The Additional Insured form, specifically the Commercial General Liability CG 20 37 04 13 endorsement, plays a crucial role in the realm of liability insurance. This form modifies the standard insurance policy, allowing for specific individuals or organizations to be added as additional insured parties. It primarily covers liability for bodily injury or property damage that arises from the work performed by the named insured, particularly in relation to completed operations. Key aspects of this endorsement include the requirement that the coverage provided must align with the terms of any applicable contract or agreement. Additionally, the insurance limits for the additional insured cannot exceed those outlined in the original policy or those stipulated in the contract. The form emphasizes the importance of clearly identifying the additional insured parties and the specific locations and operations covered, ensuring that all parties understand their rights and responsibilities. Understanding these nuances is essential for both insurers and insureds to navigate the complexities of liability coverage effectively.

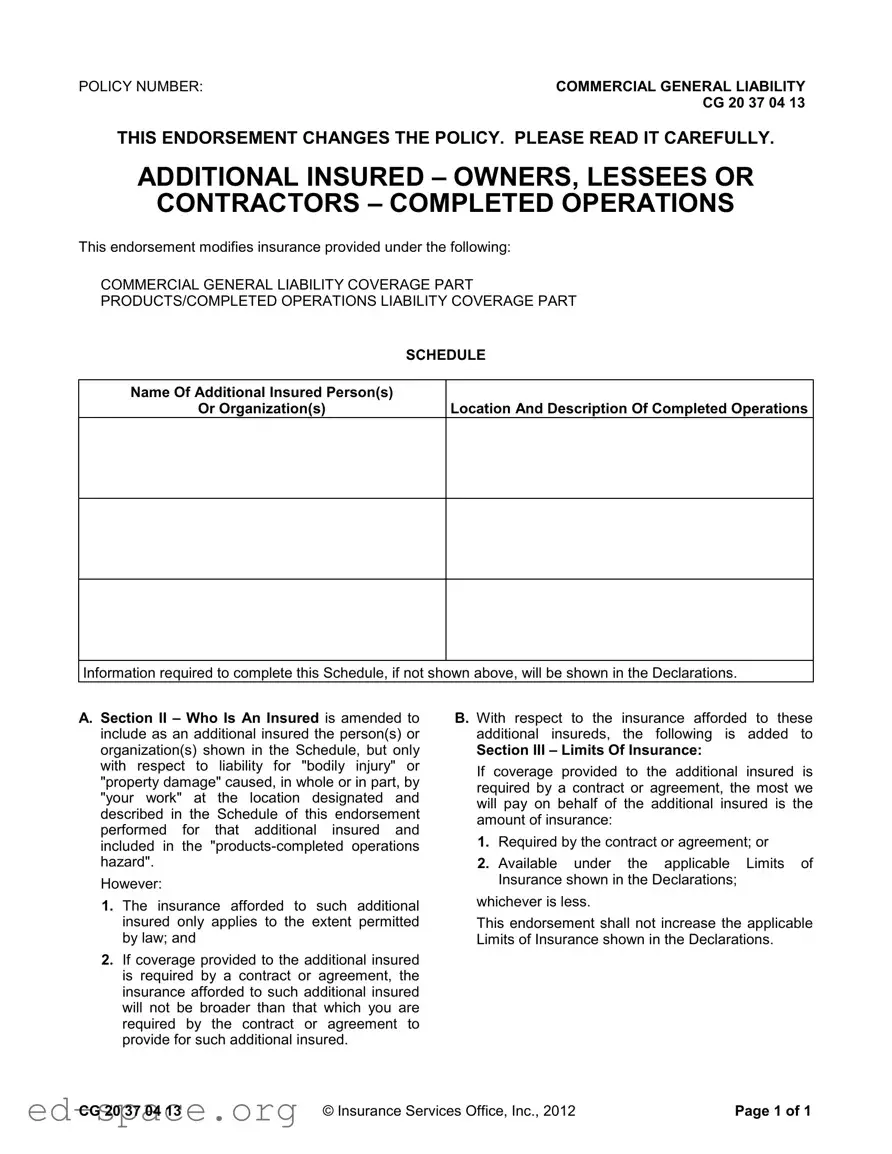

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 37 04 13 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR CONTRACTORS – COMPLETED OPERATIONS

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

PRODUCTS/COMPLETED OPERATIONS LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location And Description Of Completed Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A.Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury" or "property damage" caused, in whole or in part, by "your work" at the location designated and described in the Schedule of this endorsement performed for that additional insured and included in the

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable Limits of Insurance shown in the Declarations;

whichever is less.

This endorsement shall not increase the applicable Limits of Insurance shown in the Declarations.

CG 20 37 04 13 |

© Insurance Services Office, Inc., 2012 |

Page 1 of 1 |

| Fact Name | Description |

|---|---|

| Policy Number | The form is identified by the policy number CG 20 37 04 13. |

| Purpose | This endorsement adds additional insured status for owners, lessees, or contractors related to completed operations. |

| Modification | The endorsement modifies the insurance provided under the Commercial General Liability Coverage Part. |

| Coverage Scope | It covers liability for bodily injury or property damage caused by your work at the specified location. |

| Legal Limitations | The insurance for additional insureds applies only to the extent permitted by law. |

| Contractual Limitations | If required by contract, coverage cannot exceed what is stipulated in that agreement. |

| Insurance Limits | The maximum amount payable to an additional insured is the lesser of the contract amount or the limits shown in the Declarations. |

| Completed Operations | This endorsement specifically relates to completed operations within the products-completed operations hazard. |

| State-Specific Forms | Different states may have variations in the Additional Insured forms, governed by state-specific laws. |

| Endorsement Review | Policyholders should read the endorsement carefully to understand its implications and coverage details. |

Filling out the Additional Insured form is a straightforward process. Follow these steps carefully to ensure that all necessary information is included. Once completed, the form will help clarify the coverage details for additional insured parties related to your operations.

What is an Additional Insured form?

An Additional Insured form is a document that extends liability coverage under a primary insurance policy to another party, often required in contracts. This form is commonly used in construction and service agreements to protect owners, lessees, or contractors from claims arising from the work done by the primary insured party.

Who can be listed as an Additional Insured?

Any person or organization can be listed as an Additional Insured, provided that it is specified in the endorsement schedule. Typically, these include property owners, contractors, or other entities that may be exposed to liability from the primary insured's operations.

What types of coverage does the Additional Insured form provide?

The form provides coverage for "bodily injury" or "property damage" that occurs as a result of the primary insured's work. This coverage is applicable only for completed operations at the location described in the endorsement.

Are there limitations to the coverage provided to Additional Insureds?

Yes, the coverage for Additional Insureds is limited to the extent permitted by law. Additionally, if the coverage is required by a contract, it will not exceed the coverage specified in that contract.

What happens if the contract requires broader coverage than what is provided?

If the contract requires broader coverage than what is provided in the Additional Insured endorsement, the insurance will only cover what is stipulated in the endorsement. The coverage cannot exceed what is legally permitted or what is required by the contract.

How are the limits of insurance determined for Additional Insureds?

The limits of insurance for Additional Insureds are determined by the lesser of two amounts: the limit required by the contract or the limit available under the primary insured's policy. This means that the coverage cannot exceed either of these amounts.

Does the Additional Insured endorsement increase the overall policy limits?

No, the Additional Insured endorsement does not increase the overall policy limits. The limits remain as stated in the declarations of the primary insurance policy.

How can one obtain an Additional Insured form?

An Additional Insured form can typically be obtained from the insurance provider or agent handling the primary insured's policy. It is important to ensure that the form is completed accurately and includes all necessary information about the Additional Insured parties.

Incomplete Information: One common mistake is not filling out all required fields. The form asks for the name of the additional insured and details about the completed operations. Leaving any section blank can lead to confusion or denial of coverage.

Incorrect Names: People sometimes misspell the names of the additional insured. Even a small error can create issues when trying to enforce the policy. Always double-check the spelling and ensure that the names match official documents.

Misunderstanding Coverage Limits: Many individuals do not realize that the coverage for the additional insured cannot exceed what is required by a contract. This misunderstanding can lead to unexpected gaps in protection. It is crucial to understand the limits set forth in the contract before completing the form.

Not Reviewing the Endorsement: Failing to read the endorsement carefully is another frequent error. This document outlines important details about the coverage. Ignoring it can result in missing critical information that affects the overall insurance protection.

The Additional Insured form is a critical document in the realm of insurance, particularly in construction and contracting. It serves to extend coverage to additional parties, ensuring they are protected under the primary policy. However, several other forms and documents often accompany this endorsement to clarify responsibilities, coverage limits, and obligations. Below is a list of these documents, each serving a unique purpose.

Each of these documents plays a vital role in ensuring clarity and protection for all parties involved in a project. Understanding their purpose can significantly enhance compliance and reduce potential disputes in the future.

The Additional Insured form is a crucial document in the realm of insurance, particularly in construction and service contracts. Several other documents serve similar purposes in providing coverage and defining responsibilities. Below is a list of nine documents that share similarities with the Additional Insured form:

When filling out the Additional Insured form, it is crucial to be thorough and accurate. Here are seven essential do's and don'ts to keep in mind:

Completing the form accurately is not just a formality; it is essential for protecting yourself and your business. Take the time to review each entry carefully.

Misconceptions about the Additional Insured form can lead to confusion and potential liability issues. Here are six common misconceptions:

Understanding these misconceptions can help clarify the purpose and limitations of the Additional Insured form, ensuring better risk management and compliance.

Understanding the Additional Insured form is essential for anyone involved in contracts that require additional insured coverage. Here are key takeaways to consider:

Being aware of these points can help ensure that all parties understand their coverage and responsibilities under the Additional Insured endorsement.