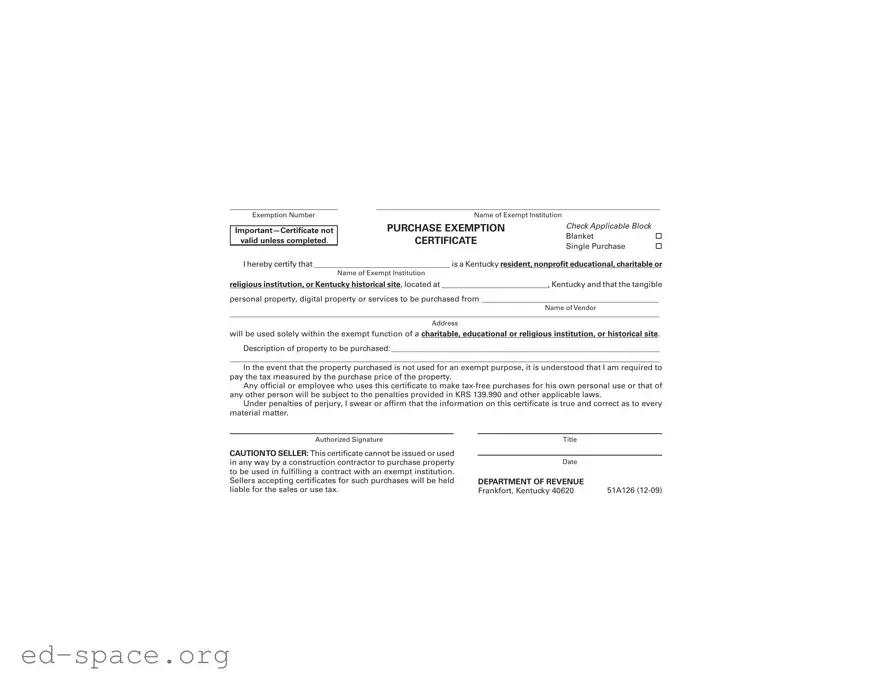

The 51A126 form plays a crucial role in facilitating tax-exempt purchases for specific organizations in Kentucky. This certificate is designed for use by nonprofit educational, charitable, or religious institutions, as well as historical sites within the state. To utilize this form, the exempt institution must provide its name and address, along with details about the vendor from whom it intends to make a purchase. The form allows for either a blanket exemption or a single purchase exemption, depending on the needs of the institution. Importantly, the tangible personal property, digital property, or services acquired using this certificate must be used solely for the exempt purpose of the organization. If the property is not utilized as intended, the institution is responsible for paying the applicable sales tax based on the purchase price. Furthermore, the form contains a cautionary note for sellers, emphasizing that this certificate cannot be employed by construction contractors for purchases related to contracts with exempt institutions. Compliance with the regulations surrounding this certificate is essential, as misuse can lead to significant penalties under Kentucky law.

Exemption Number

valid unless completed.

Name of Exempt Institution |

|

|

PURCHASE EXEMPTION |

Check Applicable Block |

|

CERTIFICATE |

Blanket |

|

Single Purchase |

||

|

I hereby certify that ___________________________________ is a Kentucky resident, nonprofit educational, charitable or

Name of Exempt Institution

religious institution, or Kentucky historical site, located at ___________________________, Kentucky and that the tangible

personal property, digital property or services to be purchased from _____________________________________________

Name of Vendor

_____________________________________________________________________________________________________________

Address

will be used solely within the exempt function of a charitable, educational or religious institution, or historical site.

Description of property to be purchased: ____________________________________________________________________

_____________________________________________________________________________________________________________

In the event that the property purchased is not used for an exempt purpose, it is understood that I am required to pay the tax measured by the purchase price of the property.

Any official or employee who uses this certificate to make

Under penalties of perjury, I swear or affirm that the information on this certificate is true and correct as to every material matter.

Authorized Signature

CAUTIONTO SELLER: This certificate cannot be issued or used in any way by a construction contractor to purchase property to be used in fulfilling a contract with an exempt institution. Sellers accepting certificates for such purchases will be held liable for the sales or use tax.

Title

Date |

|

DEPARTMENT OF REVENUE |

|

Frankfort, Kentucky 40620 |

51A126 |

| Fact Name | Details |

|---|---|

| Form Title | 51A126 Exemption Certificate |

| Governing Law | Kentucky Revised Statutes (KRS) 139.990 |

| Purpose | To certify that purchases made by qualifying institutions are exempt from sales tax. |

| Eligible Institutions | Nonprofit educational, charitable, or religious institutions, and historical sites located in Kentucky. |

| Usage Requirement | Purchased items must be used solely for exempt functions of the institution. |

| Penalties for Misuse | Using the certificate for personal purchases can result in penalties as outlined in KRS 139.990. |

| Seller's Responsibility | Sellers must ensure the certificate is valid and cannot accept it for construction-related purchases. |

After completing the 51A126 form, ensure that all information is accurate and legible. This form must be submitted to the vendor to qualify for the tax exemption. Follow the steps below to fill out the form correctly.

What is the 51A126 form used for?

The 51A126 form is a certificate used by certain exempt institutions in Kentucky to make tax-free purchases. This includes nonprofit educational, charitable, or religious institutions, as well as Kentucky historical sites. The form certifies that the items purchased will be used solely for exempt purposes.

Who can use the 51A126 form?

Only authorized representatives of qualified institutions can use the 51A126 form. This includes individuals from nonprofit educational, charitable, or religious organizations, as well as historical sites located in Kentucky. The form must be completed accurately to be valid.

What information is required on the 51A126 form?

The form requires several key pieces of information. You must provide the name and address of the exempt institution, the name and address of the vendor, and a description of the property being purchased. Additionally, the authorized representative must sign the form, affirming the accuracy of the information provided.

What happens if the purchased items are not used for exempt purposes?

If the tangible personal property, digital property, or services purchased with the 51A126 form are not used for exempt purposes, the institution is responsible for paying the sales tax based on the purchase price. This is an important consideration to ensure compliance with tax regulations.

Are there any penalties for misuse of the 51A126 form?

Yes, there are penalties for misuse. If an official or employee uses the 51A126 form to make tax-free purchases for personal use or for someone else's benefit, they may face penalties as outlined in KRS 139.990 and other applicable laws. It is crucial to use the form strictly for its intended purpose.

Can construction contractors use the 51A126 form?

No, construction contractors cannot use the 51A126 form to purchase property for fulfilling contracts with exempt institutions. If a seller accepts this certificate for such purchases, they will be held liable for the sales or use tax. It is important for sellers to verify the legitimacy of the certificate before proceeding with tax-free transactions.

How often can the 51A126 form be used?

The 51A126 form can be used for both blanket and single purchases, depending on the needs of the exempt institution. However, each use must comply with the rules governing tax-exempt purchases. Institutions should keep accurate records of all transactions made using this certificate.

Leaving the Exemption Number Blank: This form requires an exemption number. Without it, the certificate is invalid.

Incorrectly Identifying the Institution: Make sure to accurately name the exempt institution. Errors here can lead to complications.

Not Specifying the Purchase Type: Check the appropriate box for either Blanket or Single Purchase. Failing to do so can cause confusion.

Missing the Vendor's Information: It's essential to provide the full name and address of the vendor. Omitting this can invalidate the form.

Vague Description of Property: Clearly describe the property being purchased. A vague description can lead to misunderstandings regarding the exemption.

Ignoring the Tax Consequences: Understand that if the property is not used for exempt purposes, tax must be paid. This is a crucial responsibility.

Signature Issues: Ensure the authorized signature is included. A missing signature can render the certificate invalid.

Failure to Understand Limitations: Be aware that this certificate cannot be used by construction contractors for purchases related to their contracts. Misuse can lead to penalties.

The 51A126 form is used in Kentucky to certify that certain purchases made by nonprofit organizations are exempt from sales tax. It is important to understand that this form is often accompanied by other documents that may be necessary for various transactions. Below is a list of commonly used forms and documents that may accompany the 51A126 form.

Understanding these documents can help ensure compliance with tax regulations and facilitate smoother transactions for exempt organizations. Always keep accurate records and consult with a tax professional if there are any uncertainties regarding the use of these forms.

The 51A126 form is a tax exemption certificate used by certain nonprofit organizations in Kentucky. Several other documents serve similar purposes, allowing for tax exemptions under specific conditions. Here’s a list of eight documents that are comparable to the 51A126 form:

When filling out the 51A126 form, it is important to follow certain guidelines to ensure compliance and avoid issues. Here are nine things you should and shouldn't do:

Following these guidelines will help ensure that your form is completed correctly and used appropriately.

Here are seven common misconceptions about the 51A126 form:

When filling out and using the 51A126 form, it’s important to keep several key points in mind. This form is primarily used by nonprofit educational, charitable, or religious institutions in Kentucky to make tax-exempt purchases. Here are the essential takeaways:

Following these guidelines will help ensure that your use of the 51A126 form is compliant and effective. Always keep a copy for your records and consult with a legal advisor if you have any questions about your specific situation.