedule |

|

20c |

• |

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . 20d |

|

|||

d |

Extension payment |

|

|

• |

|

|

. . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . 20e |

|

|||

e Payments prior to adjustment |

|

|

• |

|

||

. . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . 20f |

|

|||

f Refundable credits (from Schedule BC, Section F, line F3) |

• |

|

||||

. . . 20g |

|

|||||

g Total Payments (add lines 20a through 20f) |

|

• |

|

|||

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . |

|

||||

21 Reductions/applications of overpayments |

|

|

|

|

||

a Credit to subsequent year's estimated tax |

. . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|||

b |

Penny Trust Fund |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . .. . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

c |

Penalty due (see instructions) |

Late Payment Estimate |

• |

Other |

|

• |

d |

Interest due (see instructions) |

Estimate Interest |

• |

Interest on Tax |

• |

|

e Total reductions (total lines 21a, b, c and d) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

22 Total amount due/(refund) (line 19 less 20g, plus 21e) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If you paid electronically check here: 6

1•

2•

3•

4•

5•

6•

7 • |

% |

8•

9•

10•

11a •

11b •

12•

13•

14•

15•

16•

17•

18•

19•

UNLESS A COPY OF THE

FEDERAL RETURN IS

ATTACHED, THIS RETURN

WILL BE CONSIDERED

INCOMPLETE. (SEE ALSO

PAGE 4, OTHER

INFORMATION, NO. 5.)

21a •

21b •

21c •

21d •

21e •

22•

Please

Sign

Here

•6 I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

|

|

( |

) |

Signature |

Title |

Date |

Daytime Telephone No. |

ADOR

*2100022C* |

PAGE 2 |

ALABAMA 20C – 2021 |

|

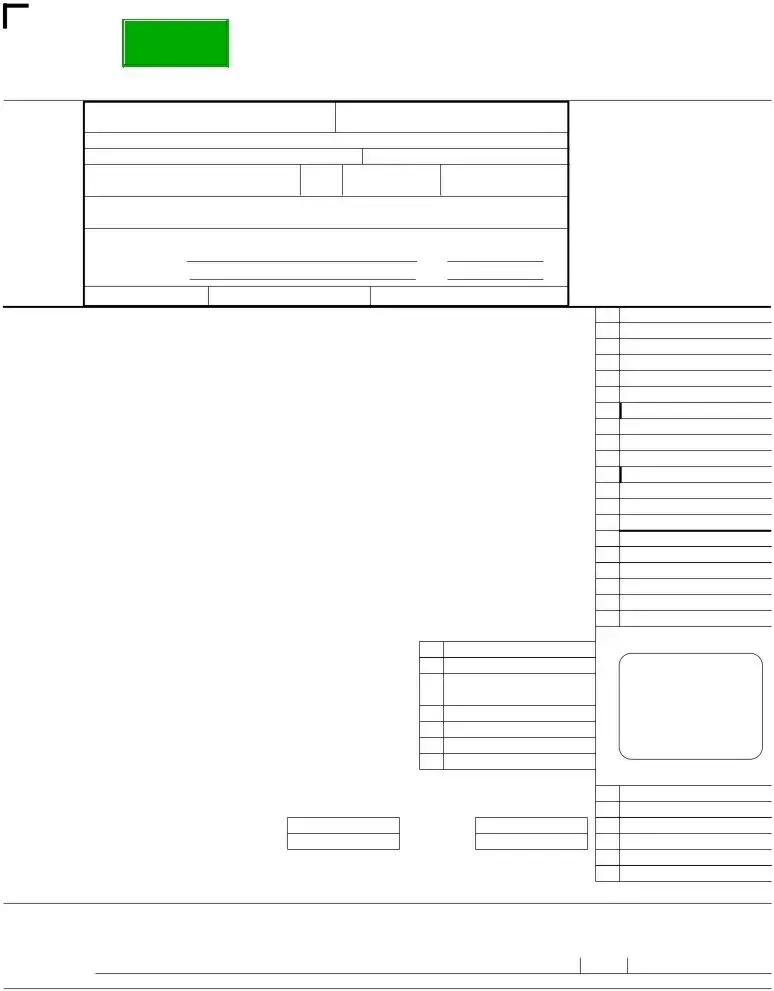

Schedule A Reconciliation Adjustments of Federal Taxable Income to Alabama Taxable Income |

|

ADDITIONS

1 |

State and local income taxes |

1 |

• |

2 |

Federal exempt interest income (other than Alabama) on state, county and municipal obligations (everywhere) |

2 |

• |

3Dividends from corporations in which the taxpayer owns less than 20 percent of stock to the extent properly deducted on

|

federal income tax return (see instructions) |

3 |

• |

4 |

Federal depreciation on pollution control items previously deducted for Alabama (see instructions) |

4 |

• |

5 |

Net income from foreclosure property pursuant to |

5 |

• |

6Related members interest or intangible expenses or costs. From Schedule AB (see instructions).

|

Total Payments 6a • |

minus Exempt Amount 6b • |

equals 6c |

• |

7 |

Captive REITS: Dividends Paid Deduction (from federal Form |

. . . . . . 7 |

• |

|

8 |

Contributions not deductible on state income tax return due to election to claim state tax credit |

. . . . . 8 |

• |

|

9 |

• |

|

9 |

• |

10 |

• |

|

10 |

• |

11 |

Total additions (add lines 1 through 10) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . 11 |

• |

DEDUCTIONS

12 |

Refunds of state and local income taxes (due to overpayment or over accrual on the federal return) |

12 |

• |

13 |

Interest income earned on direct obligations of the United States |

13 |

• |

14Interest income earned on obligations of Alabama or its subdivisions or instrumentalities to extent included in

|

federal income tax return (see instructions) |

14 |

• |

15 |

Aid or assistance provided to the Alabama State Industrial Development Authority pursuant to |

15 |

• |

16 |

Expenses not deductible on federal income tax return due to election to claim a federal tax credit |

16 |

• |

17 |

Dividends described in 26 U.S.C. §78 from corporations in which taxpayer owns more than 20% of stock (see instructions) |

17 |

• |

18Dividend income – more than 20% stock ownership (including that described in 26 U.S.C. §951) from

|

corporations to the extent the dividend income would be deductible under 26 U.S.C. §243 if received from domestic corporations. . . . |

18 |

• |

19 |

Dividends received from foreign sales corporations as determined in 26 U.S.C. §922 (see instructions) |

19 |

• |

20 |

Amount of the oil/gas depletion allowance provided by |

20 |

• |

21 |

Additional Alabama depreciation related to Economic Stimulus Act of 2008 (see instructions) |

21 |

• |

22 |

Exemption of gain under |

22 |

• |

23 |

• |

23 |

• |

24 |

• |

24 |

• |

25 |

Total deductions (add lines 12 through 24) |

25 |

• |

26TOTAL RECONCILIATION ADJUSTMENTS (subtract line 25 from line 11 above).

|

Enter here and on line 3, page 1 (enclose a negative amount in parentheses) |

26 • |

|

||||||

|

Schedule B |

|

Alabama Net Operating Loss Carryforward Calculation |

|

|

||||

|

Column 1 |

Column 2 |

Column 3 |

|

Column 4 |

Column 5 |

Column 6 |

||

|

Loss Year End |

Amount of Alabama |

Amount used in years |

|

Amount used |

Remaining unused |

Acquired |

||

|

MM / DD / YYYY |

net operating loss |

prior to this year |

|

this year |

net operating loss |

NOL |

||

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

• |

• |

|

• |

• |

|

• |

|

•6 |

|

Alabama net operating loss (enter here and on line 13, page 1). |

• |

|

|

|

|

||||

ADOR

|

*2100032C* |

PAGE 3 |

ALABAMA 20C – 2021 |

||

Schedule C |

Allocation of Nonbusiness Income, Loss, and Expense – Use only if you checked Filing Status 2, page 1 |

|

Identify by account name and amount, all items of nonbusiness income, loss and expense removed from apportionable income and those items which are directly allocable to Alabama. Adjustment(s) must also be made for any proration of expenses under Alabama Income Tax Rule

|

ALLOCABLE GROSS INCOME / LOSS |

RELATED EXPENSE |

|

NET OF RELATED EXPENSE |

|||

DIRECTLY ALLOCABLE ITEMS OF |

Column A |

Column B |

Column C |

Column D |

|

Column E |

Column F |

NONBUSINESS INCOME OR LOSS |

Everywhere |

Alabama |

Everywhere |

Alabama |

|

Everywhere |

Alabama |

1a • |

• |

• |

• |

• |

• |

|

• |

b • |

• |

• |

• |

• |

• |

|

• |

c • |

• |

• |

• |

• |

• |

|

• |

d • |

• |

• |

• |

• |

• |

|

• |

e • |

• |

• |

• |

• |

• |

|

• |

2 NET NONBUSINESS INCOME / LOSS |

Column E |

Column F |

|

Enter Column E total ((income)/loss) on line 5 of page 1. Enter Column F total (income/(loss)) on line 9 of page 1 |

