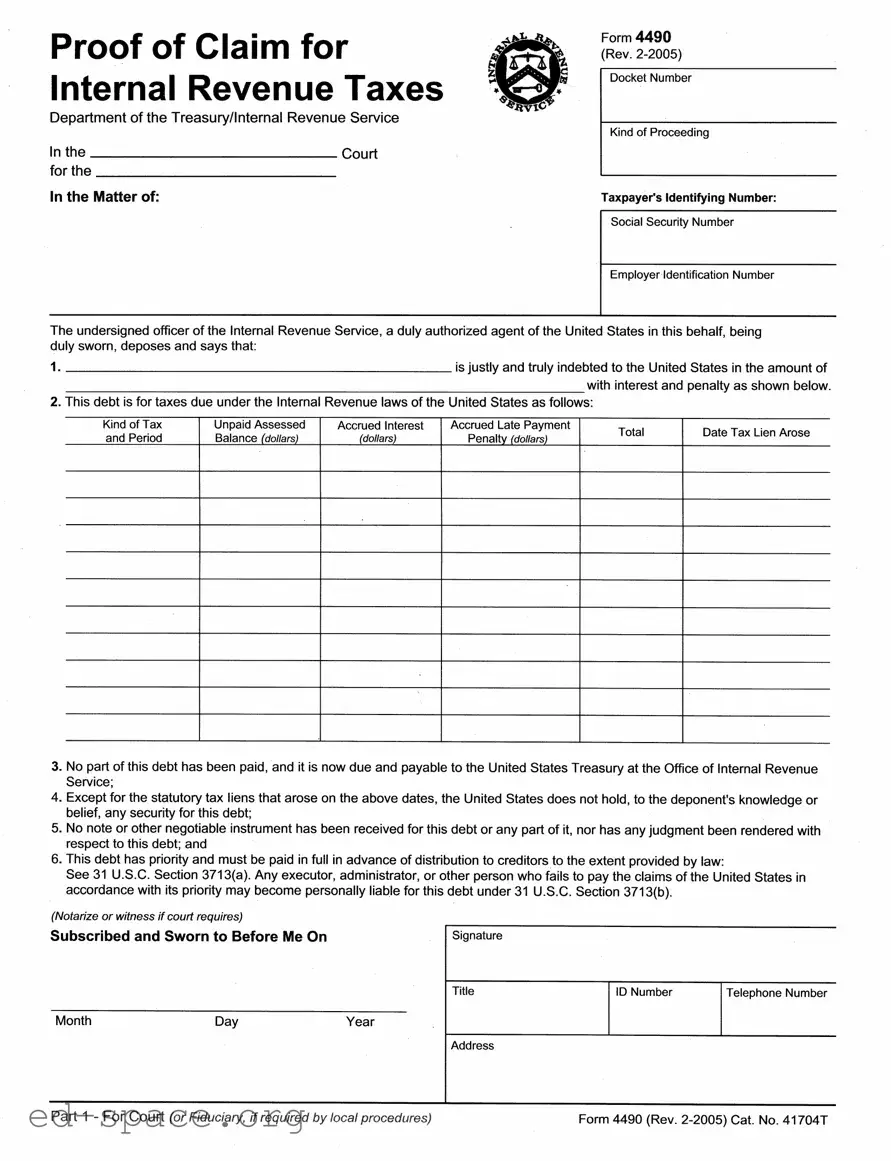

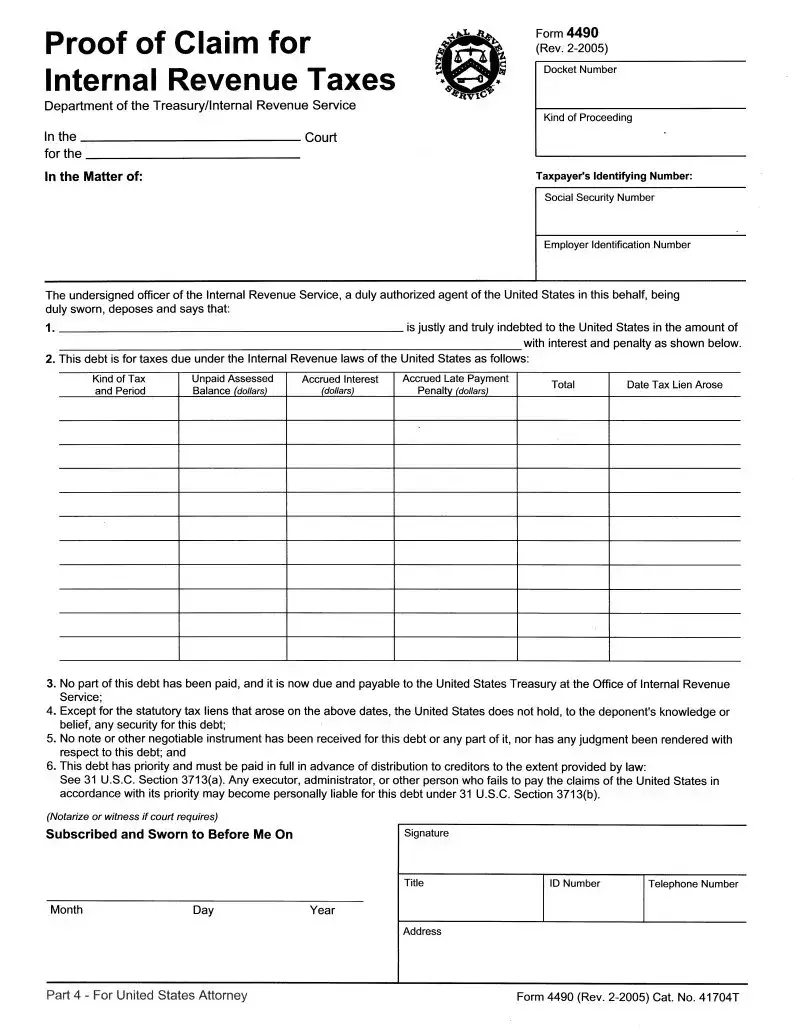

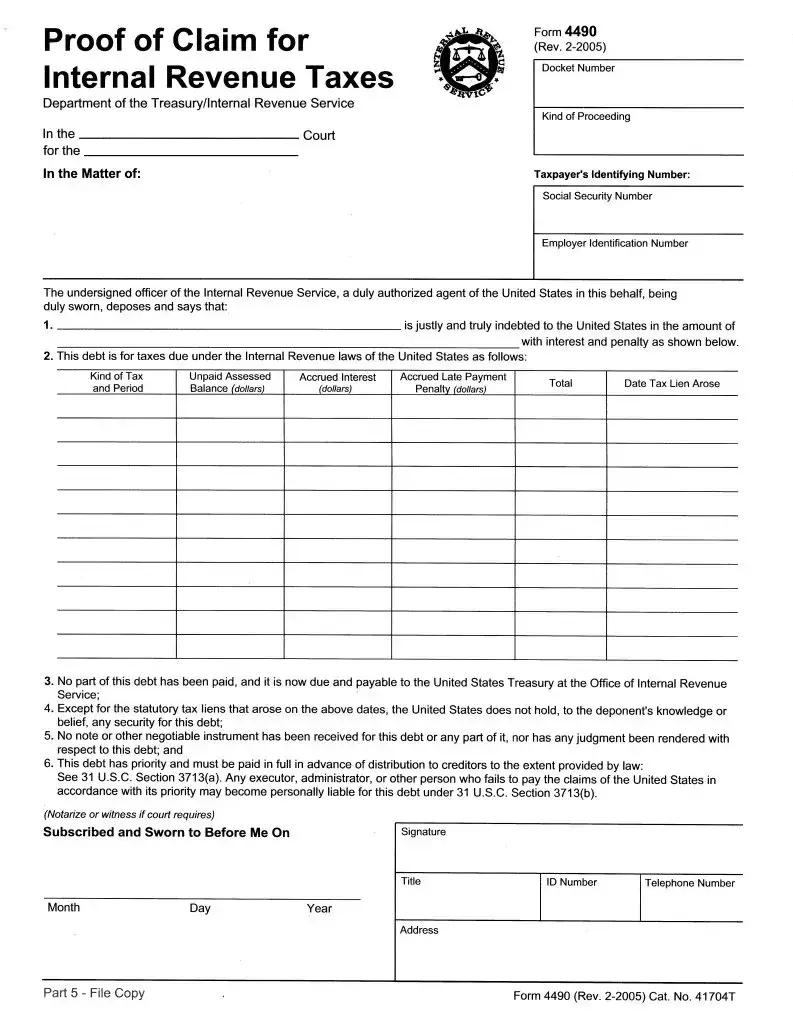

The Form 4490, also known as the Proof of Claim for Internal Revenue Taxes, plays a crucial role in tax proceedings involving the Internal Revenue Service (IRS). This form is typically filed in court to establish a claim for unpaid taxes owed to the United States. It outlines specific details, including the taxpayer's identifying numbers, the amount owed, and any applicable interest and penalties. Additionally, the form highlights that the debt is due and payable, asserting the priority of the claim over other creditors. It serves as an official declaration from a duly authorized IRS officer, affirming that the taxpayer has not made any payments toward the debt and that no security has been provided for it. Furthermore, the form emphasizes the legal implications of failing to pay the claim, which can lead to personal liability for executors or administrators involved in the estate. Understanding the significance of Form 4490 is essential for anyone navigating tax-related legal matters.

| Fact Name | Description |

|---|---|

| Purpose | The 4490 form serves as a Proof of Claim for Internal Revenue Taxes owed to the United States. |

| Governing Authority | This form is governed by the Internal Revenue Code and related federal tax laws. |

| Submission Requirement | It must be filed in court, or with a fiduciary, if required by local procedures. |

| Debt Declaration | The form requires the undersigned to declare the amount owed, including interest and penalties. |

| Priority of Claim | Claims made using this form have priority under 31 U.S.C. Section 3713(a). |

| Personal Liability | Failure to pay the claim may result in personal liability for executors or administrators under 31 U.S.C. Section 3713(b). |

| Notarization | The form must be notarized or witnessed if the court requires it. |

Completing the 4490 form requires careful attention to detail, as it is essential for establishing a claim for internal revenue taxes. Following these steps will help ensure that the form is filled out correctly and submitted in a timely manner.

Once the form is filled out completely, ensure that it is returned to the appropriate office or individual as specified in the instructions. Keep a copy for your records, as it is essential to retain documentation of the claim.

What is Form 4490?

Form 4490 is a document used to file a Proof of Claim for Internal Revenue Taxes with the Internal Revenue Service (IRS). This form is typically filed in bankruptcy proceedings to establish the government's claim for unpaid taxes owed by a taxpayer.

Who needs to file Form 4490?

Individuals or entities that owe taxes to the IRS and are involved in bankruptcy proceedings may need to file Form 4490. It is essential for the IRS to formally assert its claim for unpaid taxes in these situations.

What information is required on Form 4490?

Form 4490 requires specific information, including the taxpayer's identifying number (Social Security Number or Employer Identification Number), the amount owed, details about the tax type, and any accrued interest or penalties. The form also includes sections for the date the tax lien arose and the total amount due.

What happens if Form 4490 is not filed?

If Form 4490 is not filed, the IRS may not be able to recover the taxes owed during the bankruptcy process. This could result in the IRS losing its priority claim over other creditors, which may lead to the taxpayer being relieved of the tax debt if it is not properly asserted.

How is Form 4490 submitted?

After completing Form 4490, it should be submitted to the appropriate court or fiduciary handling the bankruptcy case. It may also need to be returned to the IRS, depending on local procedures.

What are the consequences of not paying the debt listed on Form 4490?

Failure to pay the debt listed on Form 4490 may lead to personal liability for executors or administrators who do not comply with the IRS's priority claims. This liability can arise under federal law, making it crucial to address the claims appropriately.

Is notarization required for Form 4490?

Yes, Form 4490 may require notarization or a witness signature, depending on the court's requirements. This step helps to verify the authenticity of the claims made in the document.

What should I do if I have questions about Form 4490?

If you have questions about Form 4490, it is advisable to consult with a tax professional or legal expert who can provide guidance tailored to your specific situation. They can help ensure that the form is completed correctly and submitted in accordance with the law.

Failing to provide complete taxpayer identifying information, such as the Social Security Number or Employer Identification Number.

Leaving out the total amount of debt owed, including interest and penalties, which is crucial for accurate processing.

Not specifying the kind of tax owed, which can lead to confusion and delays in processing the claim.

Incorrectly calculating the amounts for unpaid taxes, accrued interest, and penalties, leading to discrepancies.

Failing to sign and date the form, which can render the submission invalid.

Neglecting to provide a proper address or contact information, making it difficult for the IRS to reach you.

Not notarizing the form if required, which can result in rejection of the claim.

Submitting the form without checking for errors or omissions, which can lead to processing delays.

Ignoring deadlines for submission, which may affect the validity of the claim.

Failing to keep a copy of the submitted form for personal records, which is essential for future reference.

The Form 4490 is a critical document used in the context of tax claims against individuals or entities. When filing this form, there are several other documents that may be necessary to support the claim or provide additional information. Below is a list of commonly used forms and documents that often accompany the Form 4490.

Understanding these forms can help individuals and businesses navigate the complexities of tax obligations and claims. Each document serves a specific purpose and can provide valuable context when dealing with the IRS and tax-related issues.

The Form 4490 is a Proof of Claim for Internal Revenue Taxes, used primarily to establish a claim for unpaid taxes owed to the United States. Several other documents serve similar purposes in various contexts, particularly in bankruptcy and tax proceedings. Here are seven documents that share similarities with the Form 4490:

When filling out Form 4490, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are six important dos and don'ts:

Understanding the 4490 form can be challenging, especially with the various misconceptions that exist. Here are six common misunderstandings about this form, along with clarifications to help you navigate its purpose and implications.

Being informed about these misconceptions can help you approach the 4490 form with a clearer understanding of its role and the responsibilities it entails. If you have further questions, seeking guidance from a qualified professional can provide additional clarity.

Understanding the 4490 form is crucial for anyone dealing with tax claims in the United States. Here are five key takeaways to consider: