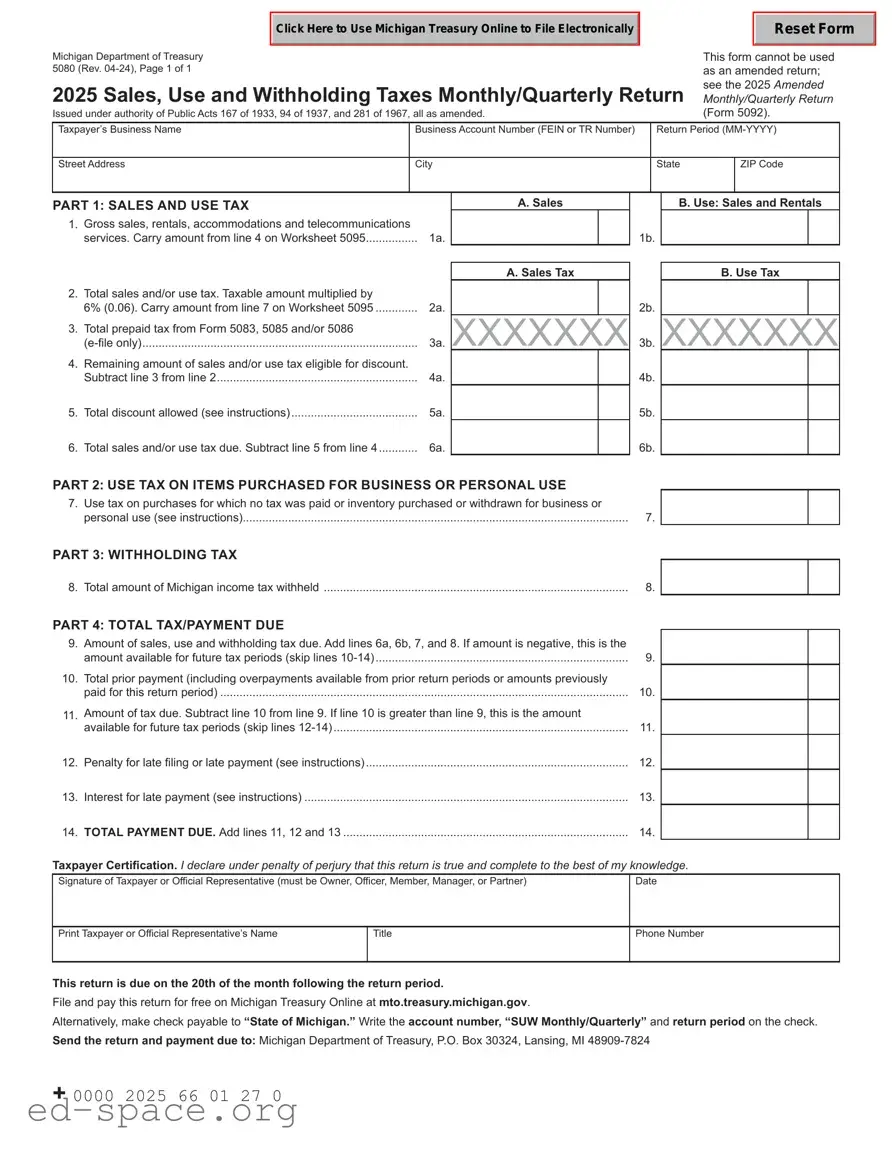

The Michigan Department of Treasury Form 5080 is a crucial document for businesses operating within the state, serving as the monthly or quarterly return for sales, use, and withholding taxes. This form is issued under the authority of Public Acts 167 of 1933 and 94 of 1937, and it plays a vital role in ensuring compliance with tax obligations. Businesses must accurately report their gross sales, rentals, and services, which include both cash and credit transactions. The form also requires taxpayers to calculate the total sales and use tax due, applying the standard rate of 6%. Additionally, it allows for the reporting of any pre-paid taxes and provides a mechanism for claiming allowable discounts based on filing frequency. The form encompasses various sections, including a breakdown of use tax on items purchased for business or personal use, as well as withholding tax details. Completing this form accurately is essential, as any discrepancies can lead to penalties and interest charges. Thus, understanding the components of Form 5080 is imperative for business owners to maintain compliance and avoid potential liabilities.

Click Here to Use Michigan Treasury Online to File Electronically

Michigan Department of Treasury

5080 (Rev.

2025 Sales, Use and Withholding Taxes Monthly/Quarterly Return

Issued under authority of Public Acts 167 of 1933, 94 of 1937, and 281 of 1967, all as amended.

Reset Form

This form cannot be used as an amended return; see the 2025 Amended

Monthly/Quarterly Return (Form 5092).

Taxpayer’s Business Name |

Business Account Number (FEIN or TR Number) |

Return Period |

||||

|

|

|

|

|||

Street Address |

City |

State |

ZIP Code |

|||

|

|

|

|

|

|

|

PART 1: SALES AND USE TAX |

|

A. Sales |

|

|

B. Use: Sales and Rentals |

|

1.Gross sales, rentals, accommodations and telecommunications

services. Carry amount from line 4 on Worksheet 5095 |

1a. |

1b. |

2. |

Total sales and/or use tax. Taxable amount multiplied by |

|

|

6% (0.06). Carry amount from line 7 on Worksheet 5095 |

2a. |

3. |

Total prepaid tax from Form 5083, 5085 and/or 5086 |

|

|

3a. |

|

4. |

Remaining amount of sales and/or use tax eligible for discount. |

|

|

Subtract line 3 from line 2 |

4a. |

5. |

Total discount allowed (see instructions) |

5a. |

6. |

Total sales and/or use tax due. Subtract line 5 from line 4 |

6a. |

A. Sales Tax

XXXXXXX

2b.

3b.

4b.

5b.

6b.

B. Use Tax

XXXXXXX

PART 2: USE TAX ON ITEMS PURCHASED FOR BUSINESS OR PERSONAL USE

7. Use tax on purchases for which no tax was paid or inventory purchased or withdrawn for business or |

|

personal use (see instructions) |

7. |

PART 3: WITHHOLDING TAX

8. Total amount of Michigan income tax withheld |

8. |

PART 4: TOTAL TAX/PAYMENT DUE

9. |

Amount of sales, use and withholding tax due. Add lines 6a, 6b, 7, and 8. If amount is negative, this is the |

|

|

amount available for future tax periods (skip lines |

9. |

10. |

Total prior payment (including overpayments available from prior return periods or amounts previously |

|

|

paid for this return period) |

10. |

11. |

Amount of tax due. Subtract line 10 from line 9. If line 10 is greater than line 9, this is the amount |

11. |

|

available for future tax periods (skip lines |

|

12. |

Penalty for late filing or late payment (see instructions) |

12. |

13. |

Interest for late payment (see instructions) |

13. |

14. |

TOTAL PAYMENT DUE. Add lines 11, 12 and 13 |

14. |

Taxpayer Certification. I declare under penalty of perjury that this return is true and complete to the best of my knowledge.

Signature of Taxpayer or Official Representative (must be Owner, Officer, Member, Manager, or Partner)

Date

Print Taxpayer or Official Representative’s Name

Title

Phone Number

This return is due on the 20th of the month following the return period.

File and pay this return for free on Michigan Treasury Online at mto.treasury.michigan.gov.

Alternatively, make check payable to “State of Michigan.” Write the account number, “SUW Monthly/Quarterly” and return period on the check. Send the return and payment due to: Michigan Department of Treasury, P.O. Box 30324, Lansing, MI

+ 0000 2025 66 01 27 0

2025 Form 5080, Page 2

Instructions for 2025 Sales, Use and Withholding Taxes Monthly/Quarterly Return (Form 5080)

Form 5080 is available for submission electronically using Michigan Treasury Online (MTO) at mto.treasury.michigan.gov or by using approved tax preparation software.

NOTE: The address field on this form is required to be completed but will not be used to replace an existing valid address for the purpose of correspondence or refunds. Update address and other registration information using MTO or mail a completed Notice of Change or Discontinuance (Form 163).

IMPORTANT: This is a return for sales tax, use tax and/or withholding tax. If the taxpayer inserts a zero on or leaves blank any line reporting sales tax, use tax or withholding tax, the taxpayer is certifying that no tax is owed for that tax type. Only enter figures for taxes the business is registered and/or liable for. If it is determined that tax is owed the taxpayer will be liable for the deficiency as well as penalty and interest. Complete the Sales, Use and Withholding Taxes Monthly/Quarterly

and Amended Monthly/Quarterly Worksheet

(Form 5095, hereafter referred to as Worksheet 5095) prior to completing this form.

PART 1: SALES AND USE TAX

Line 1a: Enter the amount from Worksheet 5095, line 4A.

Line 1b: Enter the amount from Worksheet 5095, line 4B.

Line 2a: Total Sales Tax. Negative figures are not allowed. Enter the amount from Worksheet 5095, line 7A. Gross sales minus allowable deductions, multiplied by 6%

Line 2b: Total Use Tax. Negative figures not allowed. Enter the amount from Worksheet 5095, line 7B. Total receipts from sales, rentals, and services, minus allowable deductions, multiplied by 6%.

Line 5: Total Discount Allowed for Timely Filing and Payment. Discounts apply only to 2/3 (0.6667) of the sales and/or use tax collected at the 6 percent tax rate. See below to calculate the discount:

Monthly Filer

•If the tax is less than $9, calculate the discount by multiplying the tax by 2/3 (.6667).

•If tax is $9 to $1,200 and paid by the 12th, or $9 to $1,800 and paid by the 20th, then enter $6.

•If the tax is more than $1,200 and paid by the 12th,

calculate discount using this formula: (Tax x .6667 x .0075). The maximum discount is $20,000 for the tax period.

• If the tax is more than $1,800 and paid by the 20th,

calculate discount using this formula: (Tax x .6667 x .005). The maximum discount is $15,000 for the tax period.

Quarterly Filer

•If the tax is less than $27, calculate the discount by multiplying the tax by 2/3 (.6667).

•If tax is $27 to $3,600 and paid by the 12th, or $27 to $5,400 and paid by the 20th, then enter $18.

•If the tax is more than $3,600 and paid by the 12th,

calculate discount using this formula: (Tax x .6667 x .0075). The maximum discount is $20,000 for the tax period.

• If the tax is more than $5,400 and paid by the 20th,

calculate discount using this formula: (Tax x .6667 x .005). The maximum discount is $15,000 for the tax period.

Accelerated Filer

•If the tax is paid by the 20th, calculate discount using this formula: (Tax x .6667 x .005). No maximum discount applies.

Credit Schedules

•

PART 2: USE TAX ON ITEMS PURCHASED FOR BUSINESS OR PERSONAL USE

Line 7: Enter the amount from Worksheet 5095, line 9. To determine use tax due from purchases and withdrawals, multiply the applicable tax base by 6%.

PART 3: WITHHOLDING TAX

Line 8: Enter the total Michigan income tax withheld for the tax period.

PART 4: TOTAL TAX/PAYMENT DUE

Line 9: If amount is negative, this is the amount available for future tax periods (skip lines

Line 10: Enter any payments submitted for this period prior to filing the return or any overpayment from prior periods. Liability minus prior/over payments for this period must be greater than or equal to zero.

Line 14: Total Payment Due. Add lines 11, 12 and 13. Submit payments electronically on MTO, or make check payable to the “State of Michigan” and remit with your return. Write the account number, “SUW Monthly/ Quarterly” and the return period on the check. Do not pay if the amount due is less than $1.

2025 Form 5080, Page 3

HOW TO COMPUTE PENALTY AND INTEREST

If the return is filed late with tax due, include penalty and interest with the payment. Penalty is 5% of the tax due and increases by an additional 5% per month or fraction thereof, after the second month, to a maximum of 25%. Interest is charged daily using the average prime rate, plus 1 percent.

Visit www.michigan.gov/taxes for current interest rate information or help in calculating late payment penalties.

Tax Assistance

For assistance, call

| Fact Name | Fact Details |

|---|---|

| Form Title | Michigan Department of Treasury 5080 (07-14) 2015 Sales, Use and Withholding Taxes Monthly/Quarterly Return |

| Governing Laws | Issued under authority of Public Acts 167 of 1933 and 94 of 1937, as amended. |

| Amended Return | This form cannot be used as an amended return; refer to Amended Monthly/Quarterly Return (Form 5092). |

| Tax Types | This return covers Sales Tax, Use Tax, and Withholding Tax. |

| Discount Eligibility | Taxpayers may be eligible for discounts based on filing frequency and amount of tax due. |

| Certification Requirement | Taxpayer must certify under penalty of perjury that the return is true and complete. |

| Payment Instructions | Make checks payable to “State of Michigan” and include the account number. |

| Submission Address | Returns and payments should be sent to Michigan Department of Treasury, P.O. Box 30324, Lansing, MI 48909-7824. |

Completing the Michigan Department of Treasury Form 5080 is essential for reporting your sales, use, and withholding taxes accurately. This form requires careful attention to detail, as any errors could lead to penalties or interest charges. Below are the steps to help you fill out the form correctly.

Part 1: Sales and Use Tax

Part 2: Use Tax on Items Purchased for Business or Personal Use

Part 3: Withholding Tax

Part 4: Total Tax/Payment Due

Finally, ensure you sign and date the form where indicated. Make your check payable to “State of Michigan,” including your account number, and send your completed return along with any payment to the Michigan Department of Treasury at the specified address. Taking these steps carefully will help ensure compliance and avoid unnecessary complications.

What is the Michigan Department of Treasury 5080 form used for?

The Michigan Department of Treasury 5080 form is utilized for reporting Sales Tax, Use Tax, and Withholding Tax. It serves as a monthly or quarterly return for businesses to declare their tax liabilities and make payments to the state. Completing this form accurately is essential for compliance with Michigan tax laws.

Who needs to file the 5080 form?

Any business operating in Michigan that collects sales tax, uses taxable items, or withholds income tax from employees is required to file the 5080 form. This includes retailers, service providers, and businesses that rent or lease tangible personal property. If your business falls into any of these categories, you must submit this form according to your designated filing frequency.

How do I determine my total sales and use tax?

To calculate your total sales and use tax, first, sum your gross sales, rentals, and services. This includes all cash, credit, and installment transactions. Then, multiply the taxable amount by 6% (0.06). This will give you the total sales and use tax before any discounts or pre-paid tax considerations.

What are allowable discounts on the 5080 form?

Allowable discounts can significantly reduce your tax liability. The discount is calculated based on the amount of sales and use tax eligible for discount after subtracting any pre-paid tax. The discount rate varies depending on your filing frequency and the amount of tax due. For example, monthly filers with tax less than $9 can calculate the discount by multiplying the tax by 2/3. It's essential to understand these rates to maximize your savings.

What should I do if I have an overpayment?

If you have an overpayment from a prior return period, you can apply that amount to your current tax liability. Simply enter the overpayment on the designated line of the 5080 form. If the overpayment exceeds your current liability, note that the remaining amount can be declared on your next return.

What happens if I file my return late?

Filing your return late can lead to penalties and interest charges. The penalty starts at 5% of the tax due and increases by an additional 5% for each month or part of a month after the second month, capping at 25%. Additionally, interest is charged daily based on the average prime rate plus 1%. To avoid these costs, it’s best to file your return on time.

Can I use the 5080 form to amend a previous return?

No, the 5080 form cannot be used to amend a previously filed return. If you need to make corrections to a prior submission, you must use the Amended Monthly/Quarterly Return (Form 5092) instead. This ensures that your amendments are processed correctly by the Michigan Department of Treasury.

How do I submit my payment for the 5080 form?

When submitting your payment, make your check payable to “State of Michigan” and include your account number on the check. Send your completed form and payment to the Michigan Department of Treasury at the specified address: P.O. Box 30324, Lansing, MI 48909-7824. Ensure your payment is sent in a timely manner to avoid penalties.

Where can I find additional information or assistance regarding the 5080 form?

For further information or assistance, visit the Michigan Department of Treasury's official website at www.michigan.gov/taxes. Here, you can find resources, current interest rates, and additional guidance to help you navigate the tax filing process effectively.

Inaccurate Business Information: Failing to provide the correct business name or account number can lead to significant issues. It is essential to ensure that the information matches the records held by the Michigan Department of Treasury.

Missing Signature: The form requires a signature from the taxpayer or an authorized representative. Omitting this step can result in the return being deemed invalid.

Incorrect Tax Calculations: Errors in calculating gross sales, use tax, or withholding tax can lead to underreporting or overreporting. Always double-check calculations to ensure accuracy.

Neglecting Discount Eligibility: Not taking into account any applicable discounts can lead to paying more tax than necessary. Familiarize yourself with the discount formulas based on filing frequency.

Skipping Lines: Failing to fill out all required lines, particularly those that apply to your specific tax situation, can result in incomplete information and potential penalties.

Incorrect Reporting Period: Entering the wrong return period can cause confusion and may lead to issues with the Department of Treasury. Always verify the reporting period before submission.

Failure to Keep Copies: Not retaining a copy of the submitted form for your records can be a costly mistake. Having documentation is crucial for future reference and in case of audits.

The Michigan Department of Treasury 5080 form is a crucial document for businesses, as it serves as the Sales, Use, and Withholding Taxes Monthly/Quarterly Return. However, several other forms and documents are often utilized in conjunction with the 5080 to ensure compliance with state tax regulations. Understanding these additional forms can help taxpayers navigate their obligations more effectively.

In summary, these forms and documents play vital roles in the overall tax compliance process for businesses operating in Michigan. Utilizing them correctly can help ensure that all tax obligations are met, thereby minimizing the risk of penalties and interest. Understanding the interplay between these forms and the 5080 can lead to more efficient tax management and a smoother filing experience.

When filling out the Michigan Department of Treasury 5080 form, it's essential to follow specific guidelines to ensure accuracy and compliance. Here are some important dos and don'ts:

Understanding the 5080 Michigan form can be challenging. Here are ten common misconceptions about this form, along with clarifications to help ensure accurate completion and compliance.

Being aware of these misconceptions can help taxpayers navigate the complexities of the 5080 Michigan form more effectively. Accurate reporting is essential to avoid penalties and ensure compliance with state tax regulations.