• |

• |

|

|

|

|

|

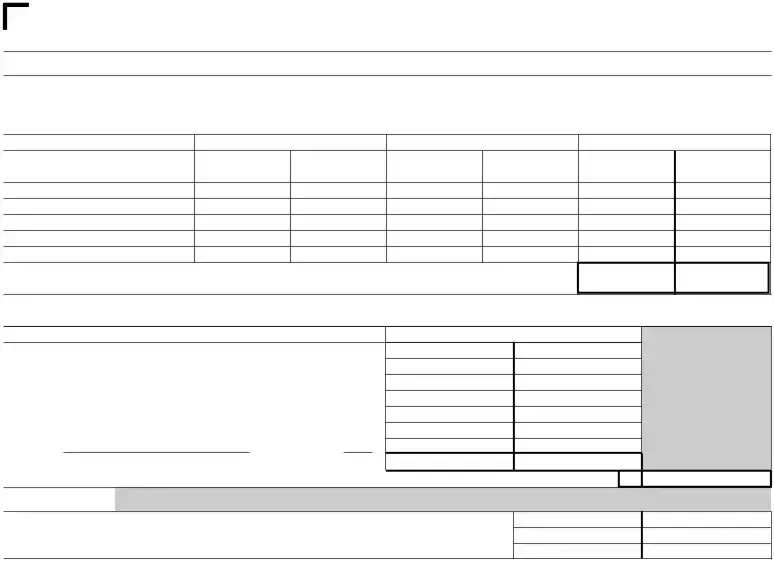

Schedule |

Apportionment Factor – Use only if Filing Status 2 or Filing Status 5, page 1 with |

|

|

Amounts must be Positive (+) Values |

|

|

|

|

|

SALES |

|

|

ALABAMA |

EVERYWHERE |

1 |

Gross receipts from sales |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

2 |

Dividends |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

3 |

Interest |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

4 |

Rents |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

5 |

Royalties |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

6 |

Gross proceeds from capital and ordinary gains . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . • |

|

• |

|

7 |

Other • |

|

(Federal 1120, line • |

) • |

|

• |

8 |

Total Sales |

. . 8a • |

|

8b • |

||

9 |

Line 8a/8b = ALABAMA APPORTIONMENT FACTOR (Enter here and on line 7, page 1) . . |

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . |

|||

|

Schedule |

Percentage of Sales – Use only if you checked Filing Status 3, page 1 – See instructions |

||||

9

•

%

DO NOT USE THIS SCHEDULE IF ALABAMA SALES EXCEED $100,000. |

ALABAMA |

EVERYWHERE |

|

1 |

Gross receipts from sales |

• |

• |

2 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tax due (multiply line 1, Alabama by .0025) (enter here and on page 1, line 15) |

• |

|

ADOR

|

*2100042C* |

PAGE 4 |

ALABAMA 20C – 2021 |

||

Schedule E |

Federal Income Tax (FIT) Deduction/(Refund) |

|

Only method 1552(a)(1) can be used to calculate the Federal Income Tax Deduction.

(a)If this corporation is an

(b)If this corporation is a

enter the amount of federal income tax paid during the year.

(c)If this corporation is a member of an affiliated group which files a consolidated federal return, enter the separate company income from line 30 of the proforma 1120 for this company on line 1. You must complete lines

Items excluded from Alabama Taxable Income must be added to adjusted total income on line 8b to calculate the Federal Income Tax deduction. (This includes any amounts listed on Schedule A lines 13, 14, 17, 18, and 19).

1 |

This company’s separate federal taxable income |

1 |

• |

|

2 |

Total positive consolidated federal taxable income |

2 |

• |

|

3 |

This company’s percentage (divide line 1 by line 2) |

3 |

• |

% |

4 |

Consolidated federal income tax (liability/payment) |

4 |

• |

|

5 |

Federal income tax for this company (multiply line 3 by line 4) |

5 |

• |

|

6 |

Federal income tax to be apportioned |

6 |

• |

|

7 |

Alabama income, page 1, line 10 |

7 |

• |

|

8a Adjusted total income, page 1, line 4 |

8a • |

|

||

8b Income excluded from Alabama Taxable Income (include any amounts listed on Schedule A lines 13, 14, 17, 18, and 19) |

8b • |

|

||

8c Adjusted Total Income including items excluded from Alabama Taxable Income (Add lines 8a and 8b) |

8c |

• |

|

|

9 |

Federal income tax ratio (divide line 7 by line 8c) |

9 |

• |

% |

10 |

Federal income tax apportioned to Alabama (multiply line 6 by line 9) |

10 |

• |

|

11 |

Less refunds or adjustments |

11 |

• |

|

12 Net federal income tax deduction / <refund> (enter here and on Page 1, line 11a) |

12 |

• |

|

|

Other Information

1.Briefly describe your Alabama operations. •

2.List locations of property within Alabama (cities and counties). •

3.List other states in which corporation operates, if applicable. •

4.Indicate your tax accounting method:

• 6 Accrual • 6 Cash • 6 Other •

5.If this corporation is a member of an affiliated group which files a consolidated federal return, the following information must be provided:

(a)Copy of Federal Form 851, Affiliations Schedule. Identify by asterisk or underline the names of those corporations subject to tax in Alabama.

(b)Signed copy of consolidated Federal Form 1120, pages

(c)Copy of the spreadsheet of income statements; all supporting schedules for all legal entities that file as part of the consolidated federal group including (but not limited to) a copy of the spreadsheet of income statements (which includes a separate column that identifies the eliminations and adjustments used in completing the federal consolidated return), beginning and ending balance sheets, Schedule

(d)Copy of federal Schedule

(e)Copy of federal Schedule(s) UTP.

6.Enter this corporation’s federal net income (see instructions for page 1, line 1) for the last three (3) years, as last determined (e.g.: per amended federal return or IRS audit).

|

2020 •___________________ |

2019 •_________________ 2018 •___________________ |

|

|

|

|

|

|

7. |

Check if currently being audited by the IRS. • 6 If so, enter the periods: •________________________________________________ |

|

|

|||||

8. |

Location of the corporate records: |

Street address: • |

|

|

|

|

|

|

|

City: • |

|

State: • |

|

|

ZIP: • |

|

|

9. |

Person to contact for information concerning this return: |

|

|

|

|

|

||

|

Name: • |

|

Email Address: • |

|

|

Telephone: • ( |

) |

|

10. |

Files Business Privilege Tax Return. • 6 |

FEIN: • |

/ |

/ |

|

/ |

/ |

|

11. |

State of Incorporation: • |

|

Date of Incorporation: • |

Date Qualified in Alabama: • |

||||

Nature of business in Alabama: •

Paid

Preparer’s

Use Only

Preparer’s signature

Firm’s name (or yours, |

• |

|

if |

• |

|

and address |

|

|

Date |

|

Preparer’s Tax Identification Number |

• |

Check if |

•6 • |

Tel. No. • ( |

) |

E.I. No. • |

|

|

ZIP Code • |

ADOR

ALABAMA 20C – 2021 |

|

PAGE 5 |

|

Alabama Department of Revenue |

Payment returns, mail with |

Alabama Department of Revenue |

|

mail to: |

Income Tax Administration Division |

payment voucher (Form |

Income Tax Administration Division |

|

Corporate Tax Section |

|

Corporate Tax Section |

|

PO Box 327430 |

|

PO Box 327435 |

|

Montgomery, AL |

|

Montgomery, AL |

Federal audit change |

|

|

|

returns, mail to: |

Alabama Department of Revenue |

|

|

|

Income Tax Administration Divisionn |

|

|

|

Corporate Tax Section |

|

|

PO Box 327451

Montgomery, AL

ADOR

| Fact Name | Fact Description |

|---|---|

| Form Title | The Alabama 20C form is officially titled the "Corporation Income Tax Return." It is used for reporting corporate income tax in Alabama. |

| Filing Period | This form is applicable for the tax year beginning January 1 and ending December 31, 2010, or for other specified tax years. |

| Governing Law | The Alabama 20C form is governed by §40-18-33 of the Code of Alabama 1975, which defines Alabama Taxable Income. |

| Filing Status | Corporations must indicate their filing status, which can include options such as single-state, multistate, or consolidated returns. |

| Net Operating Loss | Corporations can report net operating losses (NOL) on this form, specifically as outlined in §40-18-35.1 of the Code of Alabama 1975. |

| Alabama Apportionment Factor | The form requires calculation of the Alabama apportionment factor, which determines the portion of income subject to Alabama tax. |

| Signature Requirement | A signature is required from an authorized representative of the corporation, affirming the accuracy of the information provided. |

| Payment Instructions | Corporations must mail their completed 20C form along with any payment to the appropriate addresses specified by the Alabama Department of Revenue. |

Completing the Alabama 20C form requires careful attention to detail. This form is essential for corporations operating in Alabama to report their income and tax obligations. Follow these steps to fill out the form accurately.

Once you have filled out the Alabama 20C form, review it for any errors or omissions. Make sure to attach any required schedules or documentation before submitting it to the Alabama Department of Revenue. Proper filing will help avoid penalties and ensure compliance with state tax regulations.

What is the Alabama 20C form?

The Alabama 20C form is the Corporation Income Tax Return for businesses operating in Alabama. It is used to report the corporation's income, calculate the tax owed, and determine any deductions or credits applicable to the business for the tax year.

Who needs to file the Alabama 20C form?

Any corporation that conducts business in Alabama must file the Alabama 20C form. This includes corporations incorporated in Alabama as well as those incorporated in other states but doing business within Alabama. If your corporation is part of a consolidated federal return, additional information may be required.

What is the filing period for the Alabama 20C form?

The filing period for the Alabama 20C form typically runs from January 1 to December 31 of the tax year. However, corporations may also file for a different tax year by indicating the start and end dates on the form.

What information is required to complete the Alabama 20C form?

To complete the Alabama 20C form, corporations must provide their federal business code number, federal employer identification number (FEIN), filing status, name, address, state of incorporation, date of incorporation, and nature of business. Additionally, corporations must report their federal taxable income, adjustments, deductions, and credits as outlined in the form.

Are there any penalties for late filing of the Alabama 20C form?

Yes, there are penalties for late filing of the Alabama 20C form. If a corporation fails to file by the due date, it may incur penalties and interest on any unpaid tax. It is essential to file the form on time to avoid these additional charges.

Where do I send the completed Alabama 20C form?

The completed Alabama 20C form should be mailed to the Alabama Department of Revenue. Corporations must send the form to the appropriate address based on whether they are submitting a payment or a non-payment return. Specific mailing addresses are provided on the form itself.

Incorrect Filing Status Selection: Many individuals fail to accurately select the appropriate filing status. The Alabama 20C form offers several options, including "Corporation operating only in Alabama," "Multistate Corporation," and "Proforma Return." Choosing the wrong status can lead to significant errors in tax calculations and potential penalties.

Missing Federal Employer Identification Number (FEIN): Omitting the FEIN is a common mistake. This number is essential for identifying the corporation and ensuring proper processing of the return. Without it, the return may be considered incomplete.

Failure to Attach Required Schedules: The Alabama 20C form requires various schedules, such as Schedule A for reconciliation adjustments and Schedule D-1 for apportionment factors. Not including these schedules can result in delays or rejections of the return.

Incorrect Calculation of Alabama Taxable Income: Many filers miscalculate their Alabama taxable income by failing to adjust for federal net operating losses or by not properly accounting for specific additions and deductions. This can lead to incorrect tax liability assessments.

Neglecting to Sign the Return: A simple yet critical oversight is forgetting to sign the return. The signature certifies that the information provided is accurate. An unsigned return may be deemed invalid and could lead to complications with the Alabama Department of Revenue.

The Alabama 20C form is a crucial document for corporations filing their income tax returns in Alabama. Alongside this form, several other documents and forms are often required to ensure compliance with state tax regulations. Below is a list of these additional forms, each serving a specific purpose in the tax filing process.

Completing the Alabama 20C form along with the associated schedules and forms is vital for accurate tax reporting. Each document plays a significant role in ensuring that corporations fulfill their tax obligations in Alabama. Please ensure all required forms are completed accurately and submitted on time to avoid penalties.

The Alabama 20C form is a crucial document for corporations operating in Alabama, particularly for tax reporting purposes. Several other forms share similarities with the Alabama 20C, each serving specific functions in the realm of corporate taxation. Here’s a look at seven forms that are similar to the Alabama 20C, highlighting their commonalities:

Understanding these forms can help corporations navigate their tax obligations more effectively, ensuring compliance with both state and federal regulations. Each form has its unique requirements, but they all serve the common goal of accurately reporting corporate income and calculating taxes owed.

When filling out the Alabama 20C form, it is crucial to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do:

This is incorrect. The form is designed for both Alabama-only corporations and multistate corporations. Multistate corporations must complete additional sections to accurately report their income and apportionment.

In reality, filing this form is mandatory for corporations that meet certain criteria, including those generating income in Alabama. Failure to file can result in penalties.

This is not true. While there are similarities, the 20C form specifically addresses Alabama tax laws and requires adjustments to federal taxable income to determine Alabama taxable income.

This is misleading. Corporations must include necessary schedules and documentation, such as federal returns and supporting calculations, to ensure the completeness of their filing.

Actually, the due date for the Alabama 20C form may differ. Corporations should confirm the specific deadlines to avoid late fees and interest charges.

Filling out the Alabama 20C form is a critical process for corporations operating in Alabama. Here are key takeaways to guide you through this task:

By following these key points, you can navigate the complexities of the Alabama 20C form with greater confidence and accuracy.