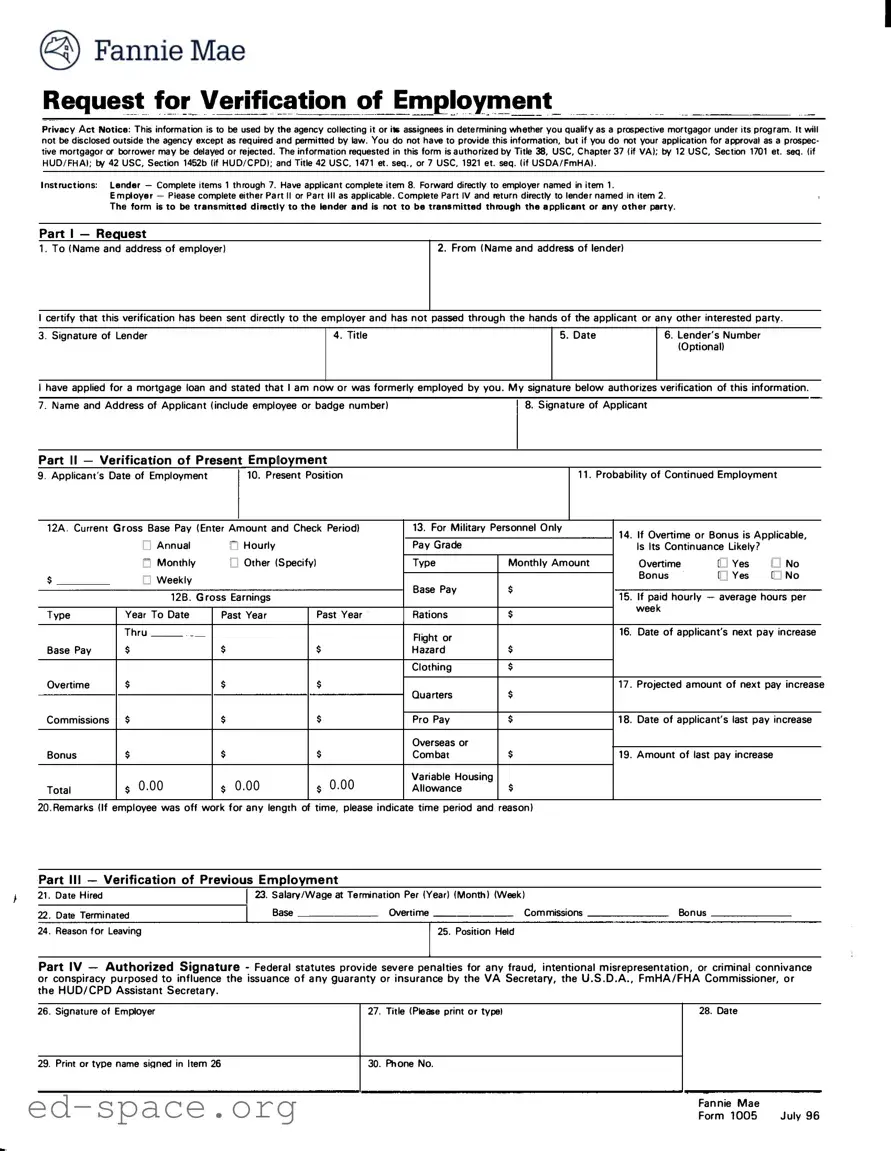

The 1005 Verification of Employment form plays a crucial role in the mortgage application process, serving as a vital tool for lenders to assess an applicant's employment history and income stability. This form is specifically designed to confirm both current and past employment details, ensuring that lenders have accurate information to evaluate a borrower's creditworthiness. The process begins when a lender fills out the initial sections of the form, which includes the lender's name, address, and other relevant details. The applicant must then authorize the verification by signing the form, thereby allowing the employer to disclose necessary employment information. The form is divided into distinct parts, allowing employers to provide detailed insights about the applicant's job status, salary, and likelihood of continued employment. Notably, the form must be sent directly from the employer to the lender, bypassing the applicant to maintain confidentiality and integrity. Furthermore, the document complies with various federal regulations, emphasizing the importance of accurate and truthful reporting. Understanding the intricacies of the 1005 Verification of Employment form is essential for both lenders and applicants, as it directly impacts the approval process for mortgage loans.

I

�FannieMae

Request fc,r Verification of Em�le>y_111ent

Privacy Act Notice: This information is to be used by the agency collecting it or its assignees in determining whether you qualify as a prospective mortgagor under its program. It will not be disclosed outside the agency except as required and permitted by law. You do not have to provide this information, but if you do not your application for approval as a prospec tive mortgagor or borrower may be delayed or rejected. The information requested in this form is authorized by Title 38, USC, Chapter 37 (if VA); by 12 USC, Section 1701 et. seq. (if HUD/FHA); by 42 USC, Section 1452b (if HUD/CPD); and Title 42 USC, 1471 et. seq., or 7 USC, 1921 et. seq. (if USDA/FmHA).

Instructions: Lender - Complete items 1 through 7. Have applicant complete item 8. Forward directly to employer named in item 1.

Employer Please complete either Part II or Part Ill as applicable. Complete Part IV and return directly to lender named in item 2.

The form is- to be transmitted directly to the lender and is not to be transmitted through the applicant or any other party.

Part I - Re uest

1. To (Name and address of employer)

I certify that this verification has been sent directly to the employer and has not passed through the hands of the applicant or any other interested party.

3. Signature of Lender4. Title5. Date 6. Lender's Number (Optional)

|

|

I have applied for a mortgage loan and stated that I am now or was formerly employed by you. My signature below authorizes verification of this information. |

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

7. Name and Address of Applicant (include employee or badge number) |

|

|

|

|

|

|

8. Signature of Applicant |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Part II - |

VenT1cat1on ofPresent |

|

Emp1oyment |

|

|

|

|

|

|

|

|

|

|

|

|

|

11. Probability of Continued Employment |

|

|

|

|

|

|||||||||||||||||||||||||||

|

9. Applicant's Date of Employment |

|

|

|

10. Present Position |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

12A. Current Gross Base Pay (Enter Amount and Check Period) |

|

|

|

|

|

13. For Military Personnel Only |

14. If Overtime or Bonus is Applicable, |

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

D |

Annual |

|

□ |

Hourly |

|

|

|

|

|

|

|

Pay Grade |

|

|

|

|

|

|

Is Its Continuance Likely? |

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

D |

Monthly |

|

D |

Other (Specify) |

|

|

|

|

|

|

Type |

|

Monthly Amount |

Overtime |

|

D |

Yes |

D |

No |

||||||||||||||||||||||

$ |

|

|

|

|

|

C |

Weekly |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bonus |

|

□ |

Yes |

□ |

No |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Base Pay |

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

128. Gross Earnings |

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

15. If paid hourly - average hours per |

||||||||||||||||||||||||

|

|

Type |

|

|

|

Year To Date |

|

Past Year |

|

|

Past Year |

19__ |

Rations |

|

$ |

|

|

|

|

|

week |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

19_ _ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Base Pay |

|

|

|

Thru __19_ |

|

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

Flight or |

|

$ |

|

|

|

|

|

16. Date of applicant's next pay increase |

|||||||||||||||||||

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hazard |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

Overtime |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Clothing |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

$ |

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

Quarters |

|

$ |

|

|

|

|

|

17. Projected amount of next pay increase |

|

|||||||||||||||||

|

|

Commissions |

$ |

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pro Pay |

|

$ |

|

|

|

|

|

18. Date of applicant's last pay increase |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Overseas or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Bonus |

|

|

|

$ |

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

Combat |

|

$ |

|

|

|

|

|

19. Amount of last pay increase |

|

|

|

|

|

|||||||||||

|

|

Total |

|

|

|

$ |

0.00 |

|

$ |

0.00 |

|

|

$ |

0.00 |

|

|

|

|

|

Variable Housing |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

20.Remarks (If employee was off work for any length of time, please indicate time period and reason) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

Part Ill - Verification ofPrevious Em lo ment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

21. Date Hired |

|

|

|

|

|

|

|

|

|

23. Salary/Wage at Termination Per (Year) (Month) (Week) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Base |

Overtime |

Commissions |

|

|

|

|

|

Bonus |

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

22. Date Terminated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

24. Reason for Leaving |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

125. Position Held |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part IV - |

Authorized Signature - Federal statutes provide severe penalties for any fraud, intentional misrepresentation, or criminal connivance |

||||||||||||||||||||||||||||||||||||||||||||||||

or conspiracy purposed to influence the issuance of any guaranty or insurance by the VA Secretary, the U.S.D.A., FmHA/FHA Commissioner, or |

|||||||||||||||||||||||||||||||||||||||||||||||||

the HUD/CPD Assistant Secretary. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

28. Date |

|

|

|

|

|

|

|||||||||||||

|

|

26. Signature of Employer |

|

|

|

|

|

|

|

|

|

|

|

|

27. Title (Please print or type) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29. Print or type name signed in Item 26 |

|

|

|

|

|

|

|

|

30. Phone No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fannie Mae |

|

July 96 |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 1005 |

|

|||||||

Instructions

Verification of Employment

The lender uses this form for applications for conventional first or second mortgages to verify the applicant's past and present employment status.

Copies

Original only.

Printing Instructions

This form must be printed on letter size paper, using portrait format.

Instructions

The applicant must sign this form to authorize his or her employer(s) to release the requested information. Separate forms should be sent to each firm that employed the applicant in the past two years. However, rather than having an applicant sign multiple forms, the lender may have the applicant sign a borrower's signature authorization form, which gives the lender blanket authorization to request the information it needs to evaluate the applicant's creditworthiness. When the lender uses this type of blanket authorization, it must attach a copy of the authorization form to each Form 1005 it sends to the applicant's employer(s).

For First Mortgages:

The lender must send the request directly to the employers. We will not permit the borrower to

For Second Mortgages:

The borrower may

Instructions Page

| Fact Name | Description |

|---|---|

| Purpose | The 1005 Verification of Employment form is used by lenders to confirm an applicant's current and past employment status during mortgage applications. |

| Privacy Notice | This form includes a Privacy Act Notice, stating that the information will be used solely for assessing mortgage eligibility and will not be shared outside the agency without legal permission. |

| Completion Instructions | Lenders must fill out items 1 through 7, while applicants are required to complete item 8 before the form is sent directly to the employer. |

| Governing Laws | The form is authorized by various federal laws including Title 38 USC, Chapter 37 (VA), and 12 USC, Section 1701 et. seq. (HUD/FHA). |

| Transmission Protocol | The form must be sent directly from the employer to the lender. It should not pass through the applicant or any third party. |

Filling out the 1005 Verification of Employment form is a straightforward process, but attention to detail is essential. Once the form is completed, it will be sent directly to the employer listed, ensuring that the lender receives accurate and timely employment verification. This helps facilitate the mortgage application process.

What is the purpose of the 1005 Verification of Employment form?

The 1005 Verification of Employment form is designed to confirm an applicant's employment status as part of the mortgage application process. Lenders use this form to gather essential information about an applicant’s current and past employment, ensuring they have the necessary financial stability to qualify for a mortgage. This verification helps assess the applicant's creditworthiness and ability to repay the loan.

Who is responsible for filling out the 1005 form?

The lender initiates the process by completing the first section of the form, which includes details about the lender and the applicant. The applicant must then sign the form to authorize their employer to release the requested information. Finally, the employer is responsible for completing the relevant sections regarding the applicant's employment status and returning the form directly to the lender.

How is the information on the 1005 form protected?

The information collected through the 1005 form is protected under the Privacy Act. This means that the data will only be used by the agency collecting it or its assignees to determine the applicant's eligibility for a mortgage. Disclosure of this information outside the agency is restricted, ensuring that the applicant's personal and employment details remain confidential, except as required by law.

What happens if I do not provide the information requested on the 1005 form?

While providing the information is not mandatory, failing to do so may lead to delays or even rejection of your mortgage application. The lender relies on this verification to evaluate your financial stability, and incomplete information could hinder their ability to make an informed decision.

Can I hand-carry the 1005 form to my employer?

For first mortgage applications, the lender must send the verification request directly to the employer. The applicant is not permitted to hand-carry the form. However, for second mortgages, the borrower may deliver the form to the employer, who must then mail it directly back to the lender. This distinction ensures that the information remains secure and is transmitted directly between the employer and lender.

What should I do if I have worked for multiple employers in the past two years?

If you have had multiple employers within the last two years, separate 1005 forms must be sent to each employer to verify your employment history. Instead of signing multiple forms, you may opt to sign a borrower's signature authorization form. This blanket authorization allows the lender to request the necessary information from all your past employers without requiring individual signatures on each form.

What are the consequences of providing false information on the 1005 form?

Providing false information or intentionally misrepresenting your employment status on the 1005 form can lead to severe penalties. Federal statutes impose strict consequences for fraud or misrepresentation, which may include legal action and financial repercussions. It is crucial to provide accurate and truthful information to avoid any potential issues with your mortgage application.

Incomplete Information: Many individuals fail to provide all required details on the form. Missing data, such as the employer's address or the applicant's employment dates, can lead to delays in processing.

Incorrect Signatures: Applicants sometimes forget to sign the form or may not sign in the designated area. An unsigned form cannot be processed, which may result in rejection of the application.

Sending Through the Applicant: Some applicants mistakenly submit the form themselves rather than ensuring it is sent directly from the employer to the lender. This can violate the requirements and lead to complications.

Failure to Follow Instructions: Not adhering to the specific instructions provided for completing the form can cause confusion. For example, applicants may not realize they need to send separate forms for different employers.

The 1005 Verification of Employment form is essential for lenders to confirm an applicant's employment status when processing mortgage applications. Alongside this form, several other documents are commonly used to provide a comprehensive view of an applicant's financial situation. Here are six important forms and documents often associated with the 1005 form:

These documents work together with the 1005 Verification of Employment form to give lenders a clearer picture of an applicant's financial situation. By providing accurate and complete information, applicants can help ensure a smoother mortgage approval process.

The 1005 Verification of Employment form serves a crucial role in the mortgage application process. Several other documents share similarities with this form, particularly in their purpose of verifying employment or income. Below are five documents that are comparable to the 1005 form:

When filling out the 1005 Verification of Employment form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are six things you should and shouldn't do:

Understanding the 1005 Verification of Employment form is essential for both lenders and applicants. However, several misconceptions can lead to confusion. Below are eight common misconceptions about this form, along with clarifications.

This is incorrect. The form must be sent directly from the lender to the employer to maintain confidentiality and integrity of the information.

In fact, the form is used to verify both current and past employment. It’s important for lenders to assess the applicant's entire employment history.

Only authorized personnel from the lender and the employer should complete the form. This ensures that the information provided is accurate and reliable.

The applicant must sign the form to authorize their employer to release the requested employment information. Without this signature, the verification cannot proceed.

While employers are encouraged to respond, they are not legally obligated to do so. However, many employers have policies in place to provide such verifications.

While it is primarily associated with mortgage applications, the 1005 form can also be utilized in other financial contexts where employment verification is necessary.

On the contrary, the information is protected under privacy laws. It should only be used for the purpose of verifying employment for lending decisions.

The form must be completed as is, without alterations. Modifications could lead to issues with the validity of the verification process.

By understanding these misconceptions, both applicants and lenders can navigate the employment verification process more effectively.

Understanding the 1005 Verification of Employment form is essential for a smooth mortgage application process.