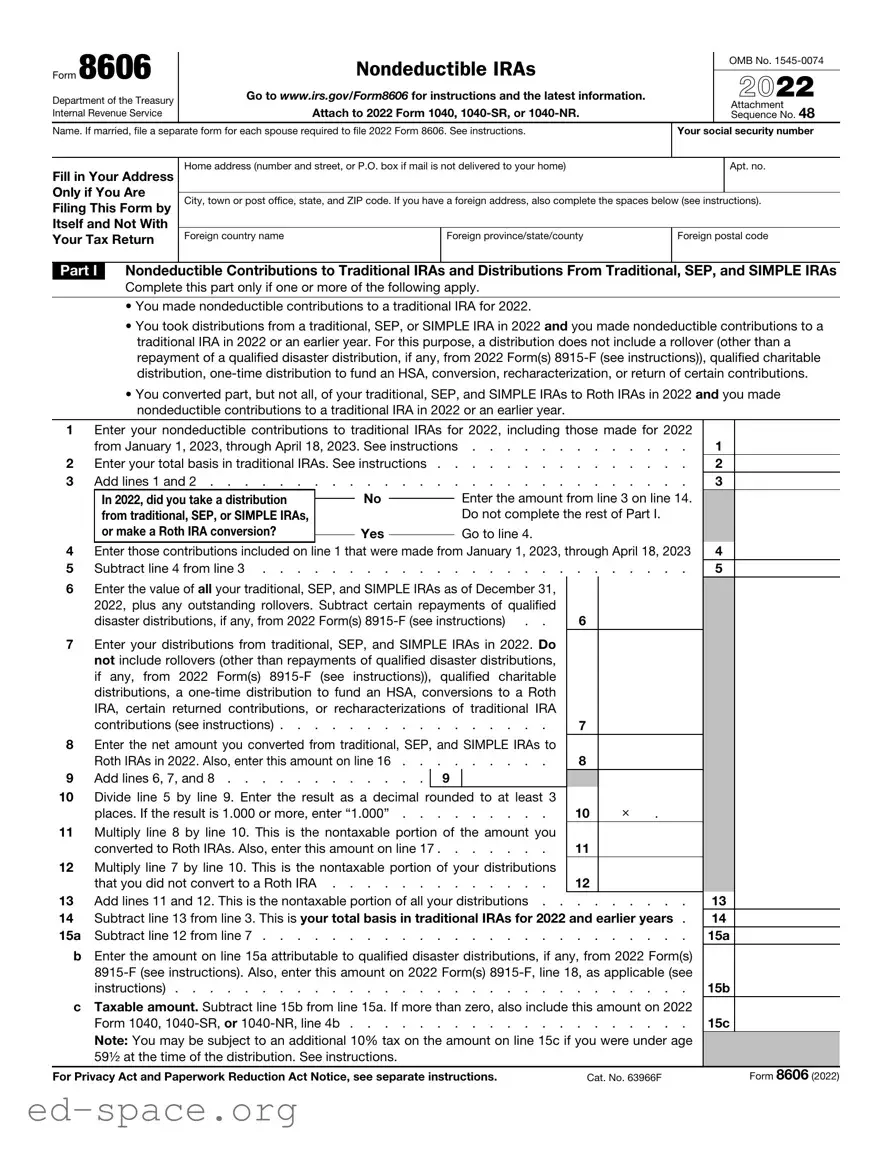

Form 8606 plays a crucial role in the realm of individual retirement accounts (IRAs), particularly for those who make nondeductible contributions. This form is essential for reporting these contributions and any distributions from traditional, SEP, or SIMPLE IRAs. If you converted a portion of your traditional IRA to a Roth IRA, you’ll also need to complete this form to track the taxable and nontaxable amounts associated with that conversion. It's important to note that if you are married and both spouses are making nondeductible contributions, each individual must file their own Form 8606. The form also addresses distributions from Roth IRAs, ensuring that individuals can accurately report any nonqualified distributions and their tax implications. By understanding how to properly fill out Form 8606, taxpayers can navigate the complexities of their retirement accounts while ensuring compliance with IRS regulations. Whether you're making contributions, taking distributions, or converting funds, this form is a key component of your tax reporting process.

Form 8606 |

|

Nondeductible IRAs |

|

|

OMB No. |

|

|

|

|

|

|||

|

|

2022 |

||||

Department of the Treasury |

Go to www.irs.gov/Form8606 for instructions and the latest information. |

|

||||

|

|

Attach to 2022 Form 1040, |

|

|

Attachment |

|

Internal Revenue Service |

|

|

|

Sequence No. 48 |

||

Name. If married, file a separate form for each spouse required to file 2022 Form 8606. See instructions. |

Your social security number |

|||||

|

|

|

|

|

||

Fill in Your Address |

Home address (number and street, or P.O. box if mail is not delivered to your home) |

|

|

Apt. no. |

||

Only if You Are |

|

|

|

|

|

|

City, town or post office, state, and ZIP code. If you have a foreign address, also complete the spaces below (see instructions). |

||||||

Filing This Form by |

||||||

Itself and Not With |

|

|

|

|

|

|

Foreign country name |

Foreign province/state/county |

Foreign postal code |

||||

Your Tax Return |

||||||

Part I Nondeductible Contributions to Traditional IRAs and Distributions From Traditional, SEP, and SIMPLE IRAs

Complete this part only if one or more of the following apply.

• You made nondeductible contributions to a traditional IRA for 2022.

• You took distributions from a traditional, SEP, or SIMPLE IRA in 2022 and you made nondeductible contributions to a traditional IRA in 2022 or an earlier year. For this purpose, a distribution does not include a rollover (other than a repayment of a qualified disaster distribution, if any, from 2022 Form(s)

• You converted part, but not all, of your traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2022 and you made nondeductible contributions to a traditional IRA in 2022 or an earlier year.

1 |

Enter your nondeductible contributions to traditional IRAs for 2022, including those made for 2022 |

|

|

|||||

|

from January 1, 2023, through April 18, 2023. See instructions |

. . . . . . . . . . . . . |

1 |

|

||||

2 |

Enter your total basis in traditional IRAs. See instructions . . |

. . . . . . . . . . . . . |

2 |

|

||||

3 |

Add lines 1 and 2 |

. . . . . . . . . . . . . |

3 |

|

||||

|

In 2022, did you take a distribution |

|

No |

|

|

Enter the amount from line 3 on line 14. |

|

|

|

|

|

|

|

||||

|

from traditional, SEP, or SIMPLE IRAs, |

|

|

|

|

Do not complete the rest of Part I. |

|

|

4 |

or make a Roth IRA conversion? |

|

Yes |

|

|

Go to line 4. |

|

|

|

|

|

|

|||||

Enter those contributions included on line 1 that were made from January 1, 2023, through April 18, 2023 |

4 |

|

||||||

5 |

Subtract line 4 from line 3 |

. . . . . . . . . . . . . |

5 |

|

||||

6Enter the value of all your traditional, SEP, and SIMPLE IRAs as of December 31, 2022, plus any outstanding rollovers. Subtract certain repayments of qualified

disaster distributions, if any, from 2022 Form(s) |

6 |

7Enter your distributions from traditional, SEP, and SIMPLE IRAs in 2022. Do not include rollovers (other than repayments of qualified disaster distributions, if any, from 2022 Form(s)

IRA, certain returned contributions, or recharacterizations of traditional |

IRA |

|

contributions (see instructions) |

. |

7 |

8Enter the net amount you converted from traditional, SEP, and SIMPLE IRAs to

Roth IRAs in 2022. Also, enter this amount on line 16 . . |

. . . . . . . |

8 |

|

|

9 Add lines 6, 7, and 8 |

9 |

|

|

|

10Divide line 5 by line 9. Enter the result as a decimal rounded to at least 3

places. If the result is 1.000 or more, enter “1.000” |

10 |

× |

. |

11Multiply line 8 by line 10. This is the nontaxable portion of the amount you

converted to Roth IRAs. Also, enter this amount on line 17 |

11 |

12Multiply line 7 by line 10. This is the nontaxable portion of your distributions

|

that you did not convert to a Roth IRA |

12 |

|

|

13 |

Add lines 11 and 12. This is the nontaxable portion of all your distributions |

|

13 |

|

14 |

Subtract line 13 from line 3. This is your total basis in traditional IRAs for 2022 and earlier years . |

|

14 |

|

15a |

Subtract line 12 from line 7 |

15a |

||

bEnter the amount on line 15a attributable to qualified disaster distributions, if any, from 2022 Form(s)

instructions) |

15b |

cTaxable amount. Subtract line 15b from line 15a. If more than zero, also include this amount on 2022 Form 1040,

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 63966F |

Form 8606 (2022) |

Form 8606 (2022) |

Page 2 |

Part II 2022 Conversions From Traditional, SEP, or SIMPLE IRAs to Roth IRAs

Complete this part if you converted part or all of your traditional, SEP, and SIMPLE IRAs to a Roth IRA in 2022.

16If you completed Part I, enter the amount from line 8. Otherwise, enter the net amount you converted

from traditional, SEP, and SIMPLE IRAs to Roth IRAs in 2022 . . . . . . . . . . . . .

17If you completed Part I, enter the amount from line 11. Otherwise, enter your basis in the amount on

line 16 (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . .

18Taxable amount. Subtract line 17 from line 16. If more than zero, also include this amount on 2022 Form 1040,

Part III Distributions From Roth IRAs

16

17

18

Complete this part only if you took a distribution from a Roth IRA in 2022. For this purpose, a distribution does not include a rollover (other than a repayment of a qualified disaster distribution (from 2022 Form(s)

19 |

Enter your total nonqualified distributions from Roth IRAs in 2022, including any qualified |

|

|

|||||||||

|

homebuyer distributions, and any qualified disaster distributions from 2022 Form(s) |

|

|

|||||||||

|

instructions) |

. . . . |

19 |

|

||||||||

20 |

Qualified |

|

|

|||||||||

|

by the total of all your prior qualified |

. . . . |

20 |

|

||||||||

21 |

Subtract line 20 from line 19. If zero or less, enter |

. . . . |

21 |

|

||||||||

22 |

Enter your basis in Roth IRA contributions (see instructions). If line 21 is zero, stop here . |

. . . . |

22 |

|

||||||||

23 |

Subtract line 22 from line 21. If zero or less, enter |

|

|

|||||||||

|

may be subject to an additional tax (see instructions) |

. . . . |

23 |

|

||||||||

24 |

Enter your basis in conversions from traditional, SEP, and SIMPLE IRAs and rollovers from qualified |

|

|

|||||||||

|

retirement plans to a Roth IRA. See instructions |

. . . . |

24 |

|

||||||||

25a |

Subtract line 24 from line 23. If zero or less, enter |

. . . . |

25a |

|

||||||||

b Enter the amount on line 25a attributable to qualified disaster distributions, if any, from 2022 Form(s) |

|

|

||||||||||

|

|

|

||||||||||

|

instructions) |

. . . . |

25b |

|

||||||||

c |

Taxable amount. Subtract line 25b from line 25a. If more than zero, also include this amount on 2022 |

|

|

|||||||||

|

Form 1040, |

. . . . |

25c |

|

||||||||

Sign Here Only if You |

Under penalties of perjury, I declare that I have examined this form, including accompanying attachments, and to the best of my knowledge and |

|||||||||||

Are Filing This Form |

belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|||

by Itself and Not With |

|

|

|

|

|

|

|

|

|

|

||

Your Tax Return |

|

|

|

|

|

|

|

|

|

|

||

|

Your signature |

|

|

|

|

Date |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

Print/Type preparer’s name |

Preparer’s signature |

Date |

|

|

|

Check |

if |

PTIN |

||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

Firm’s name |

|

|

|

|

|

|

|

Firm’s EIN |

|

|||

Use Only |

|

|

|

|

|

|

|

|

||||

Firm’s address |

|

|

|

|

|

Phone no. |

|

|||||

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Form 8606 (2022) |

| Fact Name | Description |

|---|---|

| Purpose | Form 8606 is used to report nondeductible contributions to traditional IRAs and distributions from traditional, SEP, and SIMPLE IRAs. |

| Filing Requirement | This form must be attached to the 2022 Form 1040, 1040-SR, or 1040-NR when filing your tax return. |

| Multiple Filings | If married and filing separately, each spouse must file their own Form 8606. |

| Conversions | Part II of the form addresses conversions from traditional IRAs to Roth IRAs, detailing taxable amounts. |

| State-Specific Forms | Some states may have their own forms or requirements related to IRAs. Check state laws for specifics. |

Completing Form 8606 is essential for reporting nondeductible contributions to traditional IRAs and distributions from various retirement accounts. This form must be attached to your tax return for the year you are filing. Ensure all information is accurate and complete to avoid delays in processing your return.

What is Form 8606?

Form 8606 is a tax form used to report nondeductible contributions to traditional Individual Retirement Accounts (IRAs), distributions from traditional, SEP, and SIMPLE IRAs, and conversions from these accounts to Roth IRAs. It helps taxpayers track their basis in these accounts to determine the taxable amount of distributions and conversions.

Who needs to file Form 8606?

Taxpayers must file Form 8606 if they made nondeductible contributions to a traditional IRA, took distributions from traditional, SEP, or SIMPLE IRAs, or converted any part of these accounts to Roth IRAs during the tax year. If married, each spouse must file a separate form if they both have such contributions or distributions.

What information is required to complete Form 8606?

To complete Form 8606, individuals will need to provide their name, social security number, and address. Additionally, they must report nondeductible contributions made during the tax year, the total basis in traditional IRAs, and details about any distributions or conversions that occurred. This includes values as of December 31 of the tax year and any relevant amounts from prior years.

What are nondeductible contributions?

Nondeductible contributions are contributions made to a traditional IRA for which the taxpayer does not receive a tax deduction. These contributions are important to track because they represent the taxpayer's basis in the IRA, which affects the taxation of future distributions and conversions to Roth IRAs.

How does Form 8606 affect my taxes?

Form 8606 plays a crucial role in determining the taxable portion of distributions and conversions from IRAs. By accurately reporting nondeductible contributions, taxpayers can avoid being taxed again on those amounts when they take distributions or convert to a Roth IRA. Failure to file this form when required may result in additional taxes and penalties.

When is Form 8606 due?

Form 8606 is due on the same date as the taxpayer's income tax return, typically April 15. If an extension is filed for the tax return, the same extension applies to Form 8606. It must be attached to the taxpayer's Form 1040, 1040-SR, or 1040-NR when submitted.

What happens if I don’t file Form 8606 when required?

If a taxpayer fails to file Form 8606 when required, they may face a penalty of $50 for each form not filed. Additionally, the IRS may impose taxes on amounts that should have been reported as nondeductible contributions, leading to double taxation on those funds when distributions are taken.

Incorrectly Reporting Nondeductible Contributions: Many individuals fail to accurately report their nondeductible contributions to traditional IRAs. This can lead to discrepancies in tax calculations and potential penalties.

Neglecting to Include All Required Information: Some people overlook essential information, such as their Social Security number or the correct filing status. This omission can delay processing and result in additional scrutiny from the IRS.

Improperly Calculating Taxable Amounts: Errors often occur when calculating the taxable amounts related to conversions or distributions. Miscalculating these figures can lead to an unexpected tax liability.

Failing to Attach the Form: A common mistake is not attaching Form 8606 to the main tax return. This oversight can result in the IRS not recognizing the nondeductible contributions, leading to potential penalties.

The Form 8606 is an essential document for individuals who make nondeductible contributions to traditional IRAs or convert their traditional IRAs to Roth IRAs. However, it is often accompanied by other forms that provide additional information or context regarding the taxpayer's financial situation. Understanding these related documents can enhance your grasp of the overall tax implications associated with retirement accounts.

In summary, while Form 8606 plays a pivotal role in reporting nondeductible IRA contributions and conversions, it is often used in conjunction with other forms. Each of these documents serves a unique purpose, providing essential information that supports the accurate reporting of retirement account transactions and ensures compliance with tax regulations.

Filling out Form 8606 can be a straightforward process if you know what to do and what to avoid. Here’s a handy list to help you navigate this form effectively.

By keeping these tips in mind, you can fill out Form 8606 with confidence and accuracy. Remember, attention to detail is key!

Understanding Form 8606 can be challenging, and several misconceptions can lead to confusion when filing taxes. Here are five common misunderstandings about this form:

This is not true. Anyone who makes nondeductible contributions to a traditional IRA or takes distributions from traditional IRAs must file this form, regardless of income level.

While it is often attached to your tax return, you can also file Form 8606 by itself if necessary. It's important to ensure that it is submitted correctly, even if not filed with the main tax forms.

This is a common error. Filing Form 8606 is required to report nondeductible contributions. Failing to do so can lead to complications, including tax penalties.

In fact, Form 8606 is essential for reporting conversions from traditional IRAs to Roth IRAs. It helps track the taxable and nontaxable portions of your conversions.

This is misleading. The basis reported on Form 8606 carries over to future years and is crucial for determining taxable amounts in subsequent distributions or conversions.

Here are some key takeaways about filling out and using Form 8606: