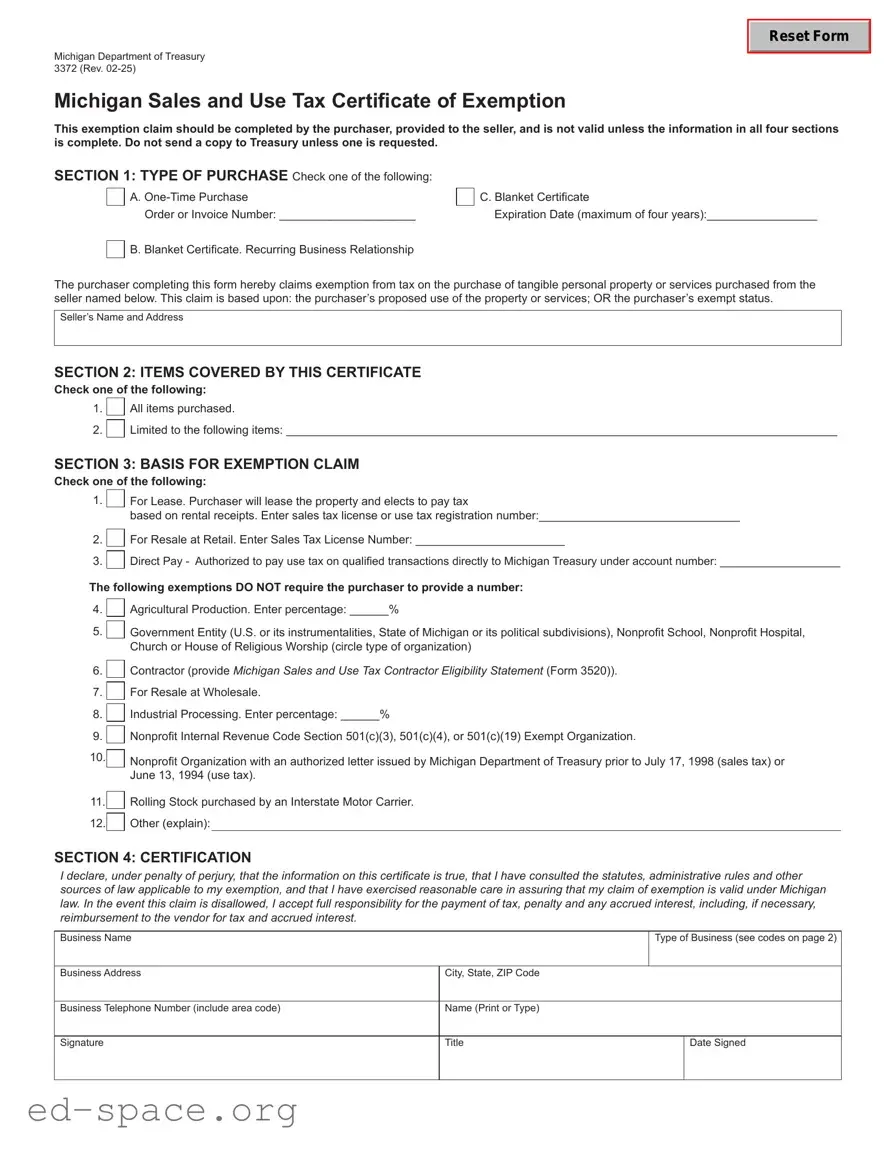

The Michigan Department of Treasury Form 3372 is an essential document for businesses seeking to claim exemption from sales and use tax in the state. This form must be filled out by the purchaser and provided to the seller to validate the exemption. It is crucial that all four sections of the form are completed accurately; otherwise, the claim may be deemed invalid. The first section allows the purchaser to specify the type of purchase, whether it’s a one-time transaction or a blanket certificate for ongoing business relationships. Section two requires the purchaser to identify the items covered by the exemption, either as all items or specific ones. In section three, the basis for the exemption claim must be selected, with options ranging from leasing to various nonprofit statuses. Finally, section four includes a certification statement that the purchaser must sign, affirming the truthfulness of the information provided. This form is not submitted to the Treasury unless requested, but it is vital for maintaining compliance and avoiding potential penalties. Proper use of Form 3372 can lead to significant tax savings for eligible businesses.

Michigan Department of Treasury 3372 (Rev.

Reset Form

Michigan Sales and Use Tax Certificate of Exemption

This exemption claim should be completed by the purchaser, provided to the seller, and is not valid unless the information in all four sections is complete. Do not send a copy to Treasury unless one is requested.

SECTION 1: TYPE OF PURCHASE Check one of the following:

A.

Order or Invoice Number: _____________________

B. Blanket Certificate. Recurring Business Relationship

C. Blanket Certificate

Expiration Date (maximum of four years):_________________

The purchaser completing this form hereby claims exemption from tax on the purchase of tangible personal property or services purchased from the seller named below. This claim is based upon: the purchaser’s proposed use of the property or services; OR the purchaser’s exempt status.

Seller’s Name and Address

SECTION 2: ITEMS COVERED BY THIS CERTIFICATE

Check one of the following:

1.

2.

All items purchased.

Limited to the following items: _____________________________________________________________________________________

SECTION 3: BASIS FOR EXEMPTION CLAIM

Check one of the following:

1.

For Lease. Purchaser will lease the property and elects to pay tax

based on rental receipts. Enter sales tax license or use tax registration number:_______________________________

2.

3.

For Resale at Retail. Enter Sales Tax License Number: _______________________

Direct Pay - Authorized to pay use tax on qualified transactions directly to Michigan Treasury under account number: ___________________

The following exemptions DO NOT require the purchaser to provide a number:

4.

5.

Agricultural Production. Enter percentage: ______%

Government Entity (U.S. or its instrumentalities, State of Michigan or its political subdivisions), Nonprofit School, Nonprofit Hospital, Church or House of Religious Worship (circle type of organization)

6.

7.

8.

9.

10.

11.

12.

Contractor (provide Michigan Sales and Use Tax Contractor Eligibility Statement (Form 3520)).

For Resale at Wholesale.

Industrial Processing. Enter percentage: ______%

Nonprofit Internal Revenue Code Section 501(c)(3), 501(c)(4), or 501(c)(19) Exempt Organization.

Nonprofit Organization with an authorized letter issued by Michigan Department of Treasury prior to July 17, 1998 (sales tax) or June 13, 1994 (use tax).

Rolling Stock purchased by an Interstate Motor Carrier.

Other (explain):

SECTION 4: CERTIFICATION

I declare, under penalty of perjury, that the information on this certificate is true, that I have consulted the statutes, administrative rules and other sources of law applicable to my exemption, and that I have exercised reasonable care in assuring that my claim of exemption is valid under Michigan law. In the event this claim is disallowed, I accept full responsibility for the payment of tax, penalty and any accrued interest, including, if necessary, reimbursement to the vendor for tax and accrued interest.

Business Name |

|

Type of Business (see codes on page 2) |

Business Address |

City, State, ZIP Code |

|

Business Telephone Number (include area code) |

Name (Print or Type) |

|

Signature |

Title |

Date Signed |

3372, Page 2

Instructions for completing Michigan Sales and Use Tax Certificate of Exemption (Form 3372)

Purchasers may use this form to claim exemption from Michigan sales and use tax on qualified transactions. All fields must be completed; however, if provided to the purchaser in electronic format, a signature is not required. All claims are subject to audit. The purchaser must ensure eligibility of the exemption claimed; a purchaser who improperly claims an exemption is liable for tax, penalty, and interest, with limited exceptions.

Sellers: Michigan does not issue “tax exempt numbers” and a seller is not permitted to rely on a number in lieu of a valid exemption claim. Sellers are required to maintain proper records of exempt sales, including exemption forms or the same information in another format. Records may be kept electronically. If the exemption certificate is received in electronic format, a signature is not required. A seller who does not comply with these requirements may be liable for tax, penalty, and interest. See Revenue Administrative Bulletin

SECTION 1:

A)Choose

B)Choose “Blanket Certificate” if there is a “recurring business relationship.” This exists when a period of not more than 12 months elapses between sales transactions between the seller and purchaser. Parties do not need to renew this blanket exemption claim as long as the recurring business relationship exists.

C)Choose “Blanket Certificate” and enter the expiration date (maximum four years) when there may be a period of more than 12 months between sales transactions. This option is best when purchaser and seller anticipate more than one exempt transaction before the expiration date but do not have or may not maintain a recurring business relationship.

SECTION 2:

Place a check in the box for “All items purchased” or choose “Limited to” and list the items that are covered by the exemption claim.

SECTION 3:

Check the box that applies and, if applicable, provide the required information. The exemptions listed are the most common. If the exemption you are claiming is not listed, check “Other” and enter the qualifying exemption.

SECTION 4:

Purchaser must complete Section 4. A signature is only required if a paper form is used; in that case, the purchaser should sign and provide their title (for example, Purchasing Manager, President, Owner). For Type of Business, enter the number from the following list that best describes the purchaser’s business.

01 |

Accommodations |

10 |

Utilities |

02 |

Agricultural |

11 |

Wholesale |

03 |

Construction |

12 |

Advertising, newspaper |

04 |

Manufacturing |

13 |

|

05 |

Government |

14 |

|

06 |

Rental or leasing |

15 |

|

07 |

Retail |

16 |

Other (enter code and write in business type) |

08 |

Church |

|

|

09 |

Transportation |

|

|

| Fact Name | Details |

|---|---|

| Form Title | Michigan Sales and Use Tax Certificate of Exemption (Form 3372) |

| Governing Law | Michigan Sales and Use Tax Act |

| Purpose | This form allows purchasers to claim exemption from sales and use tax on eligible transactions. |

| Completion Requirement | All four sections must be fully completed for the exemption claim to be valid. |

| Submission Guidelines | A copy should not be sent to the Treasury unless specifically requested. |

| Types of Purchases | Includes one-time purchases and blanket certificates for recurring relationships. |

| Exemption Basis | Claims can be based on proposed use of property or services or the purchaser’s exempt status. |

| Audit Notice | All claims are subject to audit; improper claims may result in tax liability. |

| Record Keeping | Sellers must maintain records of exempt sales, including exemption forms or equivalent information. |

Once you have gathered all necessary information, follow these steps to complete the Michigan Sales and Use Tax Certificate of Exemption (Form 3372). Ensure that all sections are filled out accurately before submitting the form to the seller.

What is the Michigan Form 3372?

The Michigan Form 3372, also known as the Michigan Sales and Use Tax Certificate of Exemption, is a document that allows purchasers to claim exemption from sales and use tax on certain transactions. It must be completed by the purchaser and provided to the seller. The form is not valid unless all four sections are filled out completely.

Who should fill out the Form 3372?

The purchaser is responsible for completing the Form 3372. This includes individuals or businesses that intend to buy tangible personal property or services without paying sales tax. The completed form should then be given to the seller to validate the exemption claim.

What information is required on the Form 3372?

The form requires several key pieces of information, including the type of purchase (one-time or blanket), items covered by the certificate, the basis for the exemption claim, and the purchaser's certification. Each section must be completed accurately to ensure the exemption is valid.

What are the types of purchases that can be claimed on Form 3372?

Purchasers can select either a one-time purchase or a blanket certificate. A one-time purchase requires an order or invoice number, while a blanket certificate can be used for recurring business relationships or for a specified period of up to four years. This flexibility allows businesses to manage their tax-exempt purchases effectively.

What are the common exemptions listed on Form 3372?

Common exemptions include purchases for resale, agricultural production, government entities, and nonprofit organizations. Each exemption type has specific requirements that must be met, such as providing a sales tax license number or percentage of agricultural production. If a purchaser's exemption is not listed, they can select "Other" and provide an explanation.

Is a signature required on the Form 3372?

A signature is only required if the form is being submitted in paper format. If the form is provided electronically, a signature is not necessary. However, the purchaser must still ensure that all information is accurate and complete, as they are responsible for the validity of the exemption claim.

What happens if an exemption claim is disallowed?

If a claim for exemption is disallowed, the purchaser is responsible for paying any tax, penalties, and accrued interest. This includes reimbursing the seller for any tax that was not collected at the time of sale. It is crucial for purchasers to understand their eligibility for the exemption to avoid potential liabilities.

How long is a blanket certificate valid?

A blanket certificate can be valid for a maximum of four years. This option is beneficial for purchasers who anticipate multiple exempt transactions within that time frame but do not maintain a recurring business relationship. It is important to keep track of the expiration date to ensure continued compliance.

What should sellers do with the exemption certificates they receive?

Sellers must maintain proper records of all exempt sales, including the exemption certificates. These records can be kept electronically and should include all necessary information to substantiate the exempt status of the sale. Failure to comply with record-keeping requirements may result in tax liabilities for the seller.

Incomplete Sections: One of the most common mistakes is failing to fill out all four sections of the form. Each section is crucial for validating the exemption claim. Incomplete forms may lead to rejection.

Incorrect Type of Purchase: Selecting the wrong type of purchase can invalidate the exemption. Ensure you accurately choose between a one-time purchase and a blanket certificate based on your business relationship with the seller.

Missing or Incorrect Seller Information: Providing incorrect seller details can complicate the transaction. Always double-check the seller’s name and address to ensure accuracy.

Failure to Specify Items: In Section 2, neglecting to specify which items are covered by the exemption can lead to issues. Be clear whether the exemption applies to all items or only specific ones.

Incorrect Basis for Exemption: Selecting the wrong basis for exemption in Section 3 can result in significant complications. Carefully review the available options and choose the one that accurately reflects your situation.

Missing Signature: If you are submitting a paper form, not signing the document can render it invalid. Make sure to sign and include your title if required.

Ignoring Expiration Dates: For blanket certificates, failing to note the expiration date can lead to misunderstandings. Always include the maximum four-year expiration date if applicable.

The Michigan Department of Treasury Form 3372 is essential for claiming exemption from sales and use tax on qualified purchases. However, it is often accompanied by other important forms and documents that help clarify the exemption process and ensure compliance with state regulations. Below are four commonly used documents that complement the 3372 form.

Understanding these additional forms and documents is crucial for anyone looking to navigate the complexities of sales and use tax exemptions in Michigan. By ensuring all necessary paperwork is in order, purchasers can protect themselves from potential tax liabilities and maintain compliance with state laws.

The Michigan Department of Treasury Form 3372 serves as a Sales and Use Tax Certificate of Exemption. It allows purchasers to claim exemption from sales and use tax on qualified transactions. Several other documents serve similar purposes in different contexts or jurisdictions. Here is a list of ten such documents:

Each of these documents plays a crucial role in establishing tax-exempt status, ensuring compliance with tax laws, and facilitating proper record-keeping for both purchasers and sellers.

When filling out the Michigan Sales and Use Tax Certificate of Exemption (Form 3372), it’s important to follow specific guidelines to ensure your submission is valid. Here’s a helpful list of things to do and avoid:

By following these guidelines, you can help ensure that your exemption claim is processed smoothly and correctly.

Here are ten common misconceptions about the Michigan Department of Treasury 3372 form, along with clarifications to help you understand its purpose and requirements:

This is incorrect. The form is only required to be given to the seller and should not be sent to the Treasury unless specifically requested.

If the form is provided in electronic format, a signature is not necessary. A signature is only required for paper submissions.

Only eligible purchasers can claim an exemption. The purchaser must ensure they meet the criteria for the exemption being claimed.

For blanket certificates, there is an expiration date of up to four years. After this period, a new form must be completed.

Sellers are not allowed to depend on a number in place of a valid exemption claim. Proper documentation must be maintained.

The form allows the purchaser to specify whether all items or only certain items are covered by the exemption.

The 3372 form is intended for business-related purchases only. Personal purchases do not qualify for exemption.

This form specifically addresses sales and use tax exemptions. Other taxes may have different requirements.

All claims are subject to audit. If an exemption is improperly claimed, the purchaser is responsible for any taxes, penalties, and interest.

Any qualifying purchaser, regardless of size, can use this form to claim exemptions on eligible transactions.

Here are key takeaways regarding the Michigan Department of Treasury 3372 form, also known as the Sales and Use Tax Certificate of Exemption: